- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Corteva (CTVA) Valuation Check After 2025 Earnings Results And 2026 Earnings Guidance

Why Corteva’s latest earnings matter for shareholders

Corteva (CTVA) just released its fourth quarter and full year 2025 results, pairing a quarterly net loss with higher full year net income and earnings per share, alongside fresh 2026 operating EPS guidance.

The company also reaffirmed a US$0.18 per share dividend for March 2026, so you are getting earnings, outlook and income signals at the same time, which can shape how you look at the stock.

See our latest analysis for Corteva.

Corteva’s recent news sits against a share price of US$73.62 and building momentum, with a 30-day share price return of 7.24% and a 90-day share price return of 12.02%. The 5-year total shareholder return of 75.36% shows how the story has played out over a longer stretch.

If earnings, guidance and dividends have you reassessing your watchlist, this is a good moment to broaden your search and check out 22 top founder-led companies as potential next ideas.

With Corteva trading at US$73.62, carrying a recent run of positive returns and sitting about 11% below the average analyst price target, you have to ask: is there still value here, or is the market already pricing in future growth?

Most Popular Narrative: 6.1% Undervalued

With Corteva last closing at $73.62 against a narrative fair value of $78.43, the current setup hinges on how earnings, margins and future valuation multiples line up.

Advancements in Corteva's innovation pipeline, including premium trait launches (Vorceed, PowerCore), expansion of biological products, and gene editing, enable premium pricing, secure market share, and improve product mix, translating into higher gross margins and earnings growth.

Want to see what is baked into that price gap? The narrative leans on steady revenue gains, rising margins and a future earnings multiple that has to step down from today. Curious how those moving parts combine to reach that fair value line, and what has to go right along the way?

Result: Fair Value of $78.43 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still watchpoints, including ongoing price pressure in crop protection and currency swings in markets like Brazil and Turkey that could challenge this valuation story.

Find out about the key risks to this Corteva narrative.

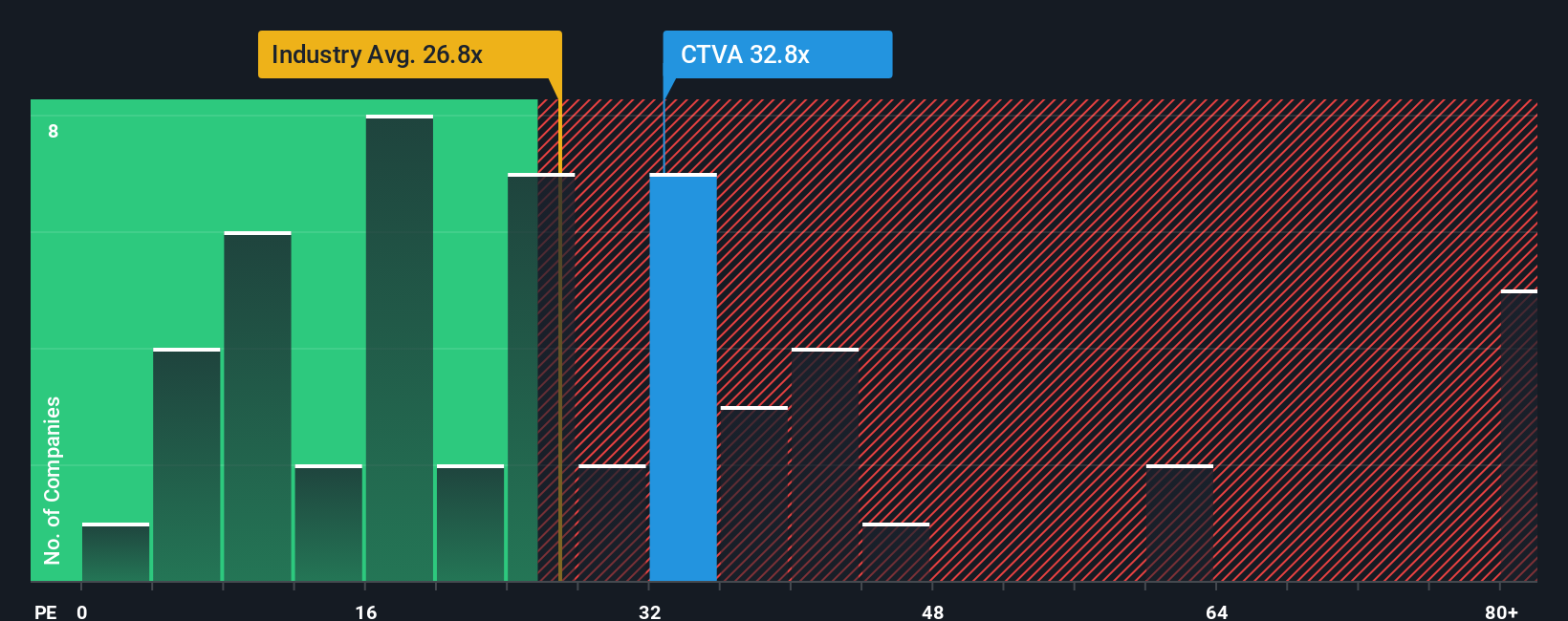

Another angle: earnings strength vs current P/E

The narrative model sees Corteva as 6.1% undervalued, yet the current P/E of 41.5x is well above both the US Chemicals industry at 25.4x and peers at 15.4x. It also sits ahead of a 28.2x fair ratio, which suggests the market is already paying up for the growth story. Is that a premium you are comfortable with?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Corteva Narrative

If you see the numbers differently or prefer to kick the tires yourself, you can rebuild the Corteva story in just a few minutes: Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Corteva.

Looking for more investment ideas?

If Corteva has sharpened your thinking, do not stop here. Use the Simply Wall St screener to quickly spot other opportunities that might suit your style.

- Zero in on quality at a discount by checking stocks our screener flags as 52 high quality undervalued stocks before the crowd focuses on them.

- Prioritise resilience by focusing on companies in our 82 resilient stocks with low risk scores that score well on stability and business risk.

- Hunt for lesser known opportunities by scanning our screener containing 24 high quality undiscovered gems that pair strong fundamentals with relatively low market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com