- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Sila Realty Trust’s Valuation After Recent Share Price Gains

Recent performance snapshot

Sila Realty Trust (SILA) has drawn investor attention after a recent stretch of positive returns, with the stock showing gains over the past week, month and past 3 months, alongside an annual revenue figure of US$193.381 million.

See our latest analysis for Sila Realty Trust.

At a share price of US$25.16, Sila Realty Trust has recently logged a 7.89% 1 month share price return and a 7.06% year to date share price return. The 1 year total shareholder return of 7.28% points to steady, if measured, momentum rather than a sharp re rating.

If Sila’s recent move has you thinking about where else income and defensiveness might show up, it could be a good moment to broaden your search with 22 top founder-led companies.

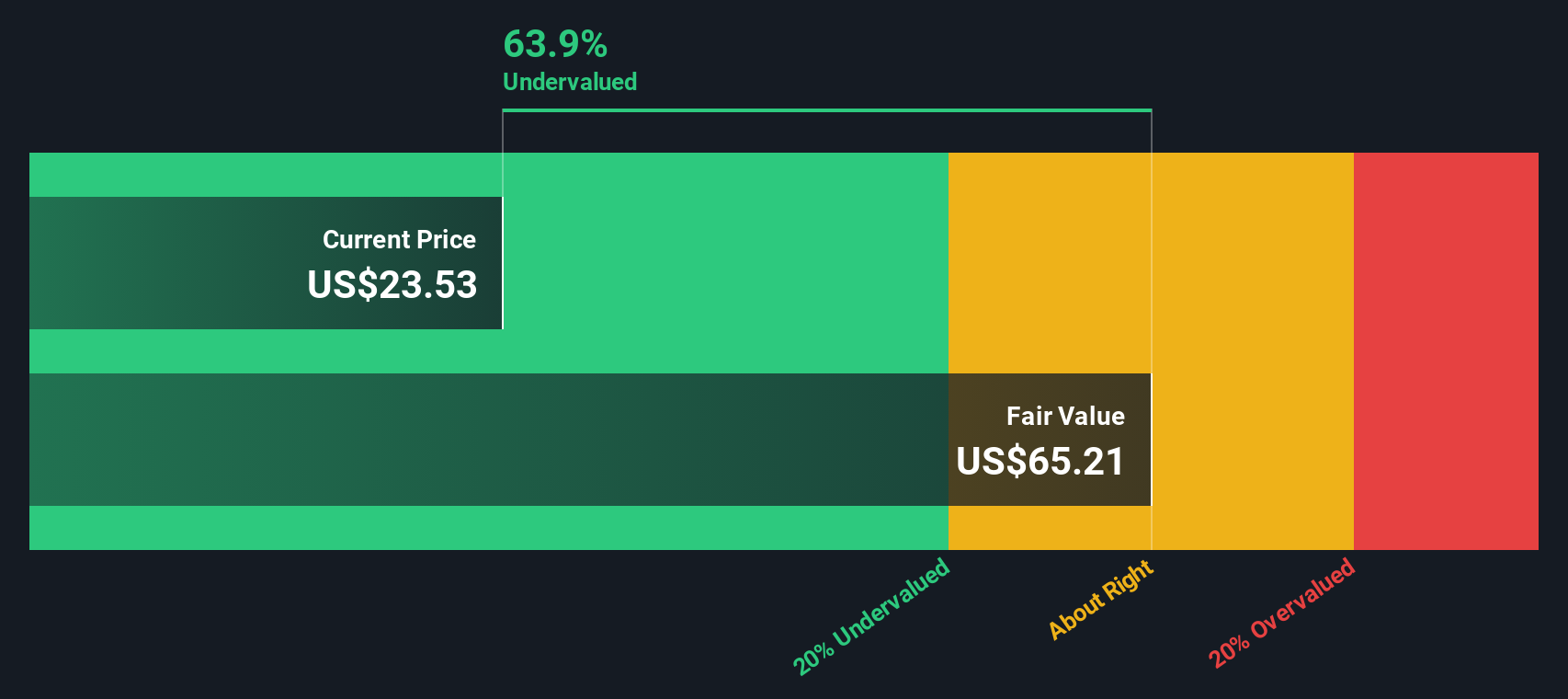

With Sila trading at US$25.16 alongside an indicated intrinsic discount of 61.69% and a value score of 2, the key question is whether this reflects a genuine mispricing or a market that is already factoring in future growth.

Most Popular Narrative: 15.1% Undervalued

With Sila Realty Trust last closing at $25.16 against a narrative fair value of $29.62, the current price sits below what this widely followed storyline considers reasonable, setting the scene for a closer look at the growth assumptions behind that gap.

Sila Realty Trust is benefitting from structural tailwinds related to the growing demand for healthcare facilities from the "aging adult" demographic and the increasing focus on necessity-based outpatient and post-acute care, which underpins stable long-term occupancy and predictable revenue from long lease terms with annual rent escalators, which in turn supports both revenue growth and margin stability.

Curious what kind of revenue climb, margin profile, and valuation multiple are baked into that fair value math, and how tightly those assumptions are wired together? The narrative spells out a specific growth runway, a targeted profitability step up, and a future earnings line that all have to sync for $29.62 to make sense.

Result: Fair Value of $29.62 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that fair value story could be knocked off course if higher interest costs squeeze profits or if more tenants run into financial trouble, which would pressure occupancy and rents.

Find out about the key risks to this Sila Realty Trust narrative.

Another angle on valuation

The consensus narrative focuses on future earnings and a high P/E. Our SWS DCF model, however, presents a different picture, with Sila trading 61.7% below its future cash flow value of $65.68. That is a much stronger undervaluation signal, so which story do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Sila Realty Trust Narrative

If you are not convinced by the existing storyline or simply want to stress test the assumptions yourself, you can build a personalised thesis in just a few minutes, starting with Do it your way.

A great starting point for your Sila Realty Trust research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Sila has caught your eye, do not stop there. A few focused screeners can quickly surface other opportunities that fit the kind of portfolio you want.

- Target income first by scanning companies in our 14 dividend fortresses that prioritize consistent shareholder payouts backed by meaningful yields.

- Hunt for pricing gaps using the 52 high quality undervalued stocks, where solid fundamentals line up with valuations that still look undemanding.

- Spot potential early movers through the screener containing 24 high quality undiscovered gems, highlighting quality businesses that are not yet widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com