- LIVE QUOTES

- LEARN

- HELP

EN

Atkore (ATKR) Valuation Check After Sharp Earnings And Profitability Declines

Q1 earnings put Atkore’s recent performance in focus

Atkore (ATKR) has come under closer scrutiny after first quarter results showed sales of US$655.55 million versus US$661.6 million a year earlier, with net income at US$15.03 million compared with US$46.34 million.

See our latest analysis for Atkore.

The weaker first quarter result comes after a period where short-term share price momentum has faded, with a 7-day share price return showing a decline of 4.81% and a 1-year total shareholder return showing a decline of 4.70%. In contrast, the 5-year total shareholder return shows a gain of 8.47%, indicating a more modest longer-term outcome.

If this earnings update has you reassessing your watchlist, it could be a good moment to widen the field and look at 24 power grid technology and infrastructure stocks as another way to find potential opportunities tied to electrical and infrastructure themes.

So with earnings under pressure, a mixed long term return profile and the shares trading only modestly below analyst targets, should you view Atkore as overlooked value, or assume the market already reflects its future growth prospects?

Most Popular Narrative: 5.5% Undervalued

Atkore’s most followed narrative puts fair value at about $70.40 per share, a little above the recent close around $66.53, and frames that gap around long dated infrastructure demand.

Robust investment trends in data centers and solar infrastructure, driven by demand for cloud/AI and renewable energy, are expected to deliver above-GDP growth in those verticals, expanding Atkore's addressable market and underpinning long-term revenue growth.

Curious what kind of revenue path, margin rebuild and future earnings multiple have to line up to reach that fair value? The most widely followed narrative spells it out, from construction exposure to mega projects to how a single discount rate ties all those moving pieces together. The full story connects modest top line ambitions with a much sharper recovery in profitability.

Result: Fair Value of $70.40 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on pricing and cost pressures easing and on mega projects arriving as expected; otherwise, earnings and margins could end up well below the narrative path.

Find out about the key risks to this Atkore narrative.

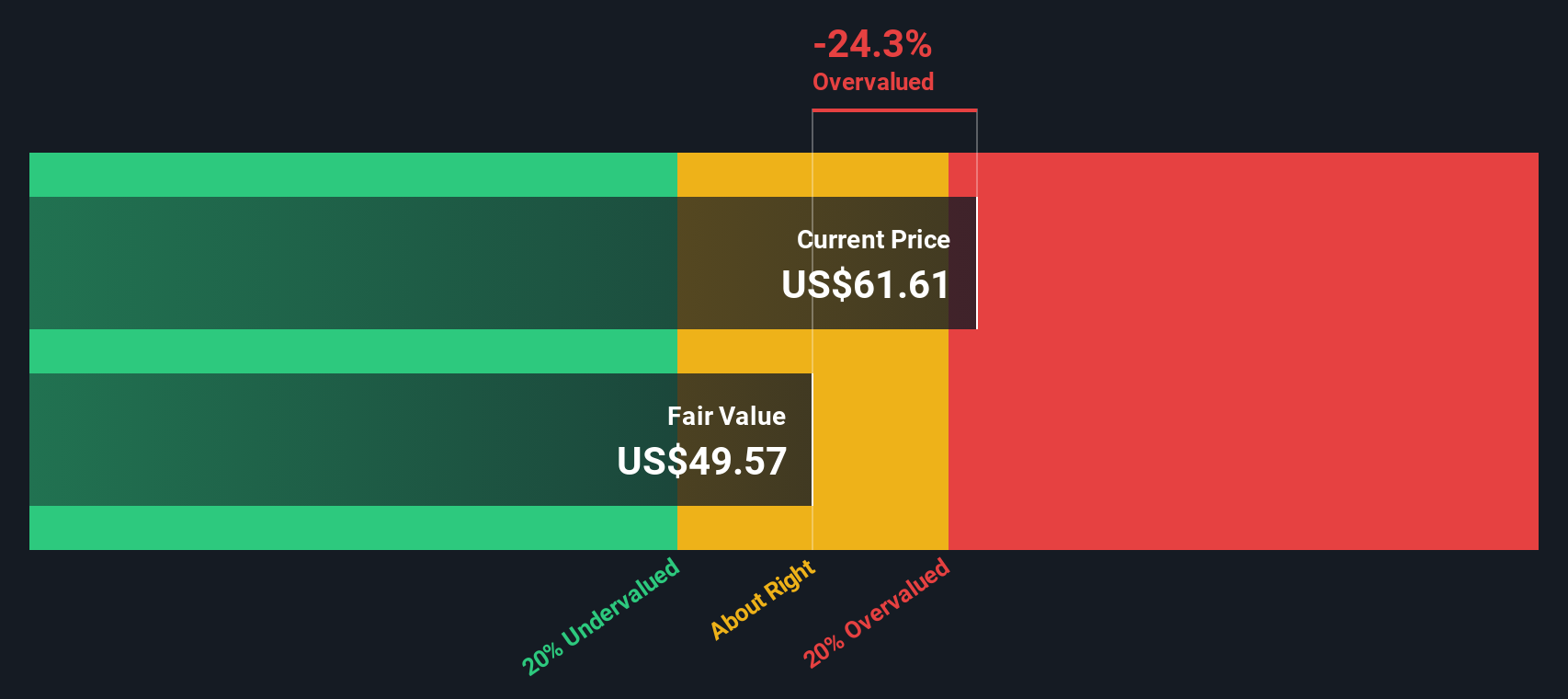

Another Angle: Our DCF Flags Overvaluation

That 5.5% undervalued narrative sits awkwardly beside our DCF work, which points to a fair value of about $32.62 per share, well below the recent $66.53 price. In this view, Atkore screens as richly priced. This raises the question of which story you trust more: the narrative or the cash flows?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Atkore for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 52 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Atkore Narrative

If you are not fully on board with any of these views or simply prefer to test the numbers yourself, you can build a personalised thesis in just a few minutes: Do it your way

A great starting point for your Atkore research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Ready to hunt for your next idea?

If Atkore has sparked new questions for you, do not stop here. The right screener can surface other opportunities you might regret overlooking later.

- Target potential mispricings by scanning companies that look attractively valued on quality and fundamentals through our 52 high quality undervalued stocks.

- Keep an eye on resilience by focusing on companies our models flag with stronger financial footing using the solid balance sheet and fundamentals stocks screener (45 results).

- Spot under-the-radar opportunities before everyone starts talking about them by checking our screener containing 24 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com