- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Simpson Manufacturing (SSD) Valuation After Strong 2025 Results And Positive 2026 Margin Outlook

Why Simpson Manufacturing’s latest results matter for shareholders

Simpson Manufacturing (SSD) just reported its fourth quarter and full year 2025 results, with higher sales and net income year over year, reaffirmed its regular dividend, and shared a supportive margin outlook for 2026.

See our latest analysis for Simpson Manufacturing.

The recent results and dividend affirmation seem to have fed into a strong run in the share price, with Simpson Manufacturing’s 30 day share price return of 9.51% and 90 day share price return of 16.75% adding to a 3 year total shareholder return of 78.98%. This suggests momentum has been building over time.

If Simpson’s update has you thinking about where growth linked to construction and infrastructure might show up next, take a look at 24 power grid technology and infrastructure stocks as a starting list of ideas.

With Simpson’s shares up strongly and the price now slightly above the average analyst target, the key question is whether the current valuation still leaves room for upside or if the market is already pricing in future growth.

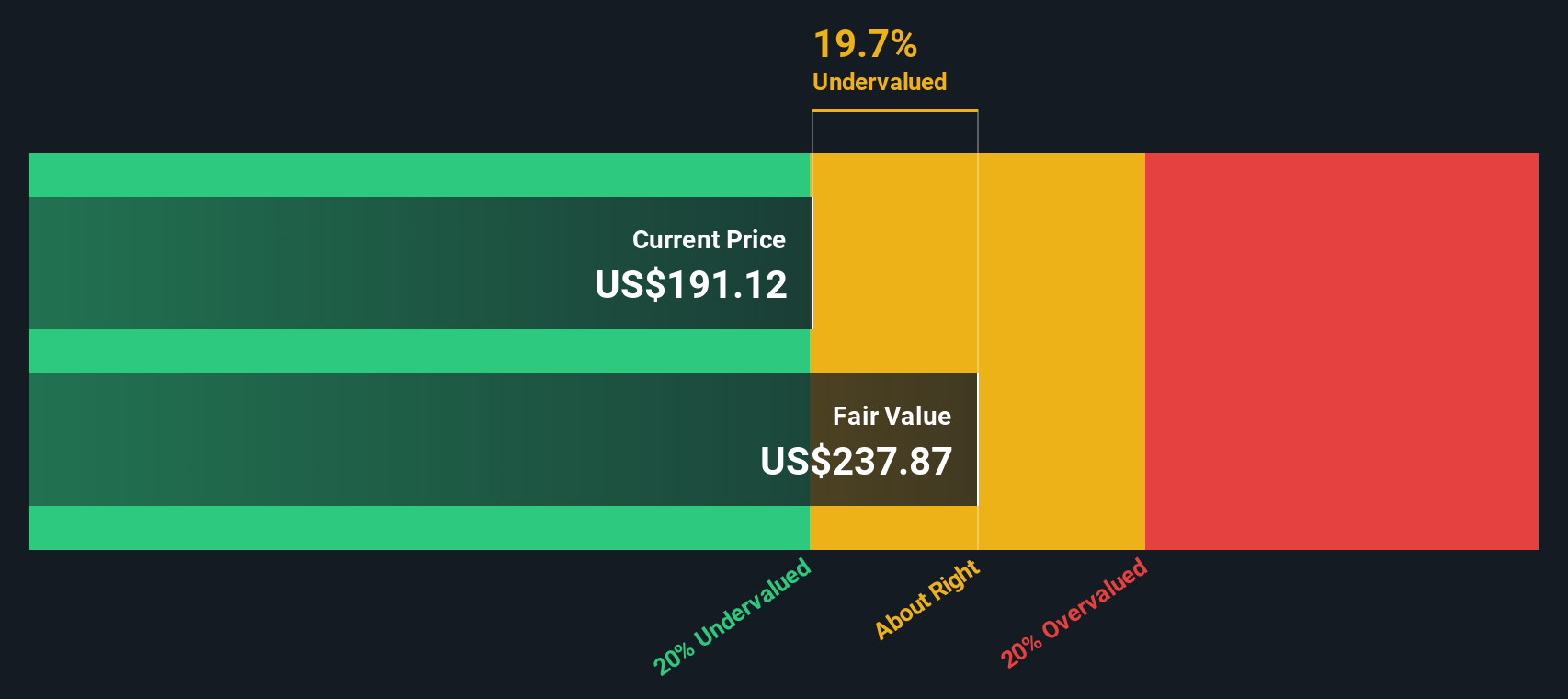

Most Popular Narrative: 1% Overvalued

At a last close of $196.07 versus a most followed fair value estimate of $194.75, Simpson Manufacturing is priced slightly above that narrative anchor, which puts the spotlight on what is driving the long term story.

The accelerating adoption of off-site, modular, and mass timber construction solutions is creating significant demand for high-performance, engineered fasteners and connectors, an area where Simpson continues to see double-digit OEM volume growth and increasing traction with new digital and software solutions. This is likely to support above-market revenue growth.

Curious what kind of revenue and earnings path justifies that fair value, and which profit margin and valuation multiple assumptions sit underneath it? Without seeing all the numbers up front, the full narrative lays out how those moving parts fit together.

Result: Fair Value of $194.75 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still pressure points, including subdued U.S. housing starts and higher steel tariffs, which could limit volumes and squeeze Simpson’s margins if they persist.

Find out about the key risks to this Simpson Manufacturing narrative.

Another Angle on Value

Our DCF model suggests Simpson Manufacturing is trading rich, with the current $196.07 share price above an estimated future cash flow value of $164.10. That contrasts with the earnings based fair value of $194.75. So which set of assumptions do you find more convincing?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Simpson Manufacturing Narrative

If you look at the numbers and come to a different conclusion, or simply prefer to build your own view from scratch, you can quickly set up a custom narrative and stress test your assumptions with Do it your way.

A great starting point for your Simpson Manufacturing research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Simpson has sharpened your thinking, do not stop here. Use the Simply Wall St screener to quickly surface other opportunities that might fit your style.

- Target dependable income by checking out 14 dividend fortresses that may suit investors who want yield with fewer surprises.

- Hunt for value by scanning 52 high quality undervalued stocks where quality fundamentals meet prices that screens flag as attractive.

- Prioritise resilience by reviewing 82 resilient stocks with low risk scores that the system scores as having steadier risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com