- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Commerce Bancshares (CBSH) Valuation After Its Latest Dividend Increase

Commerce Bancshares (CBSH) has drawn fresh attention after its board declared a quarterly dividend of $0.275 per share, a 5% increase that extends the bank's 58 year streak of annual dividend growth.

See our latest analysis for Commerce Bancshares.

At a share price of $55.23, Commerce Bancshares has seen firm near term momentum, with a 7 day share price return of 3.06% and a 90 day share price return of 6.80%, even as the 1 year total shareholder return of 12.31% decline shows that longer term holders have had a softer experience. The dividend increase comes just ahead of the company’s appearance at the Bank of America Financial Services Conference in Miami, which may keep investor focus on how management frames growth plans and risk.

If this dividend news has you rethinking where you hunt for income and stability, it could be a good moment to broaden your search with 22 top founder-led companies as potential long term compounders.

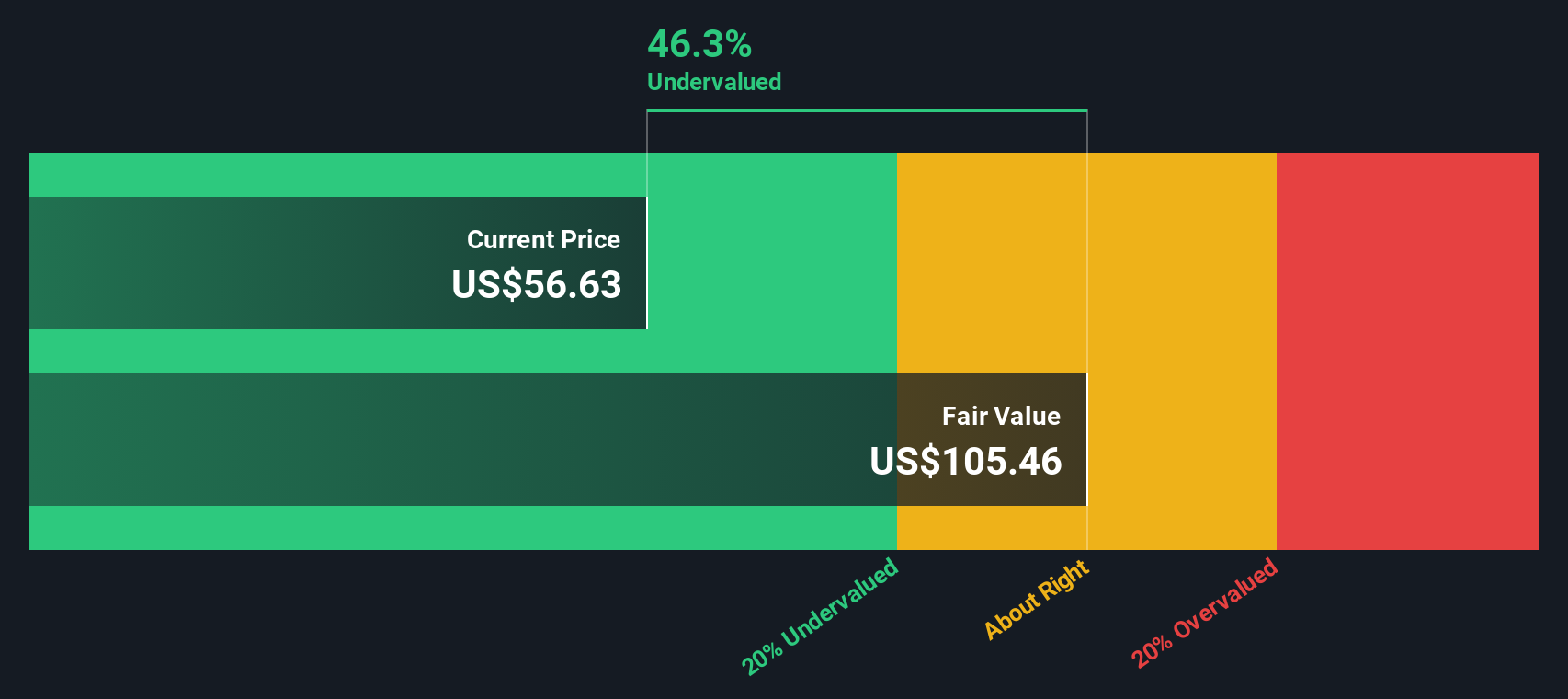

With the shares trading at $55.23 and sitting at a discount to some valuation estimates, you have to ask yourself: is Commerce Bancshares quietly undervalued right now, or is the market already pricing in future growth?

Preferred P/E of 14.4x: Is it justified?

On a P/E of 14.4x, Commerce Bancshares is priced above both the US banks industry average of 12x and the peer average of 13.7x, even though our model flags the shares as trading 42.9% below an internal fair value estimate.

The P/E multiple compares the current share price to earnings, so a higher figure usually means the market is willing to pay more for each dollar of profit. For a bank like Commerce Bancshares, that often reflects views on the quality and stability of earnings, the consistency of its dividend and how investors see its growth profile compared with other lenders.

Here, the market is assigning a richer P/E than both the broader US banks industry and close peers, even though the estimated fair P/E stands lower at 12.4x. If sentiment shifted toward that fair ratio, it would imply a level the valuation could move toward, which matters when you set expectations around how much of Commerce Bancshares’ earnings power is already reflected in the current $55.23 share price.

Explore the SWS fair ratio for Commerce Bancshares

Result: Price-to-earnings of 14.4x (OVERVALUED)

However, the 12.31% decline in 1-year total return and a relatively low value score of 2 signal that sentiment and valuation risk could still cap upside.

Find out about the key risks to this Commerce Bancshares narrative.

Another View: Our DCF Model Paints a Different Picture

While the 14.4x P/E suggests Commerce Bancshares is priced richly against banks at 12x and peers at 13.7x, our DCF model points in the other direction. On that framework, the shares at $55.23 sit below an estimated future cash flow value of $96.71, which could indicate undervaluation. Which lens you rely on may depend on your own hurdle rate and time frame.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Commerce Bancshares for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 52 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Commerce Bancshares Narrative

If you look at these numbers and reach a different conclusion, that is the point. You can dig into the same data and shape your own view in just a few minutes with Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Commerce Bancshares.

Looking for more investment ideas?

If you stop here, you only see part of the opportunity set, so use the screener to size up other ideas that might suit your goals better.

- Target potential mispricings by reviewing our list of 52 high quality undervalued stocks that combine quality fundamentals with more modest expectations baked into the market price.

- Lock in income candidates by focusing on 14 dividend fortresses that pair higher yields with businesses built to keep paying shareholders.

- Prioritise resilience by scanning 82 resilient stocks with low risk scores that our model views as having more durable financial and risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com