- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Flowserve (FLS) Is Up 8.1% After Mixed 2025 Results And Trillium Deal - Has The Bull Case Changed?

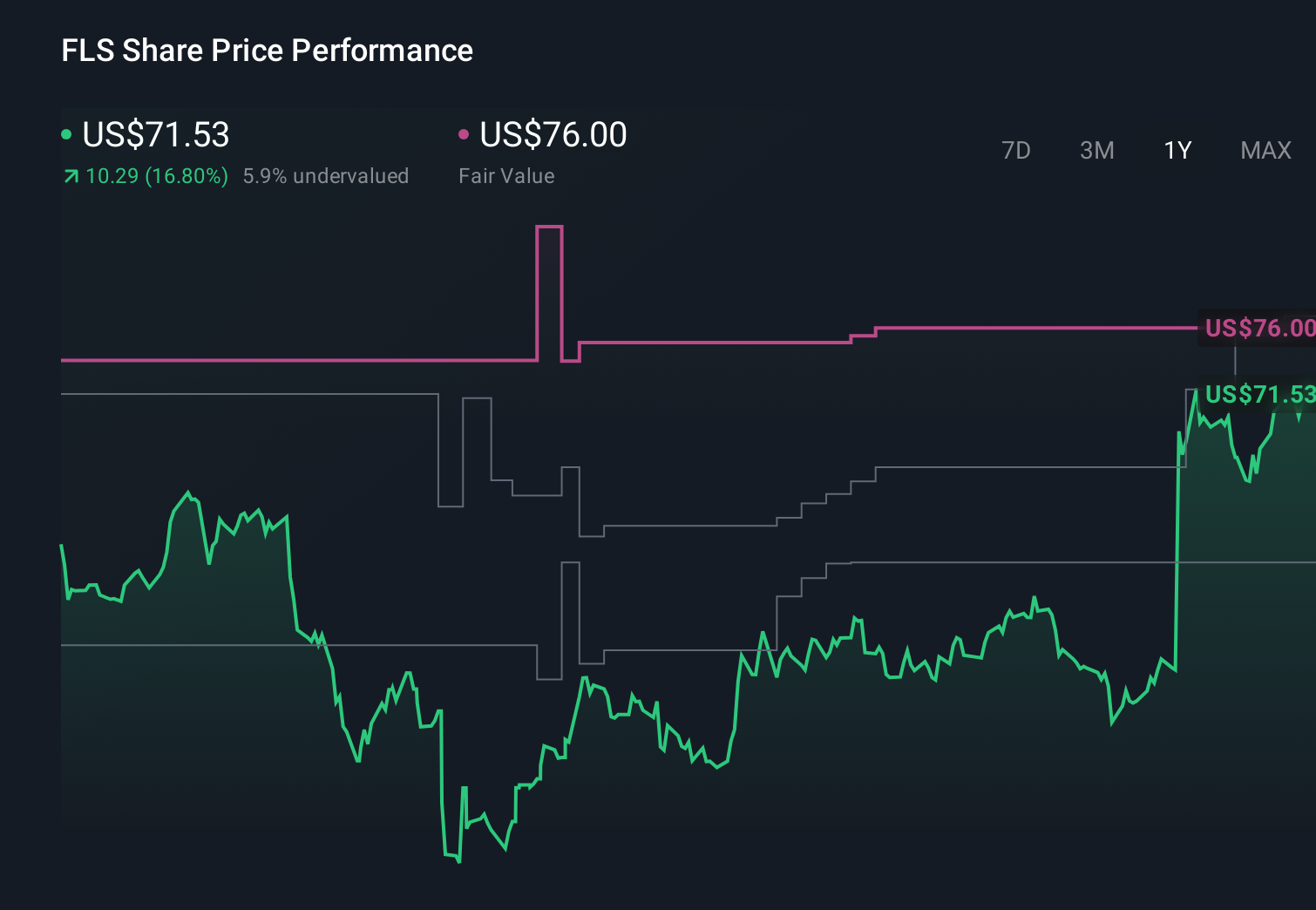

- Flowserve Corporation recently reported fourth-quarter and full-year 2025 results showing higher sales but a quarterly net loss, while issuing 2026 guidance calling for modest organic and total sales growth.

- The company also outlined longer-term margin ambitions and highlighted opportunities in nuclear and power markets, supported by the planned US$490.00 million acquisition of Trillium Flow Technologies’ valves division.

- We’ll now examine how Flowserve’s improved margin trajectory and 2026 profit outlook shape its investment narrative for investors.

Invest in the nuclear renaissance through our list of 87 elite nuclear energy infrastructure plays powering the global AI revolution.

What Is Flowserve's Investment Narrative?

To own Flowserve, you need to be comfortable with a relatively steady, industrial story where margin improvement and disciplined capital allocation matter more than rapid top-line growth. The latest results underline that tension: full-year 2025 earnings were solid and margins improved, but the quarter dipped into a net loss due to large one-off items, and 2026 organic sales guidance of 1% to 3% keeps expectations grounded. The bigger swing factor now is profitability, with management already hitting earlier margin targets and outlining an ambitious 2030 operating margin goal, reinforced by the planned US$490.00 million Trillium valves acquisition and continued strength in nuclear and power-related demand. Short-term, the stock’s sharp move higher and elevated valuation heighten the risk that any integration hiccups, slower project awards or further one-off charges could quickly reset sentiment.

However, investors should be aware that recent insider selling sends a different signal about short term risk. Flowserve's shares have been on the rise but are still potentially undervalued. Find out how large the opportunity might be.Exploring Other Perspectives

Six fair value estimates from the Simply Wall St Community span roughly US$65.63 to US$92, underscoring how differently people read Flowserve’s improved margin outlook and acquisition plans. Some focus on the upside from nuclear and power exposure, while others are more cautious about integration risk and the company’s higher earnings multiple. You can compare these contrasting viewpoints to your own expectations for how resilient Flowserve’s profitability will be through the next few years.

Explore 6 other fair value estimates on Flowserve - why the stock might be worth 23% less than the current price!

Build Your Own Flowserve Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Flowserve research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Flowserve research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Flowserve's overall financial health at a glance.

No Opportunity In Flowserve?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com