- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Impinj (PI) Valuation After Guidance Cut And Sharp Post Earnings Share Price Drop

Impinj (PI) shares came under pressure after Q4 2025 results and first quarter 2026 guidance, as management projected softer revenue and a wider GAAP net loss amid inventory and demand headwinds.

See our latest analysis for Impinj.

The weak Q1 2026 guidance and commentary on inventory reductions appear to have sharply shifted sentiment, with a 1 day share price return of negative 24.57% and a 30 day share price return of negative 44.52%, even though the 5 year total shareholder return of 67.33% still reflects a much stronger longer term result.

If this earnings shock has you reassessing the RFID space, it could be a good moment to see what else is out there by using our screener of 33 AI infrastructure stocks.

With Impinj trading well below recent analyst targets and the business now guiding to weaker near term revenue and a larger loss, you have to ask: is this a reset worth considering, or is the market already discounting future growth?

Most Popular Narrative: 51.9% Undervalued

With Impinj last closing at $116.04 against a widely followed fair value estimate of about $241.11, the narrative is built on ambitious growth and profitability assumptions that go well beyond today’s earnings picture.

Broadening adoption of RFID-enabled supply chain and logistics solutions across both dedicated logistics providers and retailers managing their own supply chains, as customers seek greater resiliency and flexibility in response to tariff-related uncertainties and global supply chain pressures. This drives recurring revenue streams from endpoint ICs and opens up additional enterprise use cases, supporting both top-line and more diversified revenue.

Curious what has to happen for that fair value to make sense? This narrative leans on rapid revenue expansion, rising margins, and a punchy future earnings multiple. The exact mix of those assumptions might surprise you.

Result: Fair Value of $241.11 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this depends on key risks, such as slower RFID adoption in new markets or customer concentration that could cause revenue swings if major apparel or logistics buyers pull back.

Find out about the key risks to this Impinj narrative.

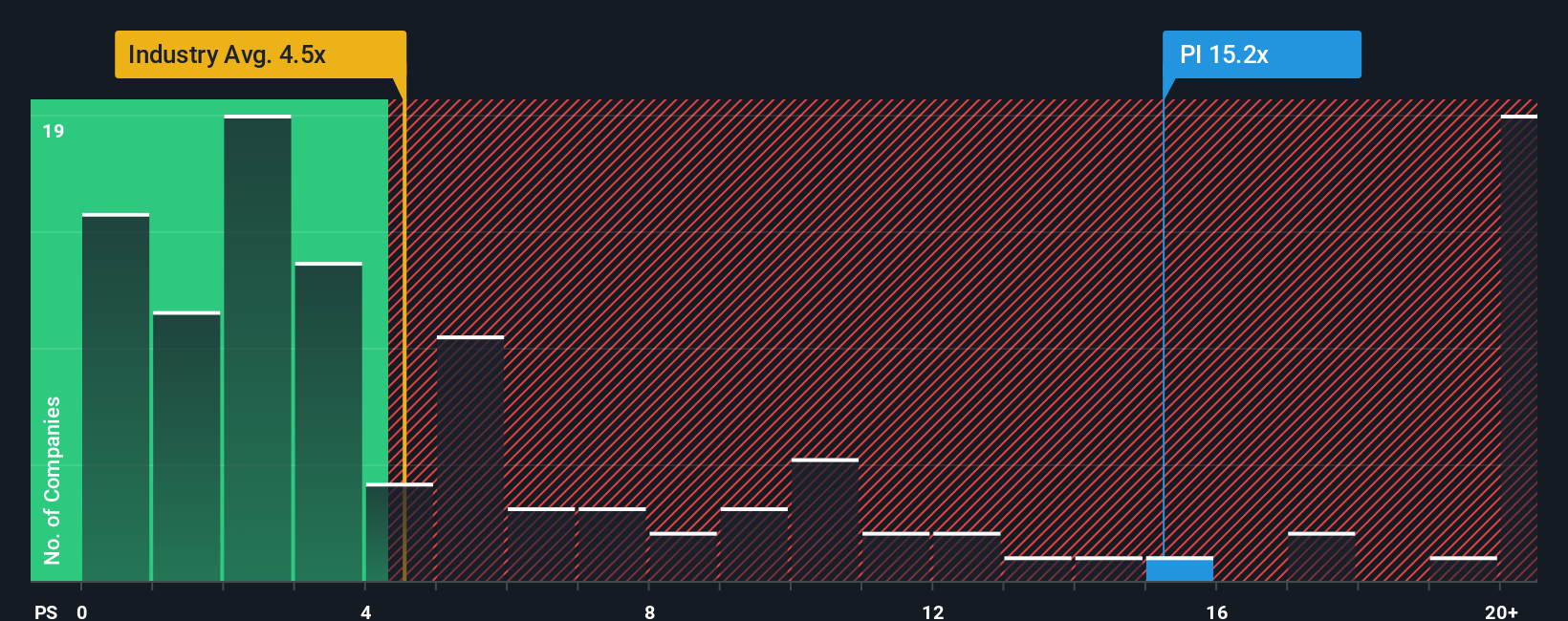

Another View: Price Tag Tension

There is a twist when you look at Impinj through its P/S ratio. At about 9.7x sales, the stock sits well above the US Semiconductor industry at 5.8x and peers at 6.3x, and even above a fair ratio of 8x. That gap suggests investors are already paying up, so it may be worth considering how much cushion is really left.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Impinj Narrative

If you read this and feel the story should look different, you can weigh the same data, frame your own view and Do it your way in just a few minutes.

A great starting point for your Impinj research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Ready to spot your next idea?

Before you move on, build on your momentum by lining up a few fresh ideas so you are prepared when opportunities arise.

- Focus on quality at a discount by scanning our list of 52 high quality undervalued stocks that combine stronger fundamentals with prices that may not fully reflect them.

- Prioritise resilience and stress test your portfolio against a set of 84 resilient stocks with low risk scores that score well on our risk checks.

- Look for potential standouts by combing through a screener containing 24 high quality undiscovered gems that many investors may not be watching yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com