- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Westlake (WLK) Valuation After Mixed Analyst Calls And Mizuho Downgrade

Why recent analyst moves matter for Westlake stock

Mizuho’s decision to shift Westlake (WLK) from an Outperform rating to Neutral, while other firms keep buy calls in place, has put fresh attention on what current prices already reflect.

See our latest analysis for Westlake.

The recent analyst debate comes on the heels of strong short term momentum, with a 4.08% 1 day share price return and a 51.19% 90 day share price return, contrasting with a 1 year total shareholder return decline of 11.26% and a 3 year total shareholder return decline of 18.93%. As a result, recent enthusiasm sits against a more mixed longer term record.

If this kind of mixed performance has you reassessing your watchlist, it could be a good time to scan our screener of 22 top founder-led companies for fresh ideas beyond Westlake.

With Westlake trading around US$95.93, slightly above the average analyst price target of US$85.36 but at an estimated 9% intrinsic discount, you have to ask: is there hidden value here, or is the market already pricing in future growth?

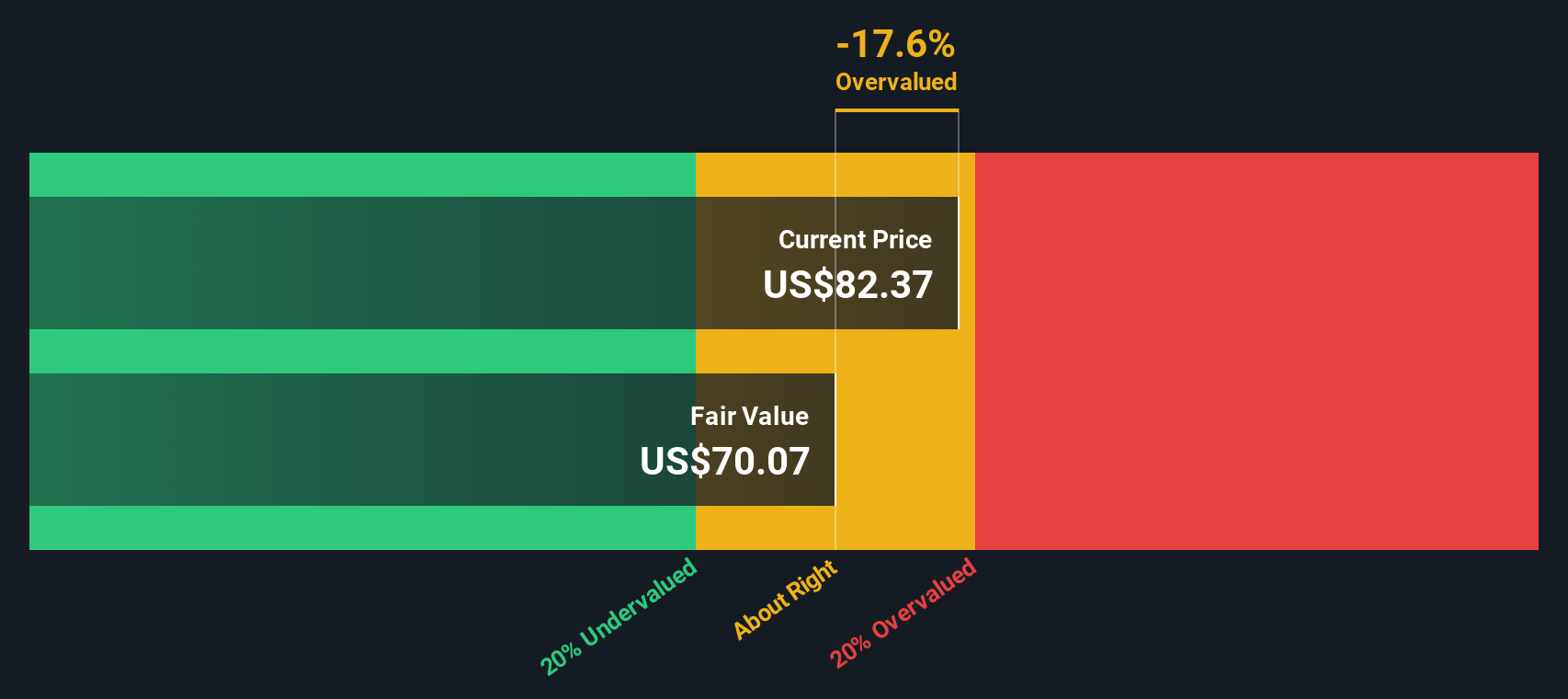

Most Popular Narrative: 12.4% Overvalued

With Westlake last closing at $95.93 against a widely followed fair value view of about $85.36, the current setup hinges on how these planned facility closures reshape future earnings power.

The multi-year increase in municipal infrastructure spending in the U.S., fueled by the Infrastructure Act and ongoing underspend in water infrastructure, is structurally supporting long-term demand for Westlake's HIP (Housing and Infrastructure Products) segment, particularly for PVC pipes and fittings, creating a reliable revenue and volume growth driver unaffected by near-term housing volatility.

Demographic trends and the long-term undersupply of homes are expected to drive a recovery in residential construction, positioning Westlake's balanced exposure to both new construction and repair/remodel markets to benefit from secular urbanization and infrastructure development, leading to sustained mid-single-digit organic HIP revenue growth and high EBITDA margins.

Want to see what is baked into that fair value? The narrative leans on measured revenue growth, firmer margins, and a richer future earnings multiple. Curious which assumptions really carry the valuation?

Result: Fair Value of $85.36 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, those assumptions could be challenged if global chemical oversupply keeps pressuring prices, or if higher North American feedstock and energy costs squeeze margins further.

Find out about the key risks to this Westlake narrative.

Another Take: Market Ratio Tells a Different Story

Our fair value work suggests Westlake trades about 8.9% below the SWS DCF estimate of $105.35, even as the popular narrative frames the stock as 12.4% overvalued against an $85.36 fair value. When cash flow and headline targets disagree this much, which signal should receive more attention?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Westlake Narrative

If you look at the numbers and reach a different conclusion, or simply want to test your own view against the data, you can build a custom thesis in just a few minutes and Do it your way

A great starting point for your Westlake research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Westlake has your attention, do not stop here. Broaden your watchlist with a few focused screens that surface different types of opportunities worth a closer look.

- Target dependable cash generators by checking companies with 14 dividend fortresses that could add steady income to your portfolio mix.

- Hunt for mispriced quality with our 52 high quality undervalued stocks, built to surface companies where fundamentals and current prices look out of sync.

- Control risk first by reviewing the 84 resilient stocks with low risk scores and see which companies score well on stability before you commit fresh capital.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com