- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Aptiv (APTV) Valuation As Versigent Spin Off And Robotics Moves Gain Attention

Guidance and spin off plans reshape the Aptiv story

Aptiv (APTV) has drawn fresh attention after outlining 2026 earnings guidance, advancing the spin out of its lower margin wire harness business as Versigent, expanding robotics partnerships, and continuing an active share repurchase program.

See our latest analysis for Aptiv.

The guidance, spin off plan and buyback activity have come as the share price has moved to US$82.38, with a 1 day share price return of 3.34% and a 7 day share price return of 5.64%, while the 30 day share price return of 7.09% suggests recent momentum has cooled. Over a longer stretch, the 1 year total shareholder return of 28.76% contrasts with 3 year and 5 year total shareholder returns of 26.96% and 47.29% respectively, so recent interest has followed a tougher multi year experience for investors.

If Aptiv's transformation is on your radar, it could be a good moment to widen the lens and check out 28 robotics and automation stocks surfaced by the Simply Wall St screener.

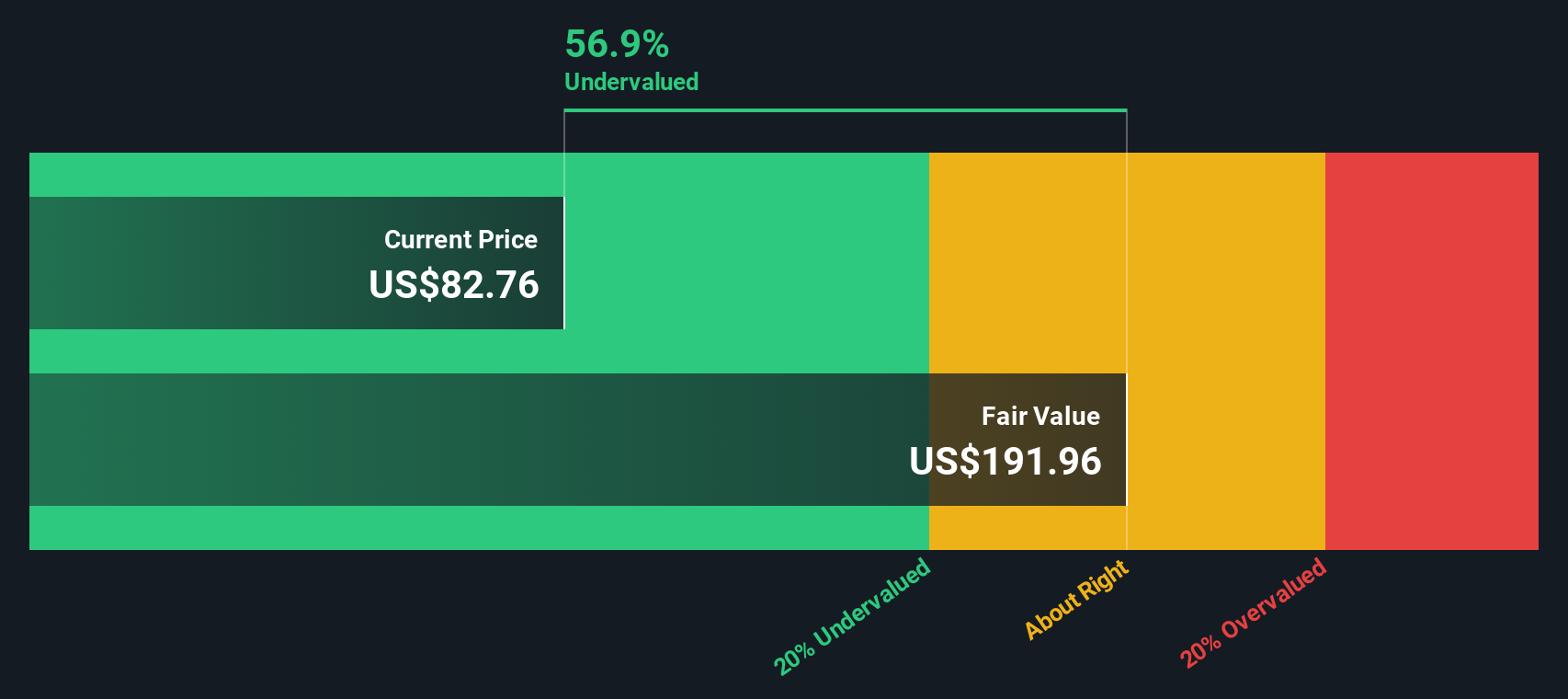

With the stock at US$82.38, analyst targets implying a discount, and an intrinsic value estimate also below the current price, the key question is whether Aptiv is still mispriced or if the market already reflects its next phase of growth.

Most Popular Narrative: 18.3% Undervalued

At a last close of $82.38 against a narrative fair value of $100.81, Aptiv is framed as undervalued, with the story hinging on how its business mix is evolving.

Expansion of non-automotive market bookings, especially in aerospace, defense, and industrial sectors, is resulting in faster growth and higher margins compared to core automotive business, which should structurally improve the company's margin profile and earnings stability over time.

Spin-off of the Electrical Distribution Systems (EDS) business and continued execution on footprint optimization/cost structure initiatives are expected to unlock shareholder value, create balance sheet flexibility, and allow for greater strategic focus on software and high-growth advanced electronics areas, with positive impact on net margins and long-term earnings growth.

Curious what sits behind that value gap? The narrative leans on paired shifts in margins and earnings, plus a lower future earnings multiple. The exact mix might surprise you.

Result: Fair Value of $100.81 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the story could change quickly if vehicle production or EV adoption slows, or if the EDS spin off introduces cost, timing, or balance sheet setbacks.

Find out about the key risks to this Aptiv narrative.

Another angle on valuation

The SWS DCF model suggests a higher value than the narrative fair value. With Aptiv at $82.38 and our DCF estimate at $130.29, the shares screen as significantly undervalued. When two approaches both indicate a value below the current price but by very different amounts, which one would you trust more?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Aptiv Narrative

If you look at the numbers and reach a different conclusion, that is fine. You can build your own view in just a few minutes, Do it your way.

A great starting point for your Aptiv research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Aptiv has you thinking more broadly about your portfolio, do not stop here, the screener can surface other opportunities you might wish you had seen earlier.

- Spot potential value by reviewing 52 high quality undervalued stocks, where the screener highlights companies that combine quality fundamentals with prices that may not fully reflect them.

- Prioritize resilience with 84 resilient stocks with low risk scores, built for investors who want businesses that score well on risk metrics while still offering room for returns.

- Hunt for lesser known opportunities using the screener containing 24 high quality undiscovered gems, focusing on companies that have solid fundamentals but limited attention from the broader market.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com