- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

ZTO Express (ZTO) Is Up 8.9% After Funding Buybacks With Low-Coupon Convertibles - Has The Bull Case Changed?

- In early February 2026, ZTO Express (Cayman) Inc. issued 2025 guidance calling for higher revenues but lower gross profit versus 2024, and completed a US$1.50 billion callable, convertible senior unsecured bond offering due 2031 priced at par with a 0.925% fixed coupon.

- The combination of rising parcel volumes, thinner margins, and using low-coupon convertible debt to fund refinancing, capped calls, and share repurchases adds a complex layer to how investors may assess ZTO’s capital structure and earnings quality.

- Next, we will assess how ZTO’s choice to fund share buybacks with a large low-coupon convertible bond shapes its investment narrative.

The future of work is here. Discover the 28 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

What Is ZTO Express (Cayman)'s Investment Narrative?

To own ZTO, you really need to believe that rising parcel volumes can offset structurally thinner unit economics, and that management will allocate capital sensibly as the market matures. The new 2025 guidance reinforces this tension: management is guiding to solid revenue growth but a drop in gross profit, implying continued price pressure just as the company layers on US$1.50 billion of low-coupon convertible debt. That funding choice amplifies some of the key short term catalysts and risks. Buybacks and capped calls can enhance per-share metrics if operational execution holds up, but the equity overhang from a large convertible and softer margins could weigh on how the market views earnings quality. Recent share price strength suggests investors are still backing the volume story, but the risk-reward mix has clearly shifted.

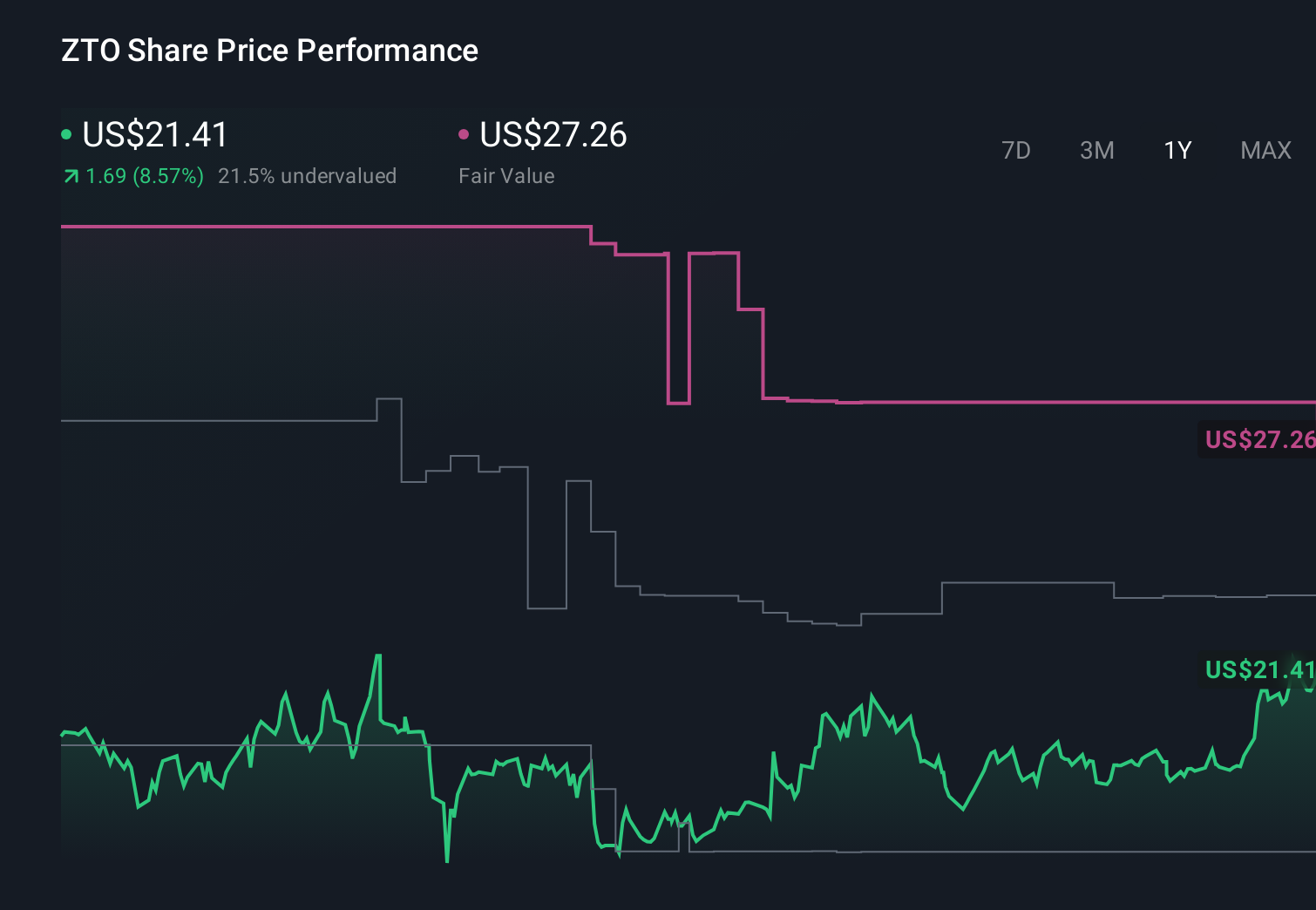

However, one risk in particular may matter more than the headline guidance implies. ZTO Express (Cayman)'s shares have been on the rise but are still potentially undervalued by 44%. Find out what it's worth.Exploring Other Perspectives

Explore 5 other fair value estimates on ZTO Express (Cayman) - why the stock might be worth as much as 78% more than the current price!

Build Your Own ZTO Express (Cayman) Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your ZTO Express (Cayman) research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ZTO Express (Cayman) research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ZTO Express (Cayman)'s overall financial health at a glance.

Curious About Other Options?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 87 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 52 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com