- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Cimpress (CMPR) Valuation Reassessed After Updated Guidance Earnings And Share Buyback

Updated guidance and earnings put Cimpress under the spotlight

Cimpress (CMPR) has moved into focus after updating earnings guidance for fiscal 2026 and 2028, reporting second quarter results, and completing a significant share repurchase tranche that together reshaped how investors view the stock.

See our latest analysis for Cimpress.

After this guidance update and earnings release, Cimpress shares closed at US$75.64, with a 1 day share price return of 2.80% and a 90 day share price return of 15.87%. The 3 year total shareholder return of 104.99% contrasts with a 5 year total shareholder return of 27.89%, suggesting momentum has strengthened more recently than over the longer period.

If this kind of move has your attention, it could be a good time to broaden your watchlist and check out 22 top founder-led companies as potential next candidates to research.

With fresh earnings, long term guidance out to 2028 and a completed buyback now in the mix, the real question is whether Cimpress at about US$76 still offers upside, or if the market is already pricing in future growth.

Most Popular Narrative: 17.3% Undervalued

At a last close of $75.64 against a widely followed fair value estimate of $91.50, Cimpress is framed as undervalued, with that gap resting on some punchy earnings and cash flow assumptions.

Strategic investments in proprietary production technology, customer experience, and manufacturing, well above maintenance levels, are expected to deliver $70-80 million in incremental annualized adjusted EBITDA improvements by FY '27, setting the stage for significant margin expansion and higher operating income in future years.

Curious what has to happen for Cimpress to reach that fair value range? The narrative leans on rising margins, steadier revenue growth, and a different earnings multiple than today. The exact mix of growth, profitability and valuation assumptions is where the real story sits.

Result: Fair Value of $91.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on newer product categories offsetting pressure in legacy print, and on heavy ongoing investment turning into the EBITDA and cash flows that analysts expect.

Find out about the key risks to this Cimpress narrative.

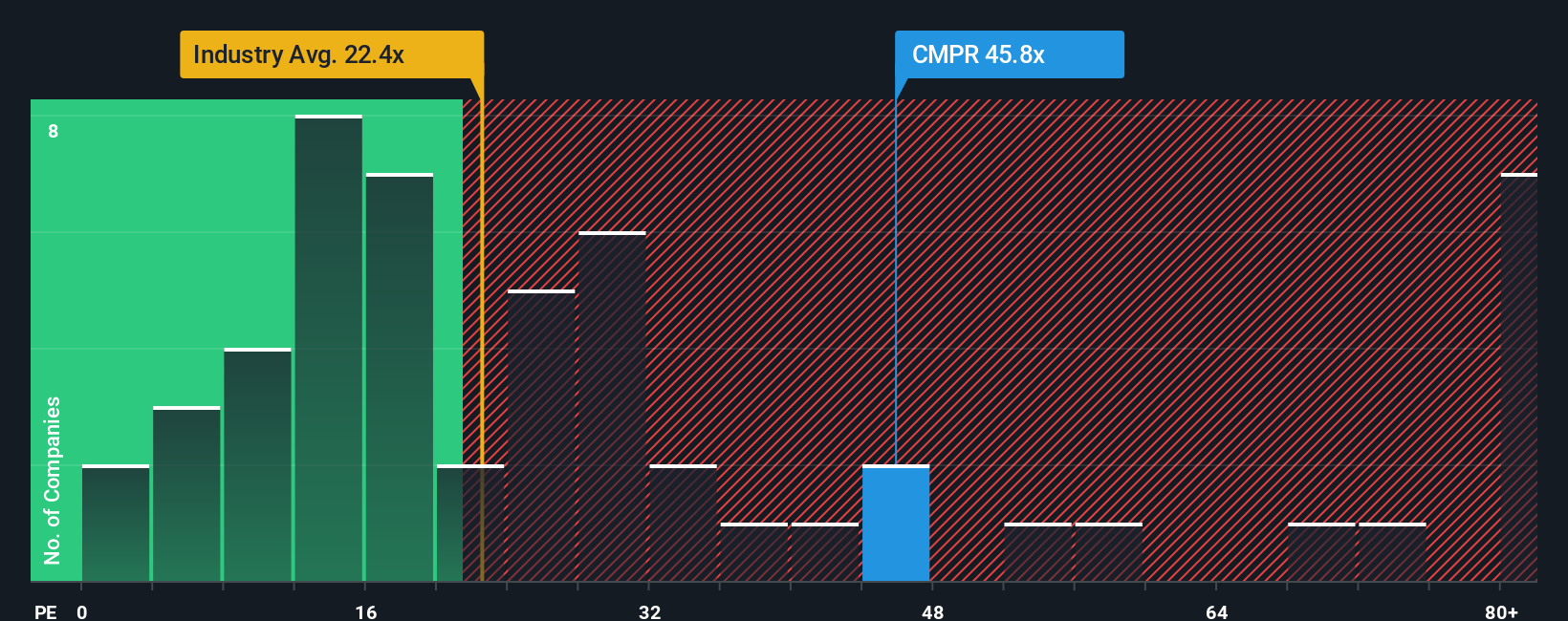

Another angle on valuation

So far the story has leaned on future earnings, margins and cash flows to argue Cimpress looks undervalued. If you just look at today's price tag though, the picture is very different. Cimpress trades on a P/E of 78.4x, while our fair ratio is 32.5x.

That is more than double the Commercial Services industry average of 26.1x and far above the 16.3x peer average, which suggests the market is already paying a rich price for current earnings. The tension for you as an investor is clear: is this a mispricing or a premium that sticks?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Cimpress Narrative

If you are not fully on board with this storyline or simply prefer to lean on your own work, you can spin up a custom view of Cimpress in just a few minutes, then stress test your thesis your way with Do it your way

A great starting point for your Cimpress research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Cimpress has you thinking more broadly about your portfolio, now is a good moment to expand your research and line up your next round of potential ideas.

- Target strong value potential by scanning our 52 high quality undervalued stocks and see which companies currently look attractively priced based on their fundamentals.

- Prioritize resilience by reviewing the 82 resilient stocks with low risk scores so you can focus on businesses with lower risk scores that might better fit a steadier approach.

- Get ahead of the crowd by checking our screener containing 24 high quality undiscovered gems, a curated list that highlights quality companies that may not yet be widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com