- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Calumet (CLMT) Valuation After Extending Its US$500m Asset Based Loan To 2031

Calumet (CLMT) has just reshaped its financing profile by extending its asset based loan facility to January 2031, with commitments of up to $500 million, revised covenants, and room for future inventory financing.

See our latest analysis for Calumet.

The financing update lands against a backdrop of strong recent momentum, with a 30 day share price return of 26.77% and a year to date gain of 28.85%. The 1 year total shareholder return of 55.40% and very large 5 year total shareholder return suggest longer term investors have already seen meaningful upside.

If this shift in Calumet’s financing has you thinking about where else capital intensive energy and infrastructure themes might go next, take a look at our 24 power grid technology and infrastructure stocks as a starting point for finding other ideas.

With the ABL now running to 2031 and the share price already up sharply over the past year, the key question is whether Calumet at about $25 is still mispriced or if the market is already banking on future growth.

Most Popular Narrative: 11.2% Overvalued

Calumet's most followed narrative sets fair value at $22.65, which sits below the recent $25.19 close, so the story now leans toward a richer pricing stance.

The MaxSAF 150 project is on track to start up in the first half of 2026, enabling Calumet to produce 120-150 million annual gallons of sustainable aviation fuel (SAF) at relatively low capital costs, capturing premiums of $1-$2/gallon over renewable diesel and tapping into surging mandated and voluntary SAF demand globally; this is likely to drive material step-up in revenues and EBITDA margin expansion once operational.

Curious how a loss making refiner earns a premium valuation tag? The narrative leans heavily on future earnings, modest top line growth, and a punchy profit multiple.

Result: Fair Value of $22.65 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the narrative could be knocked off course if regulatory support for renewable fuels weakens or if high debt keeps squeezing cash flows and limiting flexibility.

Find out about the key risks to this Calumet narrative.

Another Angle On Valuation

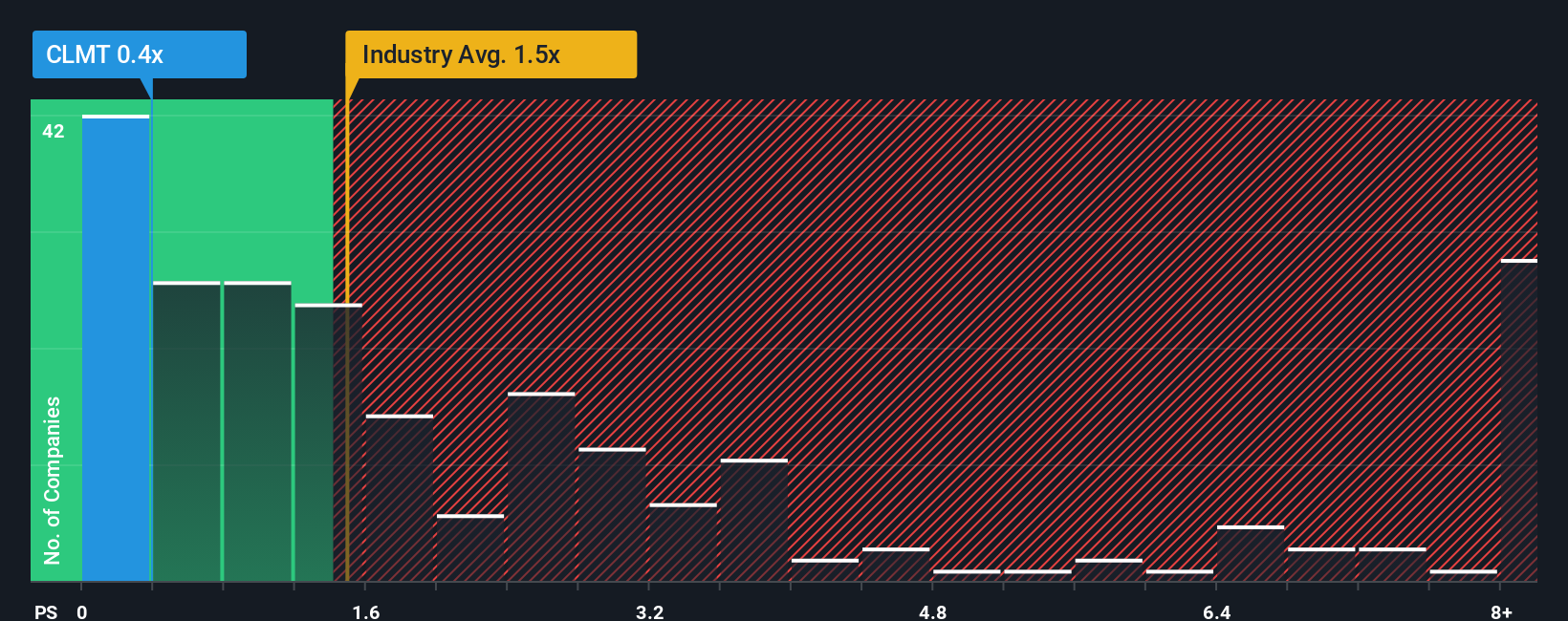

If you look past the narrative fair value of $22.65, the simple P/S picture sends a different signal. Calumet trades on a 0.5x P/S, compared with 1.6x for the wider US Oil and Gas group and 0.2x for its peer set, while our fair ratio sits around 0.6x. That mix of cheaper than the sector, richer than peers and slightly below the fair ratio leaves you asking whether the current price is stretching optimism or still leaving some room.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Calumet Narrative

If you are not fully aligned with this view, or you simply prefer to weigh the data yourself, you can shape a fresh Calumet story in just a few minutes by starting with Do it your way.

A great starting point for your Calumet research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Calumet has sparked your interest, do not stop here. The screener opens up a wider field of opportunities you might be glad you did not overlook.

- Spot potential value plays early by checking our screener containing 24 high quality undiscovered gems that many investors may not be watching yet.

- Prioritise balance sheet strength with the solid balance sheet and fundamentals stocks screener (45 results) to focus on companies that may handle tougher conditions more comfortably.

- Aim for steadier portfolio income by reviewing our 14 dividend fortresses that concentrate on higher yielding payers.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com