- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Ermenegildo Zegna (ZGN) Valuation After Q4 Growth Acceleration And UBS Upgrade

Ermenegildo Zegna (ZGN) is back in focus after reporting unaudited fourth quarter and full year 2025 revenues and receiving an upgrade from UBS, which has drawn fresh attention to the company’s recent operating trends.

See our latest analysis for Ermenegildo Zegna.

The latest unaudited revenue update and the UBS upgrade have come alongside a sharp rebound in sentiment, with a 7 day share price return of 19.56% and a 1 year total shareholder return of 20.47%. This suggests momentum has recently picked up following a softer 30 day share price return of 4.15% and a 3 year total shareholder return of 12.97%.

If this luxury story has caught your attention, it could be a good moment to broaden your watchlist and check out 22 top founder-led companies as potential next ideas to research.

On one hand, Zegna’s share price has already bounced hard on the UBS upgrade and recent Q4 enthusiasm. Yet the stock still trades below the average analyst price target, raising the question: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 10.3% Undervalued

With Ermenegildo Zegna last closing at $10.39 and the most followed narrative pointing to a fair value near $11.58, the current setup reflects a modest implied discount that hinges heavily on how the business executes its growth plans.

The strategic focus on direct-to-consumer (DTC) channels, aimed at increasing brand control, improving gross margins, and enhancing customer experience, is expected to drive long-term revenue growth and improve net margins across the Zegna, Thom Browne, and TOM FORD brands.

Curious what is backing that premium brand story with hard numbers? Revenue pacing, margin rebuild, and future earnings power all sit at the core of this fair value call, and the narrative presents them in a way the share price does not fully mirror yet.

Under this widely followed view, the fair value sits at about $11.58 per share, using a 14.04% discount rate alongside measured assumptions for revenue growth, profit margins, and a future earnings multiple. Together, these inputs suggest the current price implies some cushion if those inputs hold.

Result: Fair Value of $11.58 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are clear pressure points to watch, including ongoing revenue challenges in Greater China and continued double digit declines in Thom Browne wholesale.

Find out about the key risks to this Ermenegildo Zegna narrative.

Another View: Earnings Multiple Sends a Different Signal

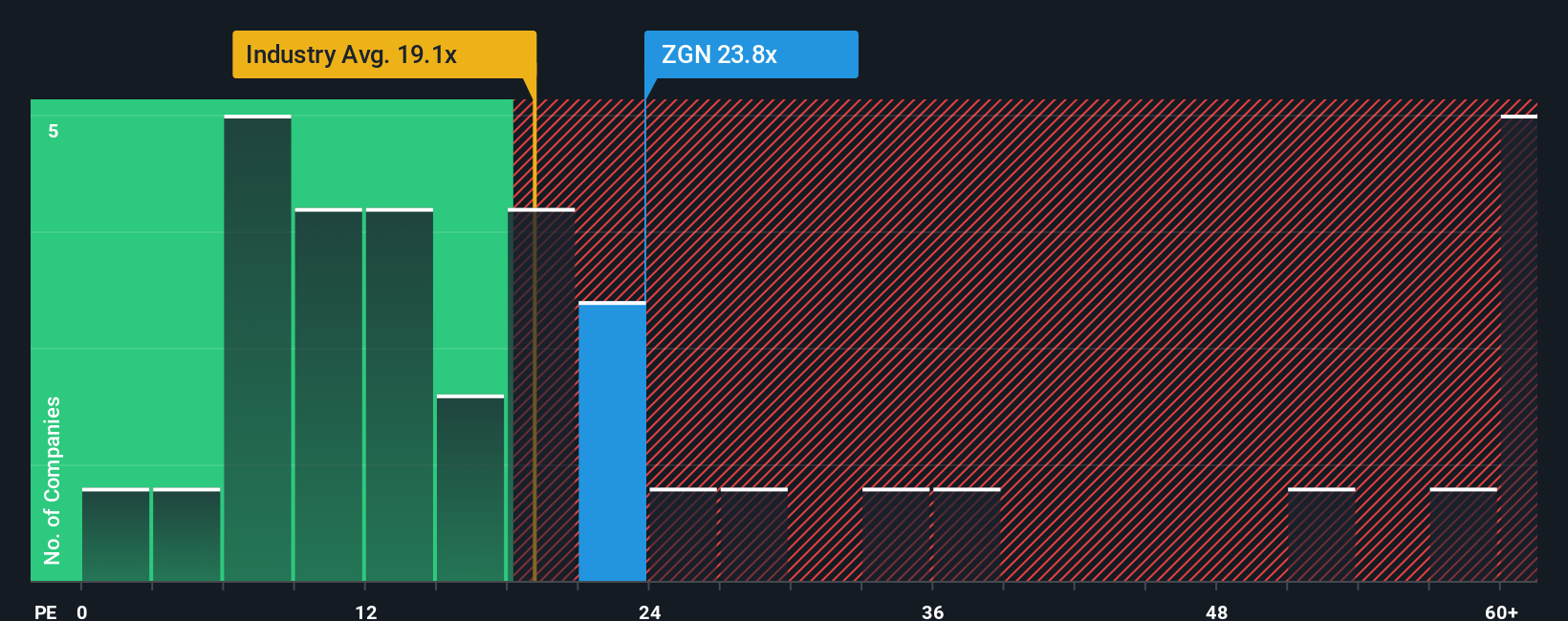

While the narrative fair value of $11.58 points to Zegna as modestly undervalued, the current P/E of 23.5x looks expensive compared with the US Luxury industry at 20.9x and an estimated fair ratio of 16.5x, even though it remains below peers at 36.4x. Is the market pricing in more than the story suggests?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Ermenegildo Zegna Narrative

If you see the numbers differently or simply prefer to stress test your own view, you can build a complete Zegna story yourself in just a few minutes by starting with Do it your way.

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Ermenegildo Zegna.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop with one stock story when a wider set of ideas is right in front of you.

- Power up your bargain hunting by checking companies that screen well as 52 high quality undervalued stocks on quality, price, and fundamentals.

- Strengthen your income stream by reviewing potential 14 dividend fortresses that focus on higher yields with resilience in mind.

- Protect your downside by shortlisting 82 resilient stocks with low risk scores that our checks flag with more measured risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com