- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Carlisle Companies (CSL) Valuation After New Results And 2026 Guidance

Carlisle Companies (CSL) has drawn fresh investor attention after releasing fourth quarter and full year 2025 results, issuing 2026 revenue guidance, and updating its capital returns through share repurchases and a newly affirmed dividend.

See our latest analysis for Carlisle Companies.

The latest earnings release, 2026 revenue guidance and update on buybacks and dividends arrived alongside strong share price momentum. The 7 day share price return of 18.47% and the 90 day share price return of 27.01%, combined with the 5 year total shareholder return of 182.47%, point to a solid longer term outcome and indicate that recent momentum is building on an already strong base.

If Carlisle's recent move has you thinking about where else capital equipment exposure or industrial demand could show up, it may be worth scanning our list of 24 power grid technology and infrastructure stocks as another angle on infrastructure related opportunities.

With Carlisle trading around US$403.86 and sitting close to recent highs after years of strong total returns, the key question now is whether the current valuation still leaves room for further upside or if the market is already pricing in future growth.

Most Popular Narrative: 8.8% Overvalued

At $403.86, Carlisle sits above the most followed fair value estimate of $371.25, which frames the recent price strength in a different light.

Continued investment in automation, digital transformation, and operational efficiency programs (e.g., Carlisle Operating System) are driving productivity improvements and significant cost savings, expected to result in at least 200+ basis points of long-term margin expansion for underperforming segments, positively impacting net margins and free cash flow.

Curious how modest revenue growth, higher margins and a lower future P/E than peers still point to that fair value? The full narrative lays out a tightly argued earnings path, share count assumptions and discount rate choice that all have to line up. If you want to see exactly which forecasts need to hold for this pricing gap to make sense, the details are waiting in that narrative.

Result: Fair Value of $371.25 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on resilient reroofing demand and smooth execution of cost savings programs, while softer construction activity or limited pricing power could easily pressure margins and earnings.

Find out about the key risks to this Carlisle Companies narrative.

Another Angle on Valuation

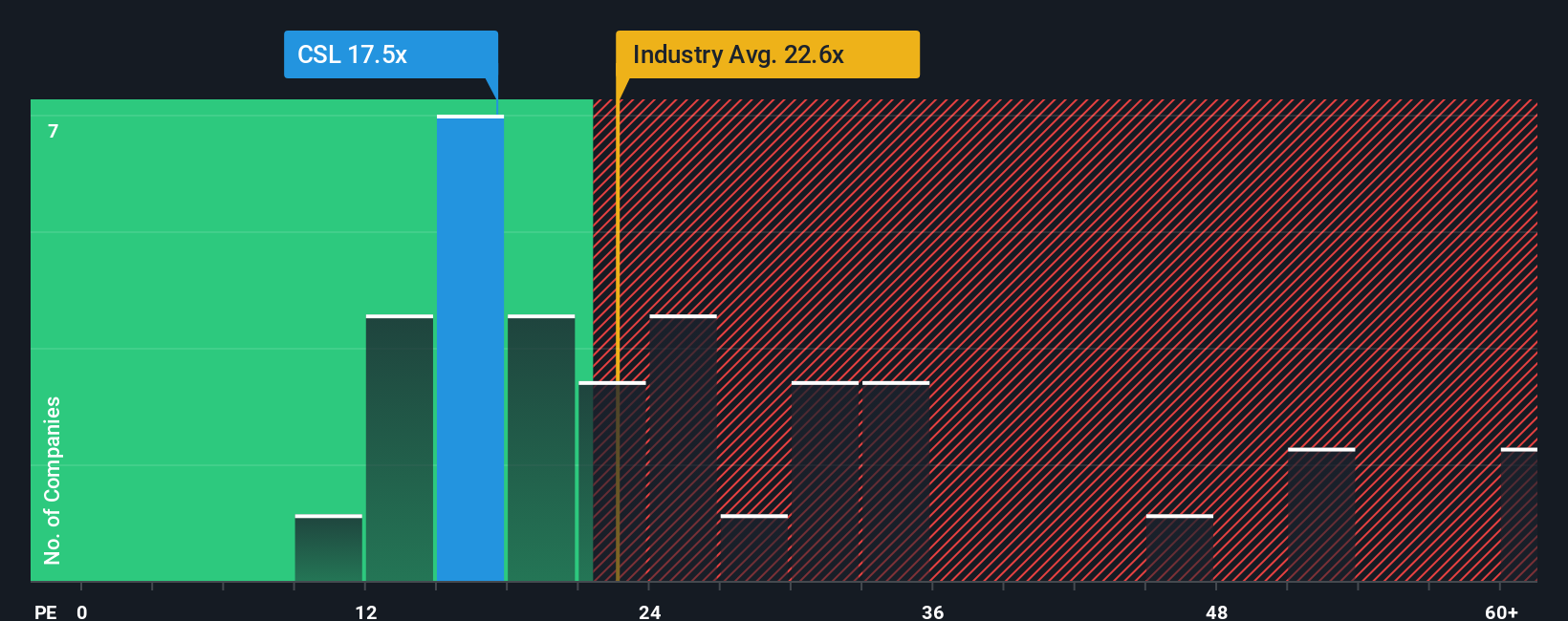

That narrative fair value of US$371.25 paints Carlisle as 8.8% overvalued, but the simple P/E story looks a bit different. At 22.7x earnings, the shares sit slightly below the US Building industry on 22.9x and below peers on 23.7x, while our fair ratio points to 25.7x.

In plain terms, the current price lines up with a small premium to the narrative model but a discount to where the fair ratio suggests the market could settle over time. For you, the question is which set of assumptions feels more realistic when growth, debt and cyclicality are all in the mix?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Carlisle Companies Narrative

If you are not on board with this view or prefer to work from your own numbers, you can stress test the assumptions and Do it your way in under three minutes.

A great starting point for your Carlisle Companies research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Carlisle feels fully priced or you just want fresh angles for your watchlist, it is worth widening the net with a few focused stock ideas.

- Start with value and see which companies our screener flags as 52 high quality undervalued stocks based on a blend of quality fundamentals and pricing.

- Zero in on reliability by checking out 82 resilient stocks with low risk scores, highlighting businesses with lower risk scores that may help steady your portfolio.

- Hunt for less crowded opportunities using our screener containing 24 high quality undiscovered gems that surface quality names many investors might be overlooking.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com