- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Honest Company (HNST) Valuation After Hydrorich Cream Skincare Launch

Hydrorich Cream launch and why Honest Company (HNST) is back on investors’ radars

Honest Company (HNST) just expanded its skincare lineup with Hydrorich Cream, a new moisturizer aimed at dry and extra dry skin, and investors are asking what this means for the stock.

See our latest analysis for Honest Company.

Hydrorich Cream arrives at a time when Honest Company’s short term trading has been choppy, with a 7 day share price return of 7.29% decline and a 30 day share price return of 11.24% decline. The 1 year total shareholder return of 60.99% decline signals that longer term momentum has been under pressure despite the current US$2.29 share price.

If Hydrorich Cream has you thinking about where else product driven stories could come through, it may be worth scanning our list of 22 top founder-led companies as a starting point.

With the share price weak over 1 year and analyst targets sitting higher than the current US$2.29 level, the real question is whether Honest is quietly undervalued or if the market is already pricing in future growth.

Most Popular Narrative: 40.8% Undervalued

The most followed narrative on Honest Company currently points to a fair value of $3.87 per share, compared with the latest $2.29 close, which is what sits behind the current undervaluation debate.

Expanding distribution and shelf presence, particularly in underpenetrated retailers and new store aisles (e.g., Whole Foods, Sprouts, HEB, Target specialty sets), represents a significant runway for top-line growth, supported by management's assessment that Honest is in less than 50% of addressable stores.

Read the complete narrative. Read the complete narrative.

Want to see what is baked into that fair value? The narrative leans heavily on steadier margins, modest revenue momentum, and a richer future earnings multiple that sits well above typical sector levels. The exact mix of growth, profitability and discount rate assumptions might surprise you.

The narrative applies a discount rate of 7.43% to Honest Company, using it to bring projected cash flows and earnings back to today's terms. It leans on expectations for earnings growth, a higher profit margin profile over time, and a future P/E that is materially above the wider US Personal Products group, while still treating Honest as a relatively early stage branded consumer business with room to scale.

Result: Fair Value of $3.87 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, weaker recent results and tariff exposure, including expected gross tariff costs in 2025, could challenge the margin and earnings story behind that fair value.

Find out about the key risks to this Honest Company narrative.

Another View on Honest’s Valuation

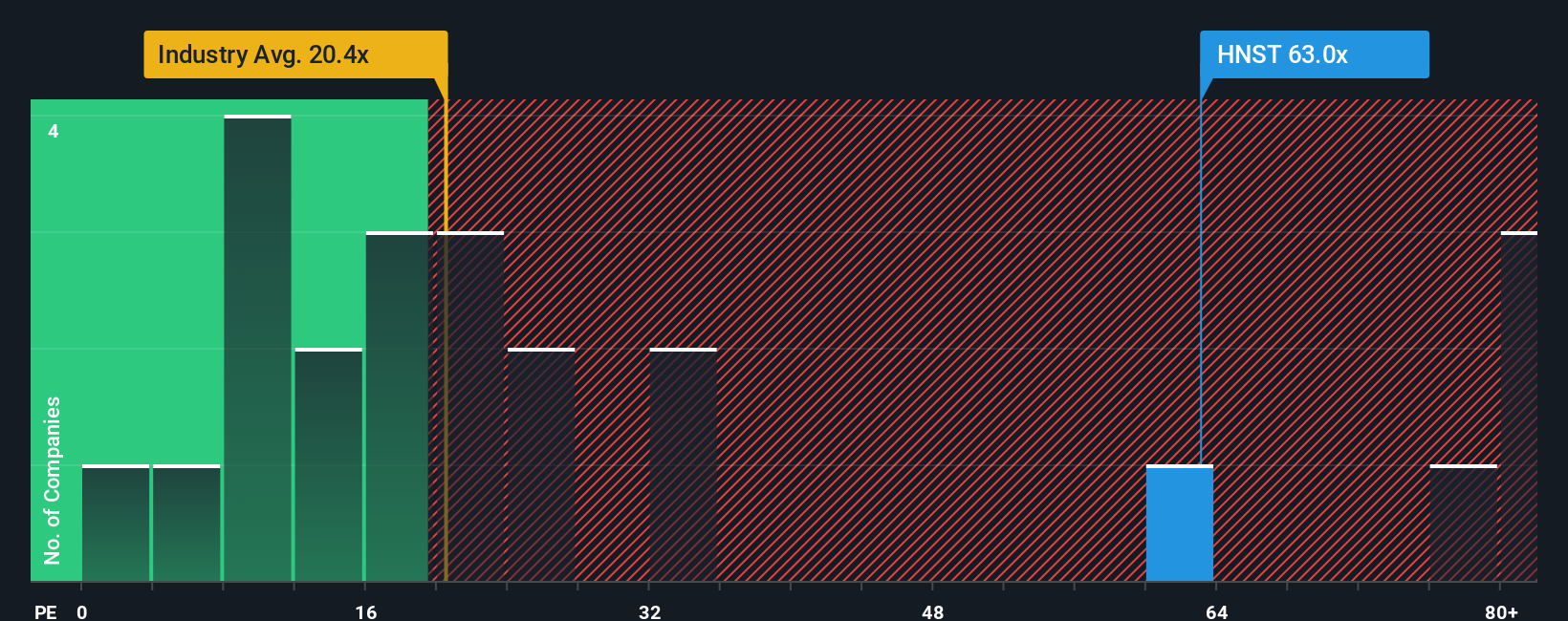

The fair value narrative suggests Honest looks 40.8% undervalued at $2.29, but the earnings multiple paints a tougher picture. The current P/E of 36.2x sits well above both the 14.9x fair ratio and the 22x North American Personal Products average, even though it is below the 62.8x peer average.

That gap to the fair ratio points to potential valuation risk if sentiment cools, while the discount to peers indicates some investors may already be pricing in caution. Which reference point do you think the market is most likely to converge toward over time?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Honest Company Narrative

If you see the numbers differently or just prefer to work from your own assumptions, you can easily build a fresh thesis in minutes: Do it your way.

A great starting point for your Honest Company research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Honest has sparked your curiosity, do not stop here. Use the Simply Wall St Screener to quickly spot other opportunities that fit your own checklist.

- Spot potential value opportunities early by scanning our list of 52 high quality undervalued stocks that combine quality fundamentals with appealing pricing signals.

- Prioritise resilience by running through 82 resilient stocks with low risk scores focused on companies with lower overall risk scores and steadier business profiles.

- Hunt for under the radar names by checking the screener containing 24 high quality undiscovered gems that may not yet be widely followed but still show solid underlying metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com