- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

The Bull Case For Avista (AVA) Could Change Following New 100 MW Battery Storage Plan - Learn Why

- In January 2026, Avista announced it had selected a mix of new resources, including natural gas turbine upgrades, a 100 MW battery storage project, a Montana wind power purchase agreement and expanded demand response programs, to meet long-term reliability, customer demand and clean energy goals outlined in its 2025 Electric Integrated Resource Plan.

- This portfolio-style approach, which combines generation, storage and customer-side demand response, highlights Avista’s effort to balance reliability with decarbonization across its service territory.

- We’ll now examine how Avista’s planned 100 MW battery energy storage system could influence the company’s broader investment narrative.

We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

What Is Avista's Investment Narrative?

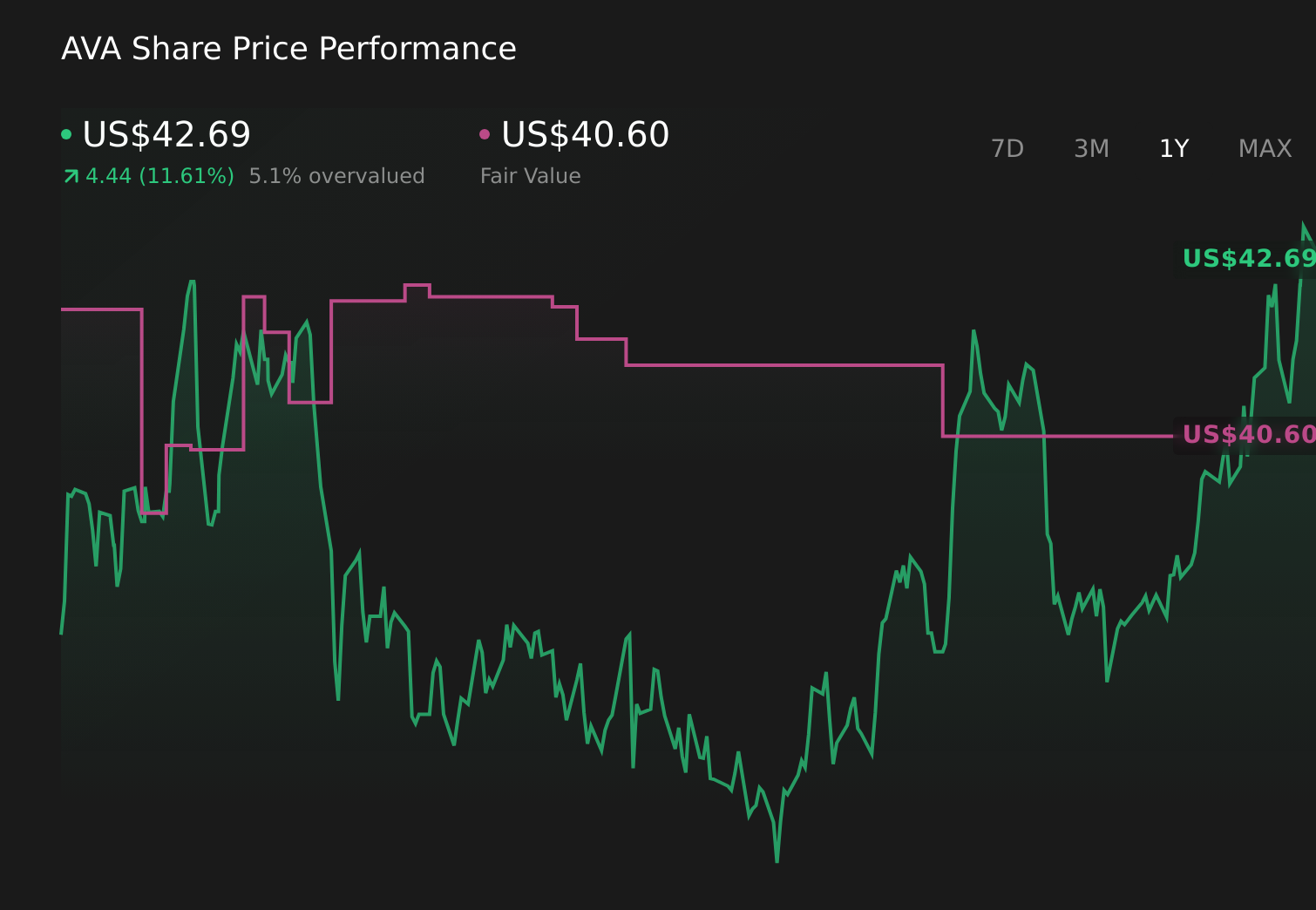

For Avista, you really have to believe in the long game of a regulated utility steadily investing in its grid while trying to keep earnings and dividends on a reasonably stable track. The new resource plan decisions, including the 100 MW battery project and Montana wind PPA, slot into that story by clarifying Avista’s capital spending and clean energy roadmap, but they are unlikely to shift the near term earnings guidance or the key catalysts around rate cases, regulatory decisions and quarterly results. The bigger swing factors still look like dividend sustainability given pressured free cash flow, modest expected earnings growth versus the wider market, and balance sheet flexibility as interest costs remain a constraint. The January announcement mostly reframes risk toward execution and regulatory recovery of these new projects rather than changing the investment thesis outright.

However, one key risk here is how regulators ultimately treat the cost recovery on these new projects. Avista's shares are on the way up, but they could be overextended by 10%. Uncover the fair value now.Exploring Other Perspectives

Explore 2 other fair value estimates on Avista - why the stock might be worth 9% less than the current price!

Build Your Own Avista Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Avista research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Avista research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Avista's overall financial health at a glance.

Searching For A Fresh Perspective?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Outshine the giants: these 30 early-stage AI stocks could fund your retirement.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 28 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com