- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Proto Labs (PRLB) Margin Improvement Tests Bullish High P/E Narrative

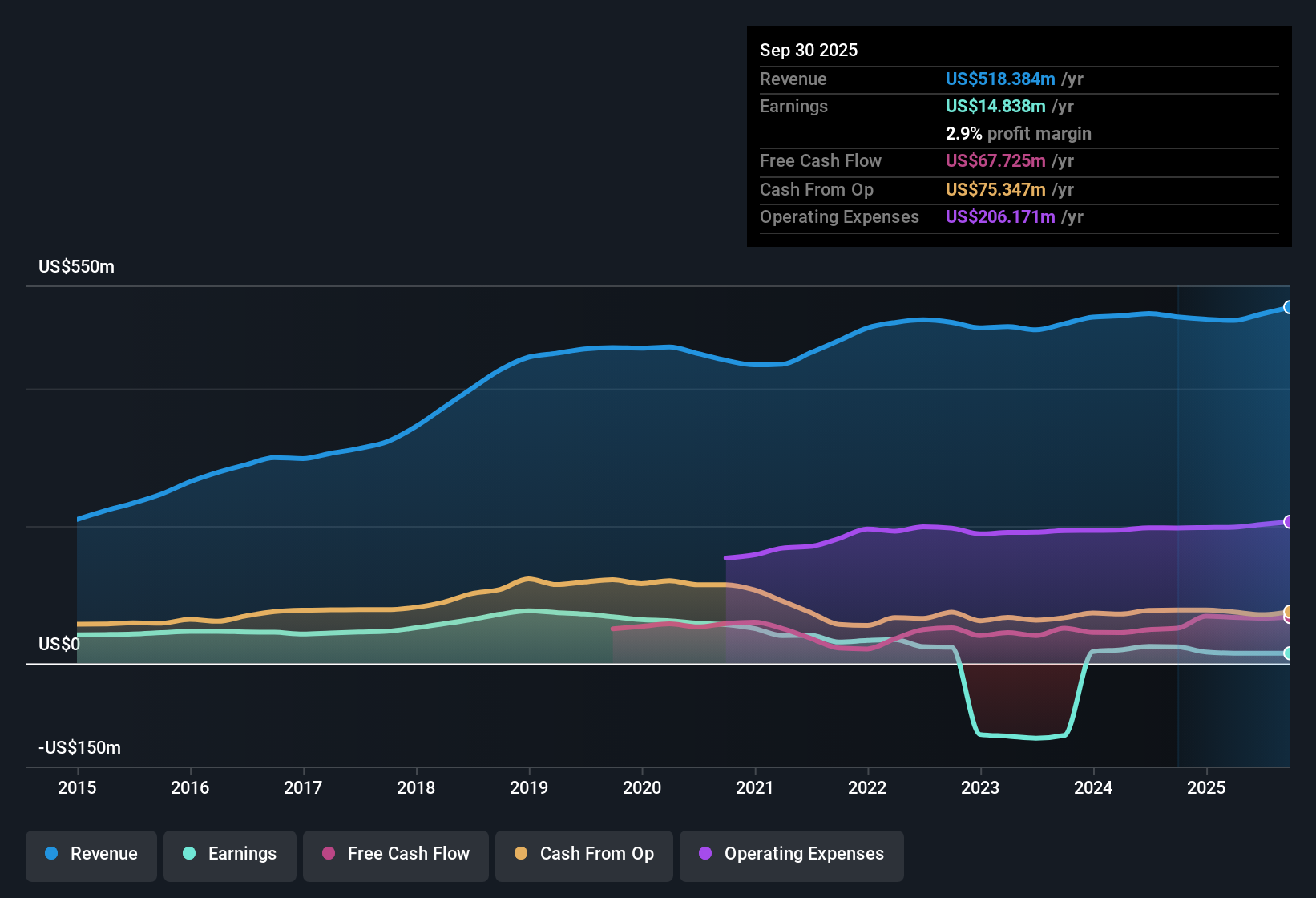

Proto Labs (PRLB) has wrapped up FY 2025 with Q4 revenue of US$136.5 million and basic EPS of US$0.25, capping off a year in which trailing twelve month revenue reached US$533.1 million and EPS came in at US$0.89. Over the past year, revenue has moved from US$500.9 million to US$533.1 million on a trailing basis while EPS shifted from US$0.66 to US$0.89, and quarterly revenue has stepped up from US$121.8 million in Q4 2024 to US$136.5 million in Q4 2025. For investors, the key storyline now is how the 4% trailing net margin and faster earnings growth versus revenue shape the risk and reward trade off around Proto Labs’ latest results.

See our full analysis for Proto Labs.With the headline numbers on the table, the next step is to see how this mix of revenue growth, EPS momentum and margin profile lines up against the widely followed bull and bear narratives around Proto Labs.

Curious how numbers become stories that shape markets? Explore Community Narratives

6.6% Revenue Growth Versus 28% Earnings Lift

- Over the last 12 months, Proto Labs grew revenue by 6.6% annually while earnings rose 28%, with trailing net income of US$21.2 million on US$533.1 million of revenue.

- What stands out for a bullish view is that earnings growth and a 4% net margin sit alongside modest top line growth, which raises questions about how much of that 28% earnings lift comes from operational efficiency versus factors that may not repeat.

- Bulls can point to the trailing margin moving from 3.3% to 4% and TTM EPS of US$0.89 as signs that profitability per dollar of revenue is improving.

- At the same time, the 6.6% revenue growth rate, which is below the 10.2% US market benchmark, means the bullish case leans heavily on sustaining this earnings and margin profile rather than rapid sales expansion.

Premium P/E Of 74.9x Sets A High Bar

- The shares trade on a trailing P/E of 74.9x compared with 27.9x for the US Machinery industry and 35x for peers, and the current price of US$67.17 sits above both the DCF fair value of US$41.14 and the US$61.67 analyst target.

- Critics highlight that this premium valuation leans on the recent 28% earnings growth and forecast ~26.7% annual earnings growth, so any slowdown versus those figures could matter quickly for a bearish view.

- The gap between the share price of US$67.17 and the DCF fair value of US$41.14, plus the discount to the US$61.67 target, suggests the market is currently paying more than both modelled cash flows and that target would indicate.

- Set against five year earnings that declined on average by 9.6% per year, the current 74.9x P/E challenges bears to decide whether the latest 12 month rebound fully resets that longer history or simply coexists with it.

Quarterly Profitability Steadies Around 4% Margin

- On a trailing basis, Proto Labs earned US$21.2 million of net income on US$533.1 million of revenue, giving a 4% net margin that is higher than the 3.3% margin reported a year earlier, while quarterly net income moved from a loss of US$0.4 million in Q4 2024 to US$6.0 million in Q4 2025.

- What is interesting for a balanced view is that this 4% margin and the step from a Q4 loss to a Q4 profit sit alongside a five year earnings decline rate of 9.6% per year, so recent profitability has to be weighed against that longer record.

- The latest four reported quarters in FY 2025 show positive net income in each period, ranging from US$3.6 million to US$7.2 million, which contrasts with the small loss in Q4 2024.

- However, the trailing EPS path in the last six TTM data points moves between roughly US$0.61 and US$0.94 before landing at US$0.89, which shows progress but not a straight line up, something long term holders may pay close attention to.

For a fuller context around where this leaves the stock and how different investors are framing the story, it is worth looking at a broader, balanced narrative on Proto Labs, not just the latest numbers. 📊 Read the full Proto Labs Consensus Narrative.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Proto Labs's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Proto Labs combines 6.6% revenue growth and a 4% net margin with a 74.9x P/E and a history of five year earnings decline.

If that mix of slower top line progress and a rich earnings multiple makes you uneasy, put some alternatives on your radar with 53 high quality undervalued stocks today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com