- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Columbia Sportswear (COLM) Valuation Check After Earnings Beat And Upbeat 2026 Growth Guidance

Columbia Sportswear (COLM) is back in focus after its latest quarterly update, where earnings and profitability came in ahead of Wall Street estimates and 2026 guidance pointed to growth in both net sales and earnings.

See our latest analysis for Columbia Sportswear.

The earnings beat and upbeat 2026 guidance helped spark a sharp shift in sentiment, with a 1 day share price return of 3.27% and a 90 day share price return of 22.06%. However, the 1 year total shareholder return is still negative at 18.85%, so recent momentum contrasts with weaker longer term results.

If this rebound in Columbia Sportswear has you looking for other potential opportunities, it could be a good time to scan 22 top founder-led companies as a fresh source of ideas.

With Columbia trading close to both its analyst target and an intrinsic value estimate, and showing a mixed record of short term gains alongside longer term losses, the key question for you is whether there is still a buying opportunity here or whether the market is already pricing in potential future growth.

Most Popular Narrative: 9.6% Overvalued

Columbia Sportswear's most followed valuation narrative pegs fair value around $57.57, which sits below the recent close of $63.07. This sets up a cautious debate about what the market is currently paying for.

Rising input and compliance costs, along with tariff uncertainty and climate impacts, threaten margins and earnings visibility while increasing inventory and revenue risks. Ongoing climate change and global warming trends are expected to reduce demand for cold-weather outerwear, Columbia's core segment, thus creating structural headwinds for future revenue growth and increasing risk of inventory markdowns or mismanagement.

Curious how a relatively modest revenue outlook, thinner projected margins and a richer future earnings multiple still support that fair value number and price path? The full narrative lays out the chain of assumptions that connects today’s earnings base, future share count and required return into one cohesive valuation story.

Result: Fair Value of $57.57 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, strong execution in international markets or a successful push in digital channels could challenge this cautious view and support a more constructive earnings path.

Find out about the key risks to this Columbia Sportswear narrative.

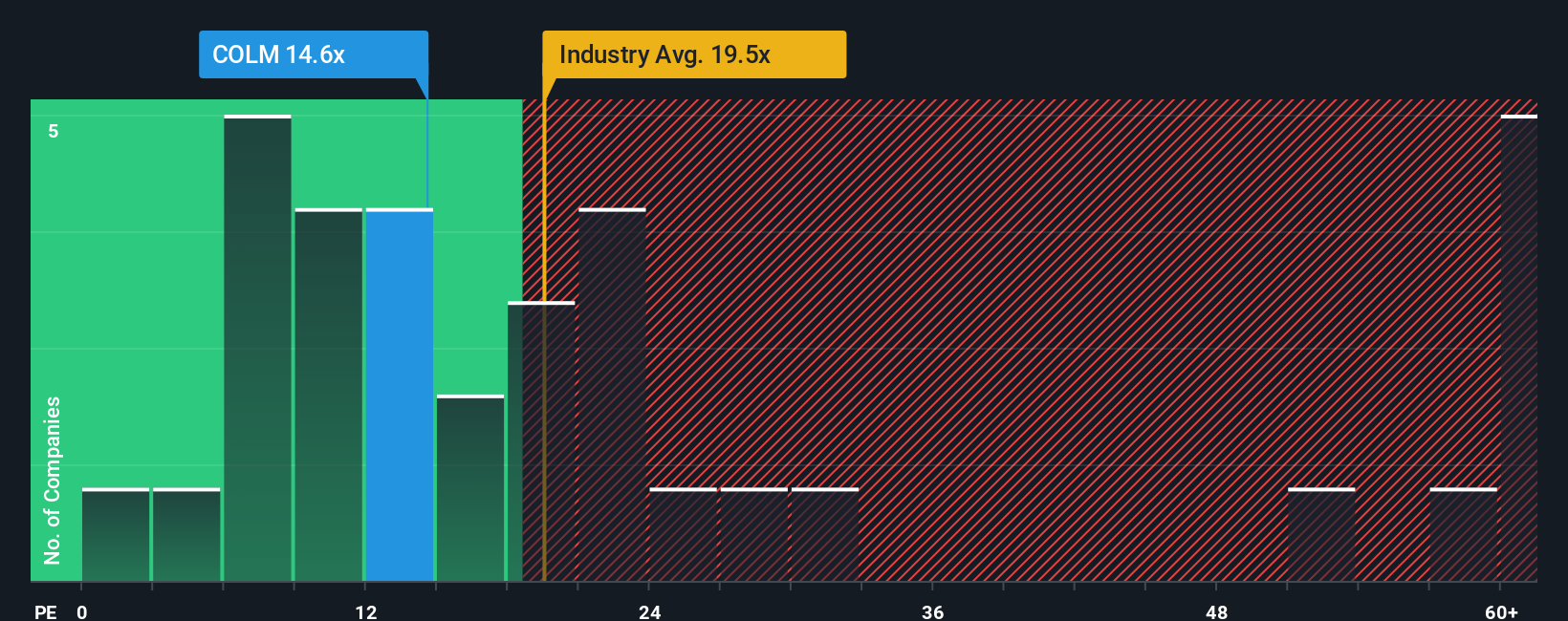

Another Take: Multiples Paint a Different Picture

The narrative flags Columbia Sportswear as about 9.6% overvalued versus a fair value of $57.57. However, the current P/E of 19.2x sits below the US Luxury industry at 20.7x and far below peers at 37.4x, even though it is above a fair ratio of 14.3x. That mix of discount and premium leaves you weighing whether this is valuation risk or a possible entry point if expectations reset again.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Columbia Sportswear Narrative

If you are not fully on board with this view or simply prefer to test the numbers yourself, you can build a custom Columbia Sportswear story in just a few minutes using our tools: Do it your way.

A great starting point for your Columbia Sportswear research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you stop with just Columbia, you risk missing other opportunities that fit your style, goals and risk comfort, so keep widening your opportunity set.

- Spot potential value opportunities early by scanning 53 high quality undervalued stocks that pair quality fundamentals with prices that may not fully reflect those characteristics yet.

- Prioritise resilience by reviewing 86 resilient stocks with low risk scores so you can focus on companies that score well on key risk checks.

- Hunt for under followed stories with strong numbers using our screener containing 24 high quality undiscovered gems and see which businesses stand out on quality and financial strength.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com