- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Bread Financial Holdings (BFH) Valuation After Strong 2025 Earnings Update

Why the latest earnings matter for Bread Financial

Bread Financial Holdings (BFH) has drawn increased investor attention after reporting higher net income and earnings per share for the fourth quarter and full year 2025 compared with the prior year.

See our latest analysis for Bread Financial Holdings.

The earnings release and recent dividend declarations have come alongside a 90 day share price return of 25.09% and a 1 year total shareholder return of 30.13%. The 3 year total shareholder return of 106.57% points to strong longer term momentum from current levels.

If Bread Financial’s move has you thinking about where else growth stories might be forming around payments and data, it could be worth scanning 22 top founder-led companies as a fresh source of ideas.

With Bread Financial trading near US$79.53, carrying a high value score of 5 and an implied 37% intrinsic discount, you have to ask: is this still an undervalued earnings story, or has the market already priced in future growth?

Most Popular Narrative: 59.1% Overvalued

Compared with Bread Financial’s last close at $79.53, the most followed narrative pegs fair value closer to $50, which sets a very different reference point for today’s price.

Bread Financial Holdings Inc. (NYSE BFH) is a highly profitable bank focused on growing its portfolio of receivables, partners and customers. Although the company still distributes little of its earnings in the form of buybacks and dividends, the retained capital is reinvested at attractive rates, which compensate for the low payout. In a pessimistic scenario, the minority interest is protected by US$48.89 per share of tangible common equity, which is probably undervalued due to the volume of provisions made over the last two years. Bread Financial is a more complex thesis compared to the other banks in my portfolio, as it deals with regulatory uncertainties that challenge its business model. However, the shareholder who tolerated the high volatility has been rewarded. After all, the asset rose 52% from January to the end of July 2024, surpassing my price ceiling of US$50.00 per share. From now on, the two main points of attention are losses and how the company will adapt to the new late fee regulation. Even so, recent results have been quite positive.

Curious how a fair value well below today’s price still leans on strong profitability, reinvested earnings and a specific future profit multiple? According to Rodrigo_Toledo, the real story sits in a tight set of assumptions about margins, receivables growth and where the earnings multiple could settle over time, and those details are where this valuation really takes shape.

Result: Fair Value of $50 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on credit losses staying contained and on Bread Financial adjusting profitably to late fee rules that could pressure earnings and returns on retained capital.

Find out about the key risks to this Bread Financial Holdings narrative.

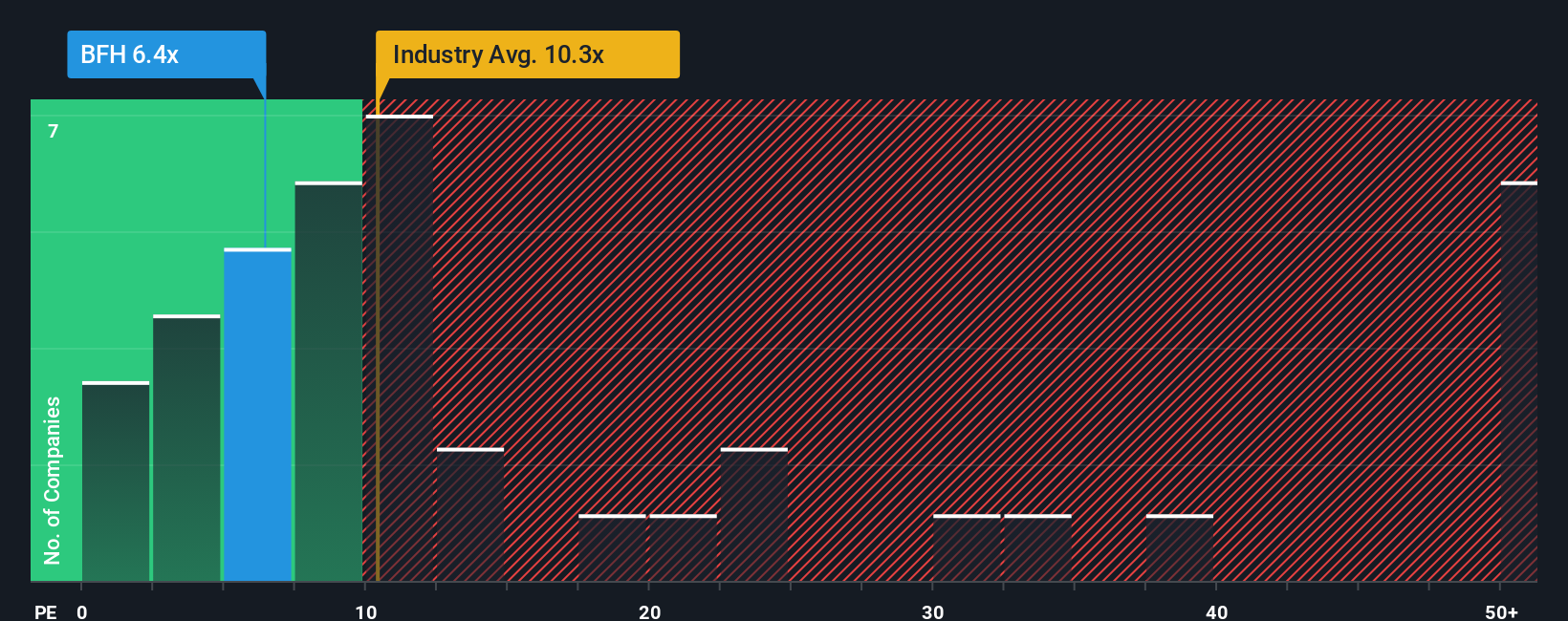

Another View: Market Pricing Through the P/E Lens

That $50 fair value from the user narrative contrasts sharply with what current earnings suggest. At a P/E of 6.7x, Bread Financial trades at a heavy discount to both its peer average of 38.2x and the US Consumer Finance industry on 8.2x, while our fair ratio sits at 13.5x. For investors, that gap raises a simple question: is the market overestimating risk or underestimating the earnings power that recent results point to?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Bread Financial Holdings Narrative

If you see the numbers differently or simply prefer to test your own assumptions, you can build a personalized view in just a few minutes: Do it your way

A great starting point for your Bread Financial Holdings research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Bread Financial has sharpened your focus, do not stop here. Broaden your watchlist with ideas that match the way you like to invest.

- Target value first and check our list of 53 high quality undervalued stocks that pass strict quality and fundamentals filters.

- Prioritize resilience by reviewing a 86 resilient stocks with low risk scores that may appeal if capital protection sits high on your list.

- Get ahead of the crowd by scanning a screener containing 24 high quality undiscovered gems that most investors are not paying attention to yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com