- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Lionsgate Studios (LION) Q3 Loss Narrows To US$46.2 Million Challenging Bearish Narratives

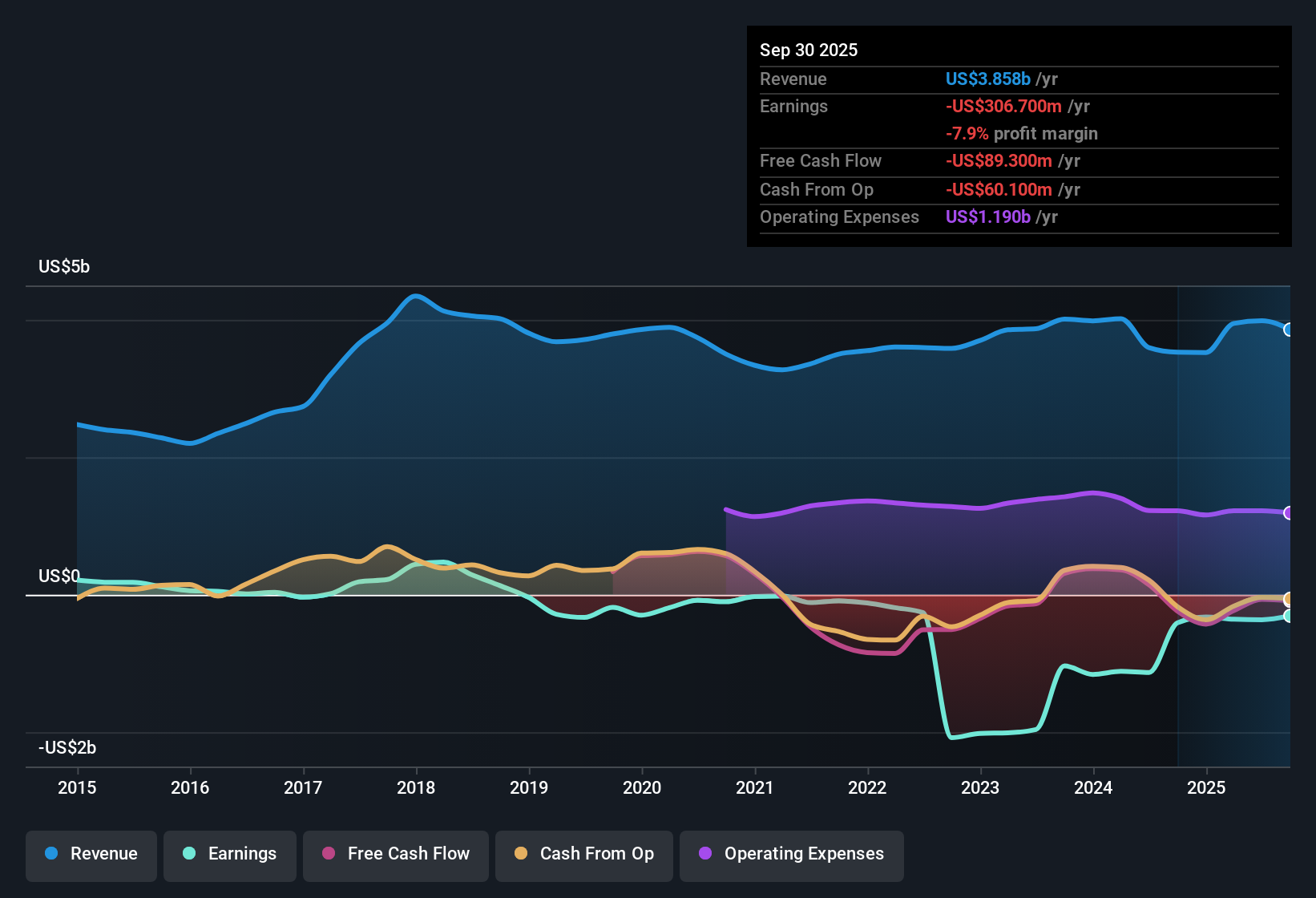

Lionsgate Studios (LION) just posted Q3 2026 results with revenue of US$724.3 million and a basic EPS loss of US$0.16, alongside net income excluding extra items of a US$46.2 million loss that keeps profitability under pressure. The company has seen quarterly revenue move from US$970.5 million in Q3 2025 to US$724.3 million in Q3 2026, while basic EPS shifted from a loss of US$0.08 to a loss of US$0.16, so investors will be weighing how much of that shortfall is tied to margins rather than top line. With current forecasts indicating stronger earnings in analyst models, this set of numbers puts the focus squarely on how quickly Lionsgate can tighten costs and rebuild film and TV margins.

See our full analysis for Lionsgate Studios.With the headline figures in place, the next step is to see how these results line up against the widely followed bullish and bearish narratives around Lionsgate’s future earnings power and margin recovery.

Curious how numbers become stories that shape markets? Explore Community Narratives

Losses Narrow Versus Recent Quarters

- Net income excluding extra items came in at a loss of US$46.2 million in Q3 2026, compared with losses of US$112.2 million in Q2 2026 and US$94 million in Q1 2026, while trailing 12 month losses stand at US$330 million.

- What stands out for the bullish view that earnings can improve is that the quarterly loss this time is smaller than the earlier 2026 quarters, even though the longer term picture still shows US$330 million of losses over the last 12 months.

- Supporters of the bullish case may point to the Q3 2026 loss being less than half of Q2 2026 as a sign that cost control or project timing is helping narrow the gap, at least for now.

- At the same time, the fact that trailing 12 month losses remain large at US$330 million keeps pressure on the idea that a return to profitability within three years depends on more than just a single softer loss.

Valuation Signals Versus Ongoing Losses

- Lionsgate trades on a P/S of 0.7x compared with 2.6x for peers and 1.3x for the US Entertainment industry, while the DCF fair value of US$13.05 sits above the current share price of US$9.04.

- Supporters of a bullish thesis see the low 0.7x P/S multiple and the gap between the US$9.04 share price and the US$13.05 DCF fair value as a potential upside setup, but the trailing 12 month loss of US$330 million shows that this hinges on a meaningful turn in profitability.

- Bullish investors may argue that the 30.7% discount to DCF fair value reflects an earnings path that includes the forecast 80.29% yearly improvement and an eventual move into profit, rather than the recent run of losses.

- What complicates that bullish angle is that revenue over the last 12 months is US$3.6b while losses still total US$330 million, so a low sales multiple is being placed on a business that has yet to convert that scale into positive earnings.

Bulls argue that Q3’s smaller loss, low P/S multiple, and discount to DCF fair value could mark an early turning point for Lionsgate’s story even while reported earnings remain negative. 🐂 Lionsgate Studios Bull Case

Balance Sheet Risks Stay Front And Center

- Trailing 12 month analysis flags less than one year of cash runway and negative shareholders’ equity alongside US$330 million of losses, with recent commentary also pointing to significant insider selling over the past three months.

- Skeptical investors focus on this bearish angle, since limited cash runway and negative equity, combined with continued losses over the last year, leave less room for error even if forecasts call for 80.29% yearly earnings improvement and a shift to profitability within three years.

- Critics highlight that an unprofitable business with negative equity may need to rely on external funding or stronger operating cash flow, which is harder to reconcile with forecasts that also assume revenue will decline around 1.4% per year.

- What reinforces the cautious stance is that the trailing 12 month loss of US$330 million sits alongside recent insider selling, which some investors view as a signal to treat those optimistic earnings forecasts with extra care.

Skeptics warn that the combination of negative equity, limited cash runway, and insider selling keeps financial risk high despite any projected earnings rebound. 🐻 Lionsgate Studios Bear Case

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Lionsgate Studios's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Lionsgate is still working through US$330 million of trailing 12 month losses, negative shareholders’ equity, limited cash runway and insider selling, which keeps risk elevated.

If that level of financial strain feels uncomfortable, shift your attention to companies in our solid balance sheet and fundamentals stocks screener (45 results) that pair sturdier balance sheets with fundamentals designed to better withstand setbacks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com