- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

WesBanco (WSBC) Valuation Check After Earnings Miss And Acquisition Integration Update

Why WesBanco’s latest earnings moved the stock

WesBanco (WSBC) shares reacted after fourth quarter results met revenue expectations but modestly missed non GAAP earnings, as management discussed acquisition integration, deposit trends, expense actions, and growth plans in newer markets.

See our latest analysis for WesBanco.

The share price reaction around earnings sits within a stronger recent trend, with a 7 day share price return of 6.02% and a 90 day share price return of 20.87%, while the 5 year total shareholder return of 52.27% points to momentum that has built over time.

If this earnings update has you reassessing your watchlist, it could be a good moment to look at 22 top founder-led companies as potential fresh ideas beyond regional banks.

With WesBanco now trading at $37.35 and sitting about 6.6% below its average analyst price target, and at a reported intrinsic discount of roughly 47%, you have to ask: is there still a buying opportunity here, or has the market already priced in future growth?

Most Popular Narrative: 3.2% Undervalued

Compared with WesBanco’s last close at $37.35, the most followed narrative points to a fair value of $38.57, built on detailed views of growth, margins, and risk.

Recent expansion into high-growth markets (such as Northern Virginia and Knoxville) and successful integration of Premier Financial has increased WesBanco's access to regions with positive economic and demographic trends, supporting sustained organic loan and deposit growth, which is expected to drive higher future revenues.

Accelerated investment in digital banking capabilities and treasury management products is boosting fee-based income streams, as evidenced by current 40% year-over-year growth in non-interest income. This positions the company to capitalize on customer migration toward digital financial services, likely enhancing both revenue mix and net margins.

Curious what kind of revenue path and margin profile could support that fair value, especially with a higher future earnings multiple and a lower discount rate baked in, the full narrative lays out the specific growth, profitability, and valuation assumptions that sit behind this $38.57 figure.

Result: Fair Value of $38.57 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that fair value view depends on WesBanco avoiding softer commercial real estate conditions and managing rising expenses from branch changes and digital projects without squeezing margins.

Find out about the key risks to this WesBanco narrative.

Another Angle On WesBanco’s Value

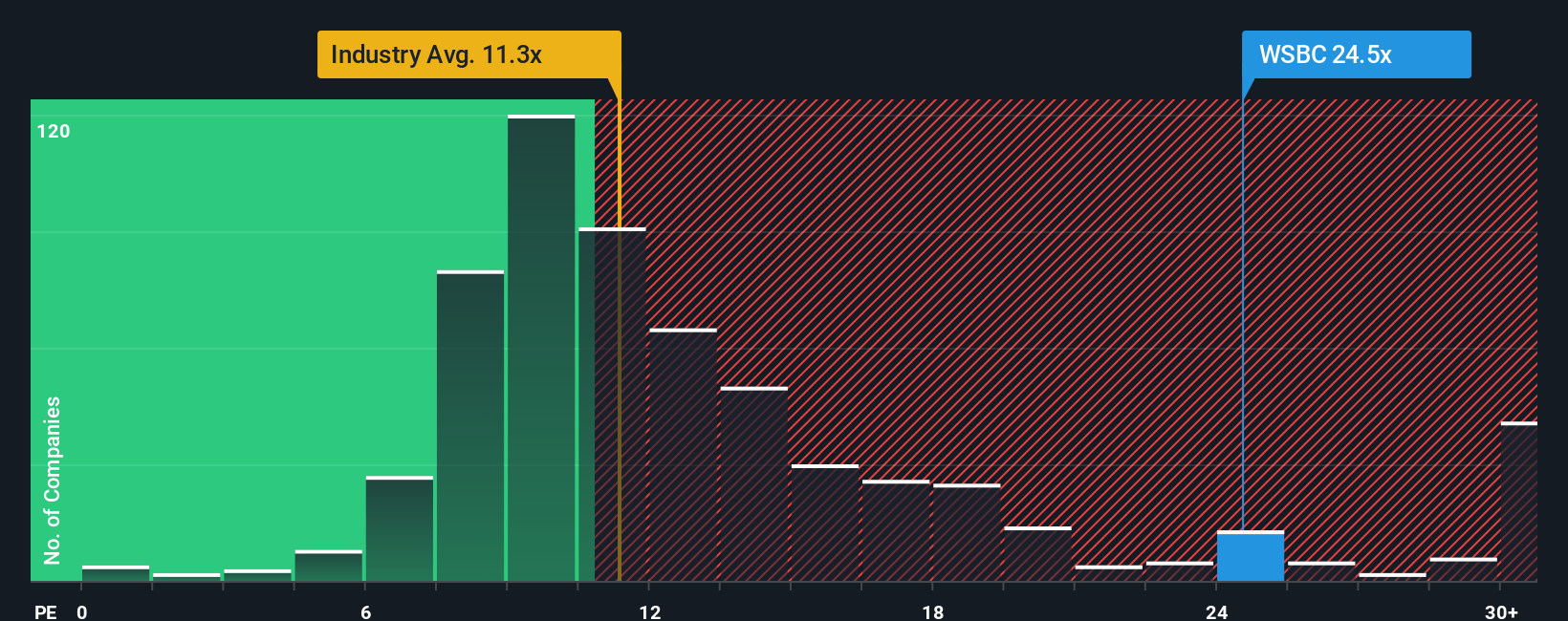

While our fair value estimate flags WesBanco as undervalued at around a 46.7% discount to a future cash flow value of $70.03, the current P/E of 17.7x sits only slightly above both the Banks industry at 12x and an estimated fair ratio of 17x. That mix of apparent upside and a full earnings multiple raises a simple question: is the gap a genuine mispricing or just a sign that expectations are already quite demanding?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own WesBanco Narrative

If you see the numbers differently or prefer to lean on your own research, you can build a fresh WesBanco story in just a few minutes, starting with Do it your way.

A great starting point for your WesBanco research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If WesBanco is already on your radar, do not stop there. A broader watchlist can help you spot opportunities you might otherwise miss.

- Kick start your hunt for value by scanning our list of 55 high quality undervalued stocks that combine quality fundamentals with what may be attractive pricing.

- Zero in on resilience by checking out our 81 resilient stocks with low risk scores that score well on stability and risk metrics.

- Unearth potential future favorites with our screener containing 25 high quality undiscovered gems that many investors may not be watching yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com