- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing NVR (NVR) Valuation After Weaker 2025 Earnings And Premium P/E Multiple

NVR (NVR) has drawn investor attention after reporting lower net income and earnings per share for both the fourth quarter and full year 2025, prompting a closer look at what the latest results imply.

See our latest analysis for NVR.

The weaker 2025 earnings numbers come after a period where momentum in NVR’s share price has been firming, with a 30 day share price return of 11.12% and a 3 year total shareholder return of 59.29% signaling that long term holders have still done materially better than short term traders.

If NVR’s move has you thinking about where else capital is flowing in the market, this could be a good moment to scan 22 top founder-led companies as potential next ideas on your list.

With earnings under pressure but the share price still climbing, the real question for you is whether NVR’s current valuation leaves any margin of safety or if the market is already pricing in future growth.

Preferred P/E of 16.8x: Is it justified?

NVR currently trades on a P/E of 16.8x, which is higher than both the US Consumer Durables industry average of 12.7x and the peer average of 15.1x. This means the market is paying a premium for each dollar of earnings at the last close of $8,044.79.

The P/E ratio compares the share price to earnings per share. It is a quick way to see how much investors are willing to pay for the company’s current earnings. For a homebuilder like NVR, that matters because earnings can be sensitive to housing demand and financing conditions, so the multiple often reflects how confident the market is in the durability of profits.

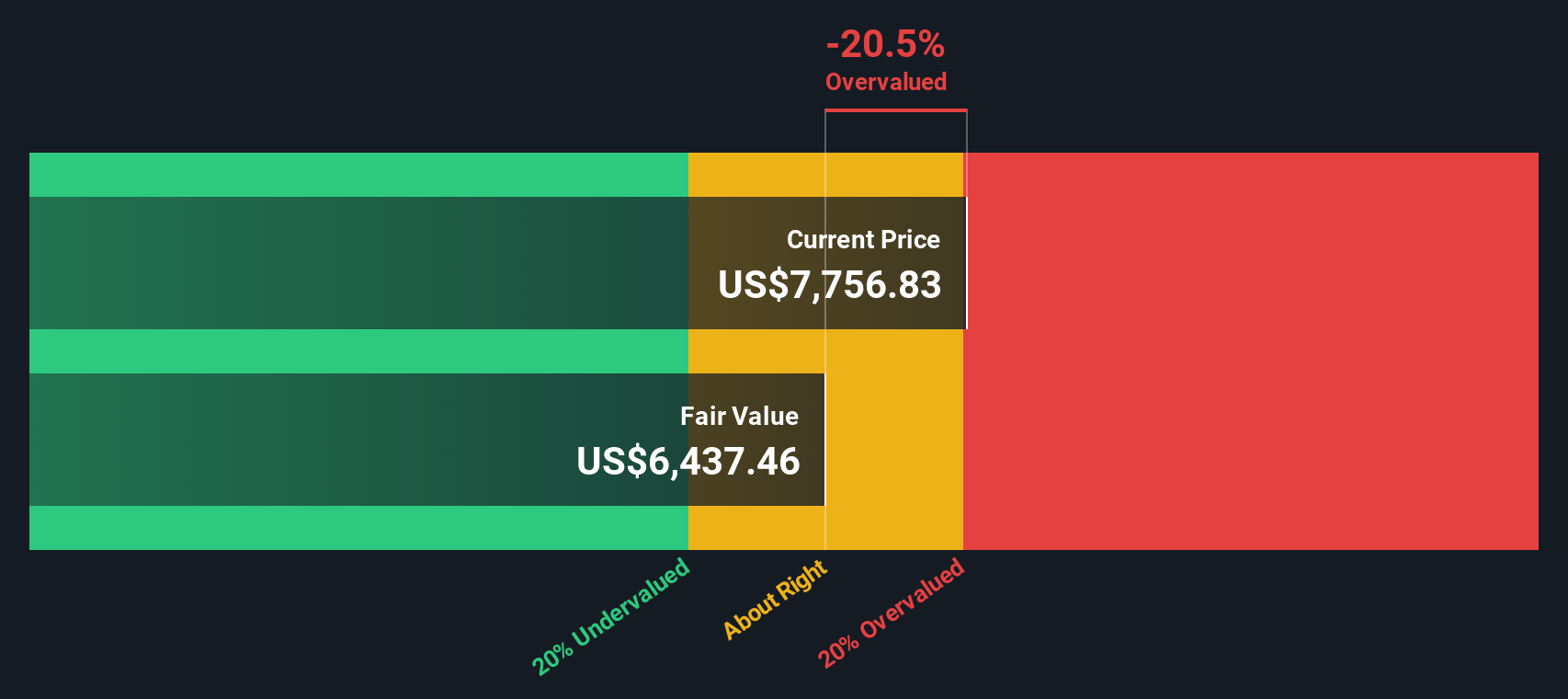

Here, the premium P/E sits against several mixed signals. NVR’s earnings have grown by 6.5% per year over the past 5 years, yet earnings over the past year declined by 20.3%. In addition, revenue and earnings are both forecast to decline on average over the next 3 years. At the same time, the company’s Return on Equity is high at 34.7% and forecast to remain high, and NVR is trading at a 13% discount to the SWS DCF model estimate of future cash flow value of $9,249.10. This is one level the market could potentially move toward if those cash flow expectations hold.

Compared with the US Consumer Durables industry average P/E of 12.7x and the peer average of 15.1x, NVR’s 16.8x multiple suggests the market is assigning a clearly higher valuation than many close comparables. That stands above the estimated fair P/E of 15.8x as well, indicating the current price already assumes stronger earnings quality or resilience than the regression based fair ratio implies.

Explore the SWS fair ratio for NVR

Result: Price-to-Earnings of 16.8x (OVERVALUED)

However, you also have to weigh risks such as annual revenue and net income declines, as well as the possibility that weaker housing demand could challenge a premium P/E like this.

Find out about the key risks to this NVR narrative.

Another way to look at value

While the P/E points to an expensive stock, our DCF model tells a different story. At $8,044.79, NVR trades about 13% below the SWS DCF model estimate of $9,249.10. This frames the current price as a discount to projected cash flows rather than a premium. Which story do you trust more, earnings today or cash flows tomorrow?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out NVR for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own NVR Narrative

If this take on NVR does not quite fit how you see the company, you can stress test every assumption yourself and shape a view that matches your own process, then Do it your way in under three minutes.

A great starting point for your NVR research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If NVR is just one piece of your watchlist, do not stop here. Widen your research now or you will miss opportunities others are already studying.

- Target steadier potential by reviewing companies with 81 resilient stocks with low risk scores that may help you build a more resilient core in your portfolio.

- Hunt for potential bargains by scanning 55 high quality undervalued stocks that pair stronger fundamentals with prices that have not fully reflected them yet.

- Add fresh names to your radar with our screener containing 25 high quality undiscovered gems, where lesser known companies can offer different return profiles to the usual large caps.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com