- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Houlihan Lokey (HLI) Valuation After Earnings Beat And Growth Expansion Signals

Houlihan Lokey (HLI) is back in focus after quarterly results topped Wall Street forecasts, supported by active Corporate Finance work, heavier private equity deal flow, and fresh commentary around data monetization and European expansion.

See our latest analysis for Houlihan Lokey.

Recent news around earnings, European hiring and the completed share repurchase comes against a weaker price backdrop, with a 30 day share price return of 9.24% and a 1 year total shareholder return of 9.2%. The 3 year total shareholder return of 86.76% and 5 year total shareholder return of 175.67% point to much stronger longer term momentum.

If this M&A and advisory story has your attention, it can be worth broadening your watchlist with our 22 top founder-led companies, a curated way to spot potential long term compounders.

With HLI shares down over the past year despite earnings coming in ahead of expectations, a completed US$221.73 million buyback and European hiring, you have to ask: is there still value here, or is the market already pricing in future growth?

Most Popular Narrative: 20% Undervalued

With Houlihan Lokey last closing at $167.94 versus a narrative fair value of about $210.86, the gap is all about what future earnings power looks like when you factor in deal flow, margins and capital returns.

Analysts are assuming Houlihan Lokey's revenue will grow by 12.5% annually over the next 3 years.

Analysts assume that profit margins will increase from 16.5% today to 18.5% in 3 years time.

Curious what kind of M&A and restructuring mix could support that earnings path and still justify a premium future multiple on those profits, and how disciplined cost control and capital returns fit into the fair value math, without relying on aggressive assumptions or blue sky scenarios.

Result: Fair Value of $210.86 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear pressure points, including reliance on U.S. deal activity and a high cost base that could squeeze margins if revenue growth disappoints.

Find out about the key risks to this Houlihan Lokey narrative.

Another Angle On Valuation

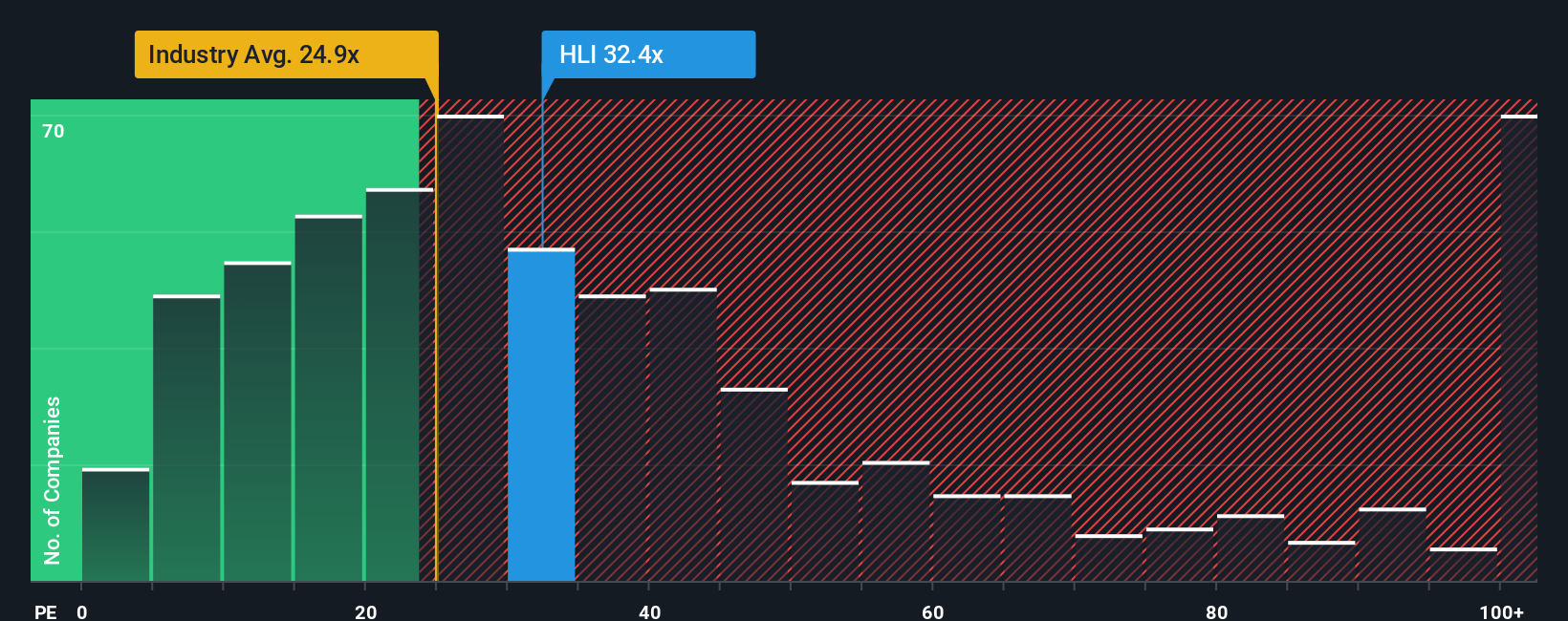

The first view suggests Houlihan Lokey is about 20% undervalued. However, its current P/E of 26.2x is higher than both the US Capital Markets industry at 22.8x and the peer average at 17.9x, and it is also above a fair ratio of 16.3x. This indicates clear re rating risk if sentiment cools.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Houlihan Lokey Narrative

If you see the numbers differently or want to stress test your own assumptions, you can build a personalized valuation story for Houlihan Lokey in just a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 5 key rewards investors are optimistic about regarding Houlihan Lokey.

Looking for more investment ideas?

If Houlihan Lokey has sharpened your thinking, do not stop here. Use the Simply Wall Street Screener to line up your next set of focused ideas.

- Target quality at a discount by scanning our 55 high quality undervalued stocks, which combines strong fundamentals with prices that look appealing on key metrics.

- Prioritise resilience by checking out the 81 resilient stocks with low risk scores, built around companies with lower risk scores and more defensible profiles.

- Spot under the radar opportunities through the screener containing 25 high quality undiscovered gems, which highlights strong businesses the broader market may be overlooking.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com