- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Surf Air Mobility (SRFM) Valuation After New Hawaii eVTOL Integration Partnership News

Surf Air Mobility (SRFM) has drawn fresh attention after announcing a collaboration with Hawaii’s Department of Transportation and BETA Technologies on an eVTOL Integration Pilot Program under the White House’s Advanced Air Mobility National Strategy.

See our latest analysis for Surf Air Mobility.

Despite the eVTOL partnership headline, Surf Air Mobility’s recent trading has been weak, with a 30 day share price return of a 36.81% decline and a 1 year total shareholder return of a 53.92% decline from a latest share price of $1.94, which hints that investor risk perceptions remain cautious even as interest in advanced air mobility grows.

If this news has you thinking more broadly about the future of air and transport technology, it could be a good moment to scan 33 AI infrastructure stocks as potential next ideas to research.

With Surf Air Mobility’s shares under pressure despite the eVTOL headlines and a price target of US$7.75 sitting well above the latest US$1.94 close, you have to ask: is this a mispriced opportunity, or is the market already discounting future growth?

Most Popular Narrative: 75.4% Undervalued

Surf Air Mobility’s most followed narrative pegs fair value at $7.88, versus the latest $1.94 close, so the story behind that gap really matters.

The accelerating demand for regional, point to point air mobility as urban congestion worsens is expected to increase the addressable market for Surf Air Mobility, especially as it expands scheduled service on new routes and accepts new aircraft deliveries in 2026, supporting future revenue growth. Widespread digitization and adoption of app driven travel is enabling Surf Air Mobility's software first approach including the commercial rollout of the SurfOS platform in 2026 bringing new high margin recurring revenue streams and improved customer acquisition efficiency, supporting both revenue and net margin expansion.

Curious what justifies that kind of upside gap? The core narrative leans on rapid revenue expansion, margin uplift from software, and a future earnings multiple more often linked to higher growth sectors.

Result: Fair Value of $7.88 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside case leans heavily on timely SurfOS monetization and steady government contract support. Both of these factors could easily move against the story.

Find out about the key risks to this Surf Air Mobility narrative.

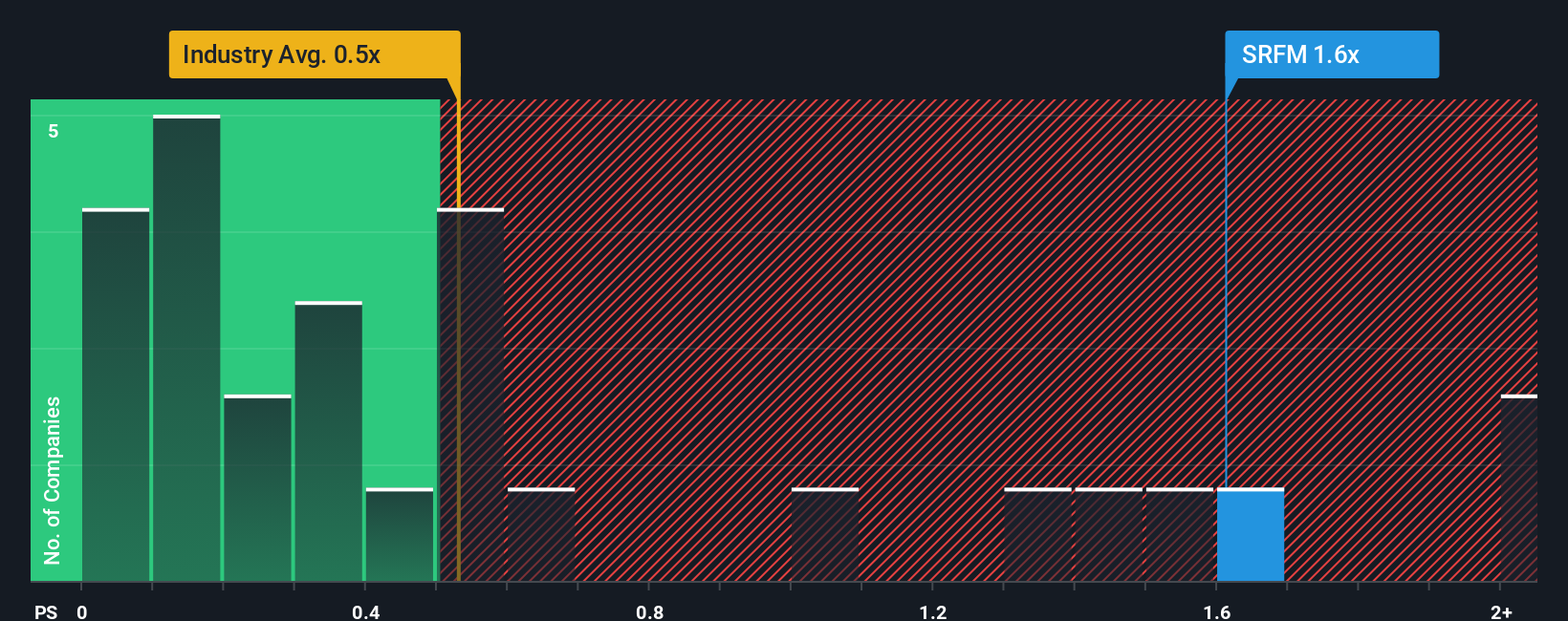

Another View: What The Sales Multiple Is Saying

That $7.88 fair value hinges on upbeat growth and margin assumptions, but the current P/S of 1.1x paints a tougher picture. It sits above the North American Airlines average of 0.6x and the fair ratio of 0.3x, which suggests meaningful downside risk if sentiment cools.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Surf Air Mobility Narrative

If you look at the numbers and reach a different conclusion, or just prefer to test your own assumptions, you can build a Surf Air Mobility story from scratch in a few minutes, your way with Do it your way

A great starting point for your Surf Air Mobility research is our analysis highlighting 1 key reward and 4 important warning signs that could impact your investment decision.

Ready to widen your opportunity set?

If Surf Air Mobility has sharpened your thinking, do not stop here, you could be skipping ideas that fit your goals even better.

- Target potential value candidates by scanning 55 high quality undervalued stocks that pair quality fundamentals with what our model views as discounted prices.

- Focus on resilience first by reviewing 81 resilient stocks with low risk scores where companies show lower risk scores based on our broader fundamentals checks.

- Hunt for earlier stage potential by checking 25 elite penny stocks with strong financials that pass our basic financial quality filters instead of relying on hype alone.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com