- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Magnera (MAGN) Narrowing Losses In Q1 2026 Challenges Bearish Profitability Narratives

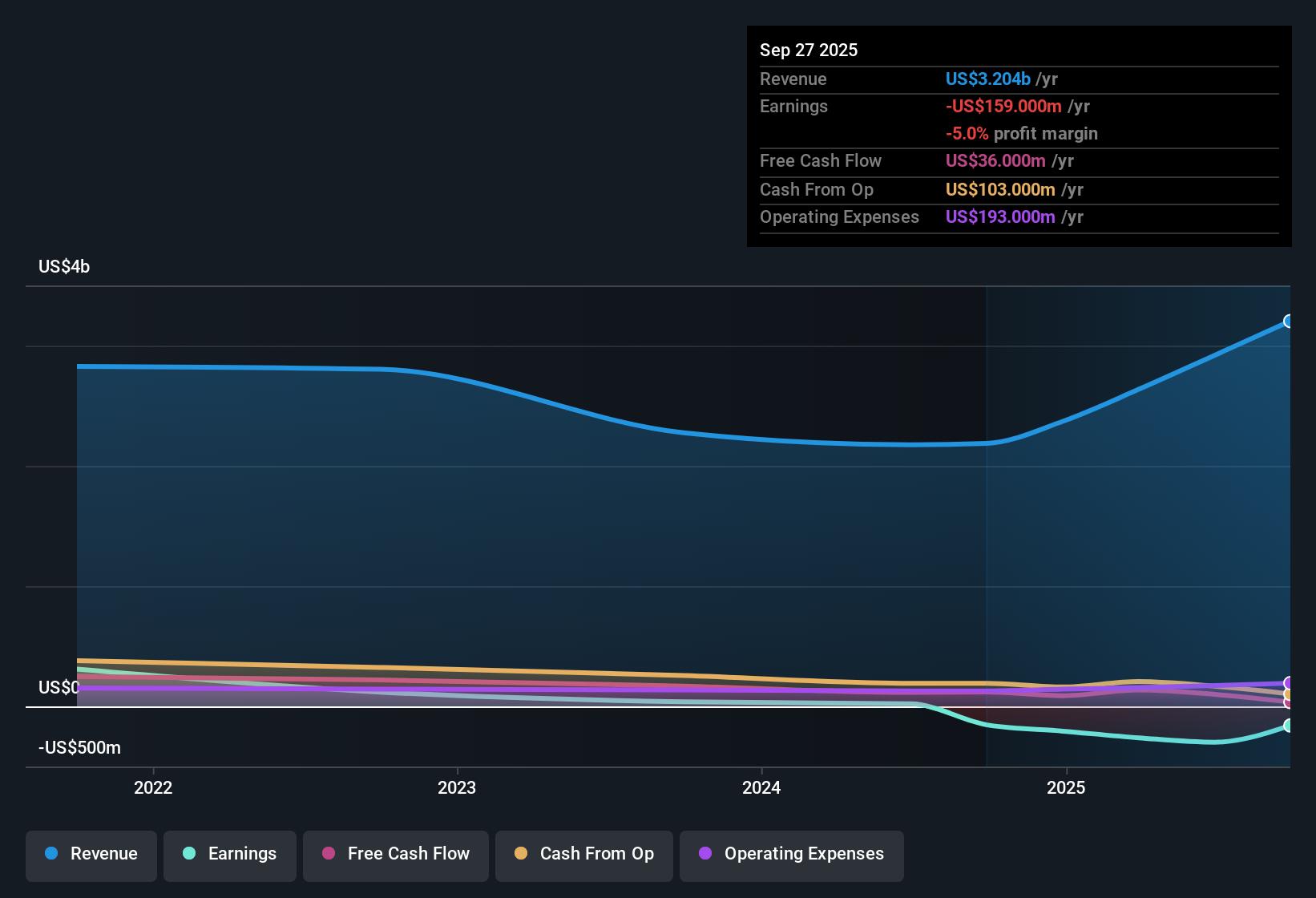

Magnera (MAGN) just opened Q1 2026 with revenue of US$792 million and a basic EPS loss of US$0.96 per share, setting the tone for another quarter where top line and per share losses stay front and center for investors. Over the past year, the company has seen quarterly revenue move from US$702 million in Q1 2025 to US$792 million in Q1 2026, while basic EPS has ranged from a loss of US$1.69 in Q1 2025 to a loss of US$0.96 most recently, leaving margins under pressure and keeping the path to improved profitability firmly in focus.

See our full analysis for Magnera.With the latest numbers on the table, the next step is to weigh these results against the stories investors follow about Magnera and see where the data backs those narratives and where it pushes back.

Curious how numbers become stories that shape markets? Explore Community Narratives

Losses Narrow to US$34 Million on Q1 Basis

- Magnera reported Q1 2026 net income excluding extra items of a US$34 million loss on US$792 million of revenue, compared with quarterly losses in the last year that ranged from US$18 million to US$60 million on revenues of US$702 million to US$839 million.

- What stands out for the bullish view that sees a path to profitability within three years is that trailing twelve month losses of US$133 million now sit against US$3.3b of revenue, and

- Trailing losses over the last year were US$159 million to US$206 million at revenues between US$2.4b and US$3.2b, which investors can compare directly to the latest US$133 million trailing loss on US$3.3b.

- This trend heavily supports the bullish argument that earnings can improve from here, even though the company is still unprofitable today.

TTM Revenue At US$3.3b With 2.6% Growth

- On a trailing twelve month basis to Q1 2026, Magnera recorded about US$3.3b in revenue and a US$133 million loss, with the analysis data pointing to 2.6% annual revenue growth over the last year.

- Skeptics focus on the bearish point that losses have grown at a 74.3% compound rate over five years and argue that modest 2.6% trailing revenue growth does not yet offset that pressure, and

- The five year loss growth rate of 74.3% a year sits against only 2.6% annual revenue growth on the trailing twelve months, which is also below the 10.3% growth rate flagged for the broader US market.

- This combination supports the bearish concern that slow top line growth has so far not been enough to materially change the company’s overall loss profile.

P/S of 0.2x and DCF Fair Value Gap

- Magnera trades on a P/S of 0.2x, compared with 0.5x for peers and 0.7x for the wider industry, and the DCF fair value of US$19.27 sits about 22.4% above the current share price of US$14.96.

- What is interesting for the bullish narrative that highlights valuation appeal is that this low P/S and the DCF fair value gap sit beside ongoing losses, and

- Trailing losses of US$133 million across US$3.3b in revenue show the business is still in loss making territory even while the market assigns a lower P/S multiple than peers.

- This tension between a discounted 0.2x P/S multiple and continued unprofitability is exactly what bulls and bears are debating when they look at the 22.4% gap to the DCF fair value.

Analysts watching this valuation and loss profile closely are asking whether the low P/S is a genuine mispricing or simply compensation for risk, and the full narrative around that trade off is set out in 📊 Read the full Magnera Consensus Narrative.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Magnera's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Magnera is still working through modest 2.6% revenue growth, continued losses, and a low P/S, which together keep risk firmly on the table for investors.

If that combination makes you want something steadier, check out 80 resilient stocks with low risk scores to quickly zero in on companies with profiles that aim to keep volatility and downside pressure in check.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com