- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Lucky Strike Entertainment (LUCK) Quarterly Loss Challenges Bulls On Path To Profitability Narrative

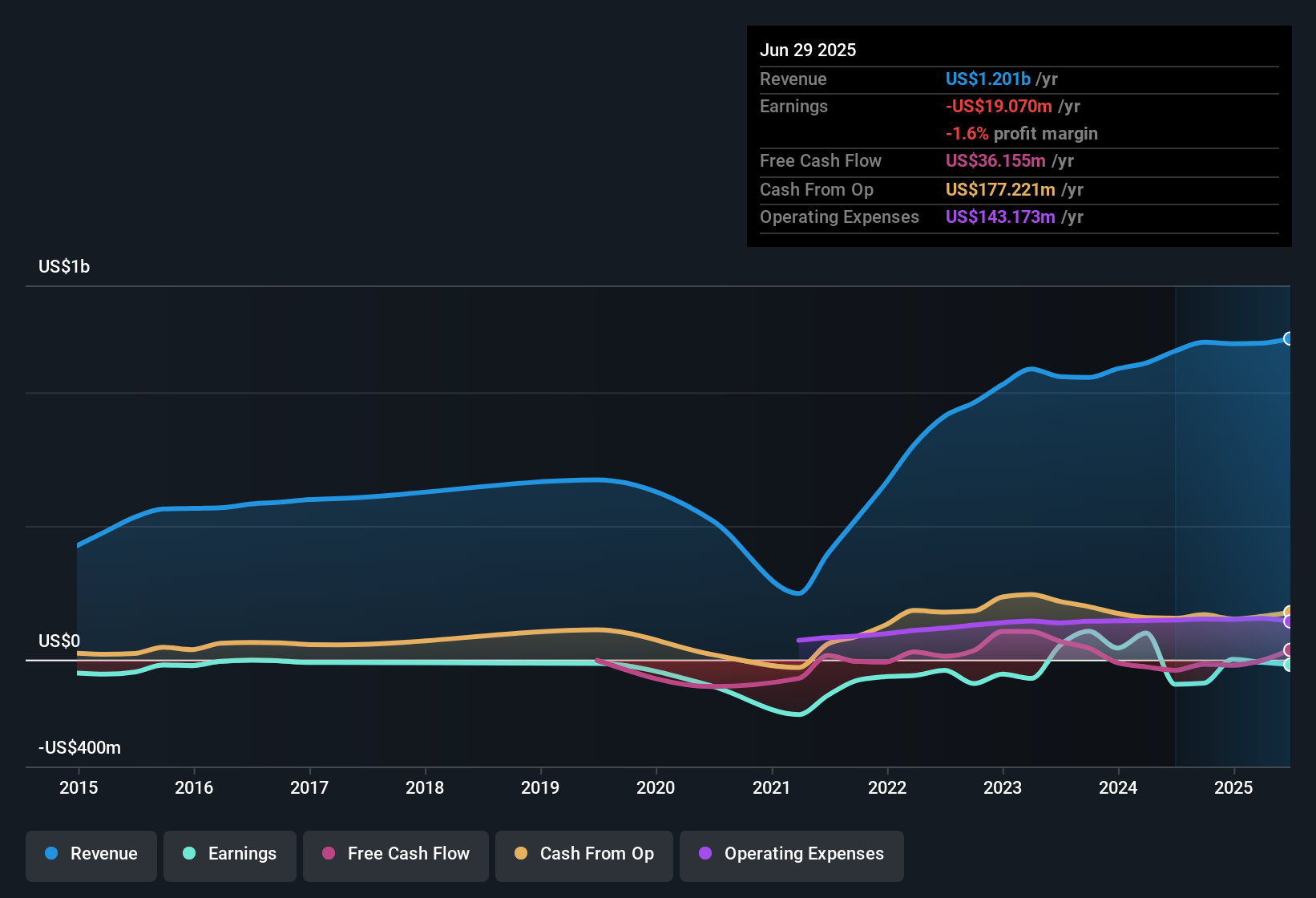

Lucky Strike Entertainment (LUCK) has just posted its Q2 2026 numbers, reporting revenue of US$306.9 million and a basic EPS loss of US$0.11, alongside a trailing twelve month basic EPS loss of US$0.68 on revenue of about US$1.2 billion. The company’s quarterly revenue has moved from US$260.2 million in Q1 2025 to US$300.1 million in Q2 2025 and US$306.9 million in Q2 2026. Over the same period, EPS has shifted from a profit of US$0.17 in Q2 2025 to a loss of US$0.11 in the latest quarter. This sets up an earnings season in which investors are likely to focus on how quickly margins can stabilise from here.

See our full analysis for Lucky Strike Entertainment.With the latest figures on the table, the next step is to assess how these results compare with the prevailing narratives around Lucky Strike’s growth prospects, risks, and potential earnings trajectory.

Curious how numbers become stories that shape markets? Explore Community Narratives

LTM loss of US$94.3 million keeps profitability in focus

- On a trailing twelve month basis, Lucky Strike recorded net income loss of US$94.3 million on US$1.24b of revenue, with basic EPS loss of US$0.68 over that same period.

- What stands out for the bullish view that talks about an improving earnings path is that trailing losses are still present even though recent quarterly net income loss narrowed from US$73.3 million in Q4 2025 to about US$15.1 million in both Q1 and Q2 2026.

- Supporters who point to five year loss reduction of about 26.6% a year can reference this shift in quarterly net income, but the full year picture over the last twelve months remains materially loss making at US$94.3 million.

- That creates a gap between the idea of a business moving toward healthier profitability and the reality that, across the last four reported quarters combined, the company is still firmly in loss territory.

Investors who want a balanced, numbers first take on where this earnings trend might lead next can read the broader market view on Lucky Strike, including how bulls and bears are weighing the current loss profile against future potential, in 📊 Read the full Lucky Strike Entertainment Consensus Narrative.

US$306.9 million Q2 revenue versus 4.7% growth outlook

- Q2 2026 revenue of US$306.9 million contributes to trailing twelve month revenue of about US$1.24b, while forecasts in the data show annual revenue growth of 4.7%, which is below the 10.3% forecast for the wider US market.

- Supportive arguments that Lucky Strike can build on its consumer entertainment brands meet a clear ceiling in these figures because the forecast 4.7% revenue growth rate sits well under the broader US market forecast of 10.3%.

- Backers who highlight the breadth of bowling, water park, karting and family entertainment venues have to reconcile that breadth with the modest revenue growth forecast embedded in the numbers.

- At the same time, Q2 revenue moving from US$260.2 million in Q1 2025 to US$306.9 million in Q2 2026 shows the top line has been holding around the US$300 million level per quarter, which may be enough for some investors to stay focused on execution rather than chasing market level growth.

0.7x P/S and US$6.34 price versus DCF fair value

- The shares trade on a P/S of 0.7x compared with 0.9x for peers and 1.6x for the US Hospitality industry, while the US$6.34 share price sits above the DCF fair value of about US$3.90 mentioned in the data.

- Critics who worry that the stock may not offer enough value point to the mix of negative shareholders’ equity, a dividend yield of 3.79% that is not well covered by earnings, and a share price above the DCF fair value even though the P/S ratio looks cheaper than peers.

- The relatively low 0.7x P/S versus 0.9x and 1.6x benchmarks suggests some valuation support on sales, yet ongoing losses over the trailing twelve months and negative equity mean the balance sheet and income statement do not fully line up with a simple cheap on multiples story.

- The fact that the US$6.34 share price is higher than the US$3.90 DCF fair value in the data adds another layer for cautious investors who prefer cash flow based yardsticks over revenue based multiples.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Lucky Strike Entertainment's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Lucky Strike is still working through a trailing twelve month loss of US$94.3 million, negative equity, and a dividend that current earnings do not cover.

If that mix of ongoing losses and a stretched balance sheet feels uncomfortable right now, check out solid balance sheet and fundamentals stocks screener (46 results) to quickly focus on companies that look financially sturdier.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com