- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Discovering US Market's Undiscovered Gems February 2026

As February 2026 unfolds, the U.S. stock market is experiencing a robust start with major indices like the Dow Jones and S&P 500 posting significant gains, reflecting optimism despite recent economic uncertainties such as delayed jobs data due to a government shutdown. In this dynamic environment, identifying promising small-cap stocks requires a keen eye for companies that not only demonstrate resilience in fluctuating economic conditions but also possess unique growth potential that can thrive amidst broader market trends.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 66.33% | 1.28% | -2.88% | ★★★★★★ |

| Morris State Bancshares | 1.99% | 2.14% | 1.63% | ★★★★★★ |

| Southern Michigan Bancorp | 113.59% | 8.48% | 3.73% | ★★★★★★ |

| Cashmere Valley Bank | 30.46% | 5.25% | 1.74% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 12.65% | 41.20% | ★★★★★★ |

| Sound Financial Bancorp | 16.27% | 0.75% | -13.26% | ★★★★★★ |

| Epsilon Energy | NA | 2.43% | -4.36% | ★★★★★★ |

| Seneca Foods | 41.64% | 2.31% | -23.77% | ★★★★★☆ |

| NameSilo Technologies | 12.63% | 14.48% | 3.12% | ★★★★★☆ |

| Pure Cycle | 5.42% | 9.36% | -2.03% | ★★★★★☆ |

Let's dive into some prime choices out of from the screener.

Capital City Bank Group (CCBG)

Simply Wall St Value Rating: ★★★★★★

Overview: Capital City Bank Group, Inc. serves as the financial holding company for Capital City Bank, offering a variety of banking services to both individual and corporate clients, with a market capitalization of approximately $731.23 million.

Operations: CCBG generates its revenue primarily from commercial banking, amounting to $248.74 million.

Capital City Bank Group, with assets totaling US$4.4 billion and equity of US$552.9 million, is trading at 41% below its estimated fair value. The bank's liabilities are 96% funded by low-risk customer deposits, which is less risky than external borrowing. Total deposits stand at US$3.7 billion against loans of US$2.5 billion, reflecting a solid funding structure. Earnings have grown impressively by 14% annually over the past five years but are expected to decrease slightly by 1% annually in the coming three years. The company also maintains a sufficient allowance for bad loans at just 0.3%.

Ategrity Specialty Insurance Company Holdings (ASIC)

Simply Wall St Value Rating: ★★★★★★

Overview: Ategrity Specialty Insurance Company Holdings, with a market cap of $841.17 million, operates through its subsidiaries to offer excess and surplus lines insurance and reinsurance products to small and medium-sized businesses in the United States.

Operations: ASIC generates revenue primarily from its insurance business, amounting to $405.66 million.

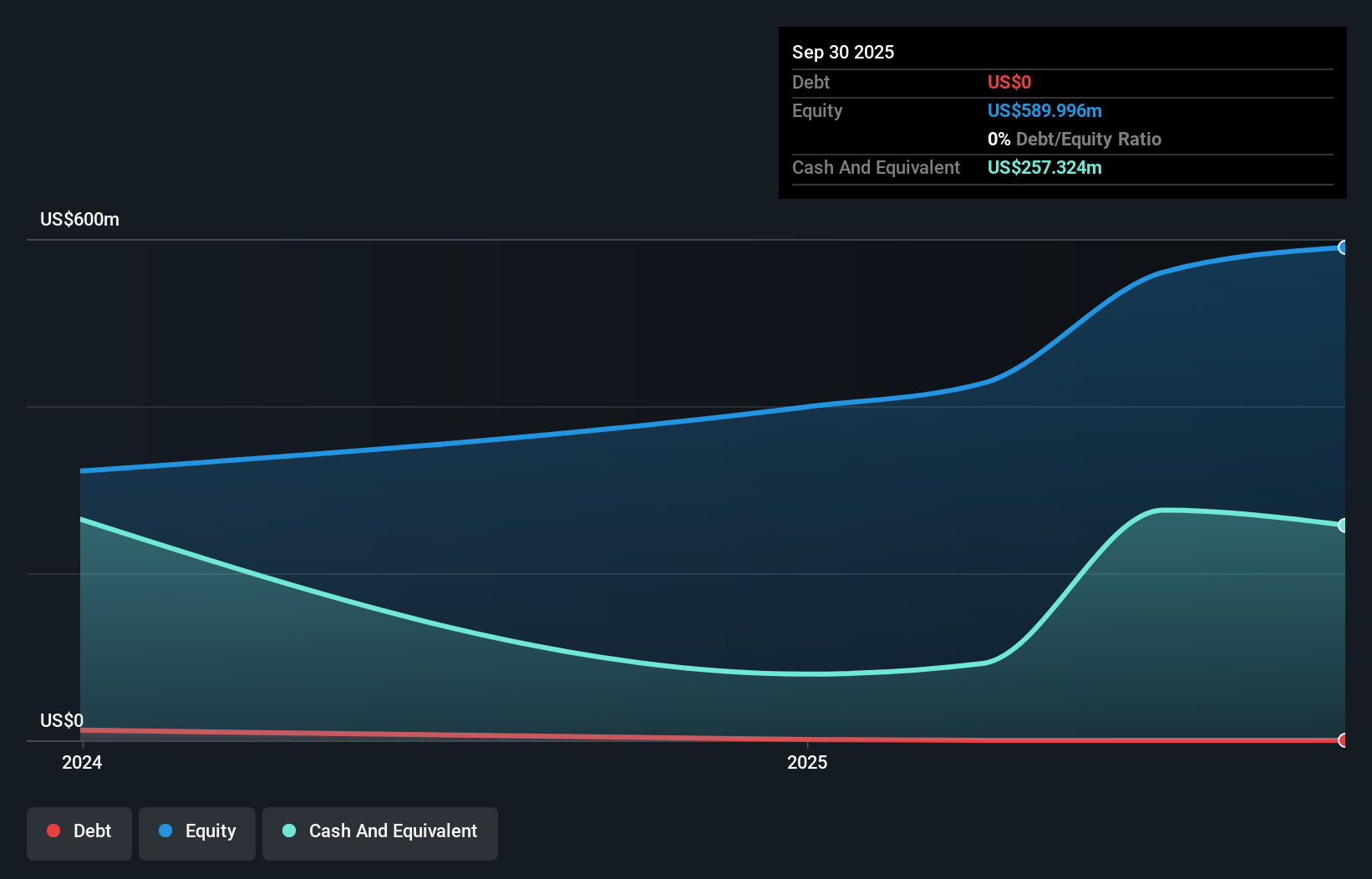

Ategrity Specialty Insurance Company Holdings, a nimble player in the insurance sector, recently joined the S&P Global BMI Index, signaling its growing market relevance. The company's innovative Ategrity Select platform targets over 200,000 religious institutions with pre-priced property and casualty coverage, enhancing underwriting efficiency. With earnings growth of 83.7% last year—well above the industry average of 10.3%—and trading at 54% below estimated fair value, Ategrity appears undervalued. Debt-free for five years and boasting high-quality earnings alongside positive free cash flow suggest strong financial health and potential for continued success in its niche market.

AdvanSix (ASIX)

Simply Wall St Value Rating: ★★★★★☆

Overview: AdvanSix Inc. is involved in the manufacture and sale of polymer resins both domestically and internationally, with a market capitalization of approximately $463.40 million.

Operations: AdvanSix generates revenue primarily from its chemical manufacturing segment, which contributed $1.49 billion. The company's financial performance is reflected in its net profit margin, indicating the efficiency of converting revenue into actual profit.

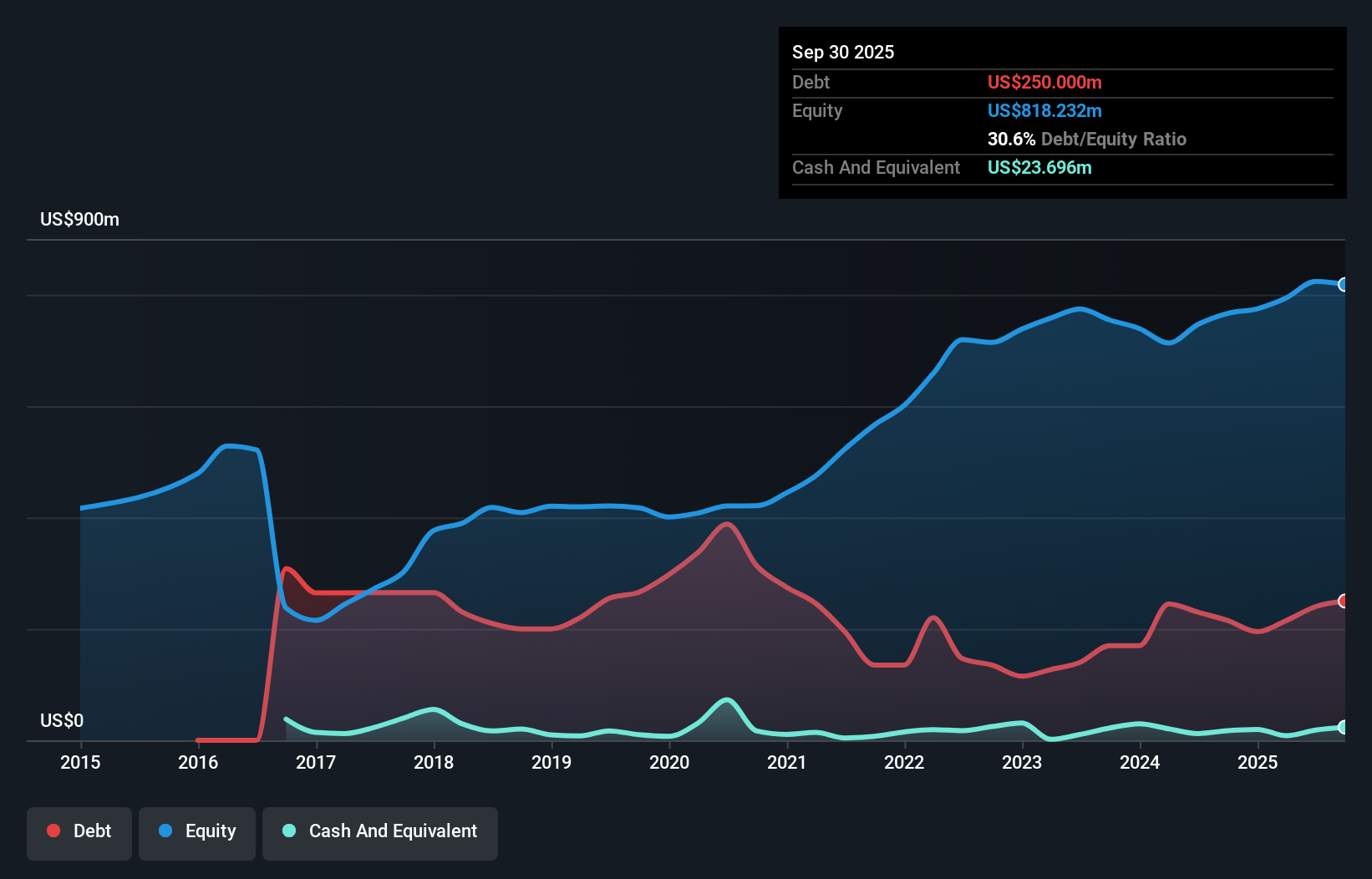

AdvanSix, a player in the chemicals sector, has been making strides with a 35% earnings growth over the past year, outpacing the industry's -0.3%. The company's net debt to equity ratio is satisfactory at 27.7%, and its interest payments are well covered by EBIT at 6.1 times coverage. Recently dropped from several S&P indices, AdvanSix still trades significantly below its estimated fair value by about 81%. Despite challenges such as rising costs and market pressures, expansions in ammonium sulfate production and carbon capture tax credits could bolster future earnings stability.

Where To Now?

- Unlock more gems! Our US Undiscovered Gems With Strong Fundamentals screener has unearthed 310 more companies for you to explore.Click here to unveil our expertly curated list of 313 US Undiscovered Gems With Strong Fundamentals.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com