- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Enova International (ENVA) Valuation After Strong 2025 Earnings Results

Enova International (ENVA) is back in focus after reporting fourth quarter and full year 2025 results. Management pointed to strong small business and consumer lending activity and targeted marketing that supported revenue and net income.

See our latest analysis for Enova International.

The earnings release and recent share repurchases have come after a strong run, with Enova International’s 90 day share price return of 26.75% and a 1 year total shareholder return of 35.72%, while shorter term share price returns have recently cooled.

If Enova’s move has you thinking about where else strong execution and ownership alignment might matter, it could be worth scanning fast growing stocks with high insider ownership for other ideas on your radar.

With the share price already up strongly over the past year and analysts’ average target sitting above the recent US$155.72 close, the key question now is whether Enova still offers upside or if the market is already pricing in future growth.

Most Popular Narrative: 19.6% Undervalued

At a last close of $155.72 against a fair value narrative of about $193.71, Enova International is framed as undervalued, with that gap tied directly to aggressive growth and profitability assumptions.

The scaling efficiencies of Enova's digital customer base, disciplined cost controls, and continued optimization of marketing effectiveness are driving operating leverage, leading to declining operating expenses as a percent of revenue and contributing to accelerating adjusted EPS growth and improving operating margins.

Curious what kind of revenue ramp and margin profile that sentence really implies? The narrative leans on rapid top line expansion, shifting profitability mix and a future earnings multiple that has to reconcile specialty finance risks with tech style growth assumptions. If you want to see exactly how those pieces fit together into that fair value, the full narrative lays it out in black and white.

Result: Fair Value of $193.71 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside view still runs into real pressure points, especially tighter consumer lending rules or a weaker nonprime credit cycle that could quickly reshape Enova’s growth and margin story.

Find out about the key risks to this Enova International narrative.

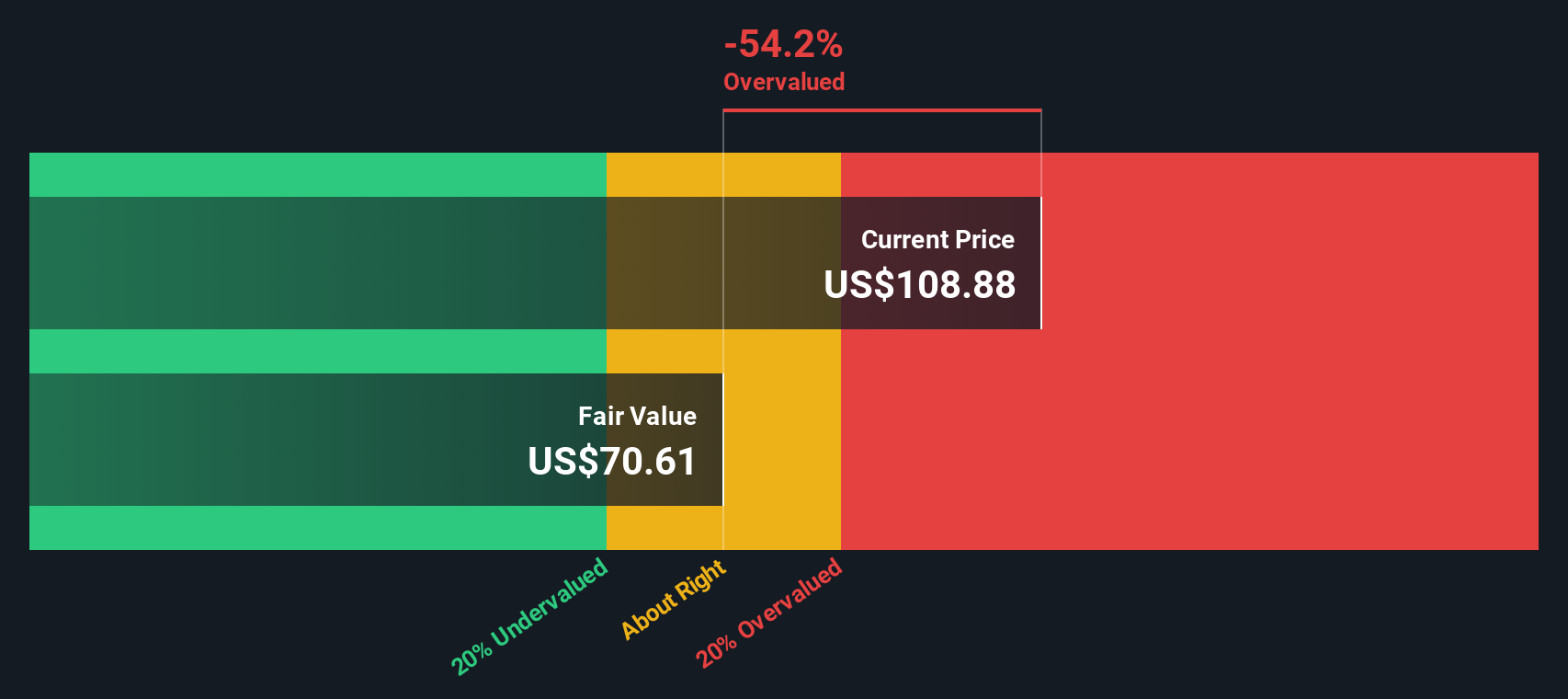

Another View: Cash Flows Tell a Tougher Story

There is a clear tension between the $193.71 fair value from the growth narrative and our DCF model, which points to a future cash flow value of about $82.01 per share. That implies Enova looks overvalued on a cash flow basis. Which signal do you trust more: earnings or cash generation?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Enova International for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 862 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Enova International Narrative

If the fair values and narratives here do not quite line up with your own view, you can always test the assumptions yourself and build a version that fits your research style, then Do it your way

A great starting point for your Enova International research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Enova sparks your interest but you do not want to stop at one name, now is the time to broaden your watchlist with focused, data driven stock ideas.

- Spot potential value opportunities by reviewing these 862 undervalued stocks based on cash flows that may offer stronger cash flow support for their current share prices.

- Position yourself for trends in digital assets by checking out these 19 cryptocurrency and blockchain stocks that are building businesses around blockchain and related technologies.

- Target income focused opportunities by scanning these 11 dividend stocks with yields > 3% that offer yields above 3% alongside listed financial metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com