- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Clean Harbors (CLH) Valuation Check After Recent Share Price Momentum

Clean Harbors (CLH) is back on investors’ radar after recent share performance, with the stock last closing at $260.95. This has prompted a closer look at how its current valuation lines up with fundamentals.

See our latest analysis for Clean Harbors.

Clean Harbors’ share price has been firming over the past few months, with a 30 day share price return of 6.89% and a 90 day share price return of 27.22%, while its 1 year total shareholder return of 10.46% and 5 year total shareholder return of 204.99% highlight how recent momentum fits into a much longer track record.

If environmental services is on your radar after looking at Clean Harbors, it could be a good moment to broaden your search with healthcare stocks as a contrast in defensive, service focused businesses.

With the shares now at $260.95, an intrinsic value estimate indicating a roughly 25% discount, and only a small gap to the latest analyst target, the key question is whether there is still a buying opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 10% Overvalued

Clean Harbors' most followed narrative pegs fair value at $260.69, which sits almost on top of the last close at $260.95, leaving little margin either way.

The growing urgency and evolving regulatory landscape around PFAS and hazardous waste management is expected to create a multibillion-dollar opportunity, and Clean Harbors' unique position as the only company with end-to-end PFAS destruction capabilities positions it to capture significant long-term revenue and margin growth as new government and corporate standards take effect.

There is a full playbook behind that PFAS angle, including revenue growth assumptions, margin shifts and a richer future earnings multiple. Curious what underpins that fair value call and how tight the discount rate assumptions really are?

Result: Fair Value of $260.69 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that playbook can fray if zero waste efforts curb hazardous volumes or if new remediation technologies undercut traditional incineration and landfill work sooner than analysts expect.

Find out about the key risks to this Clean Harbors narrative.

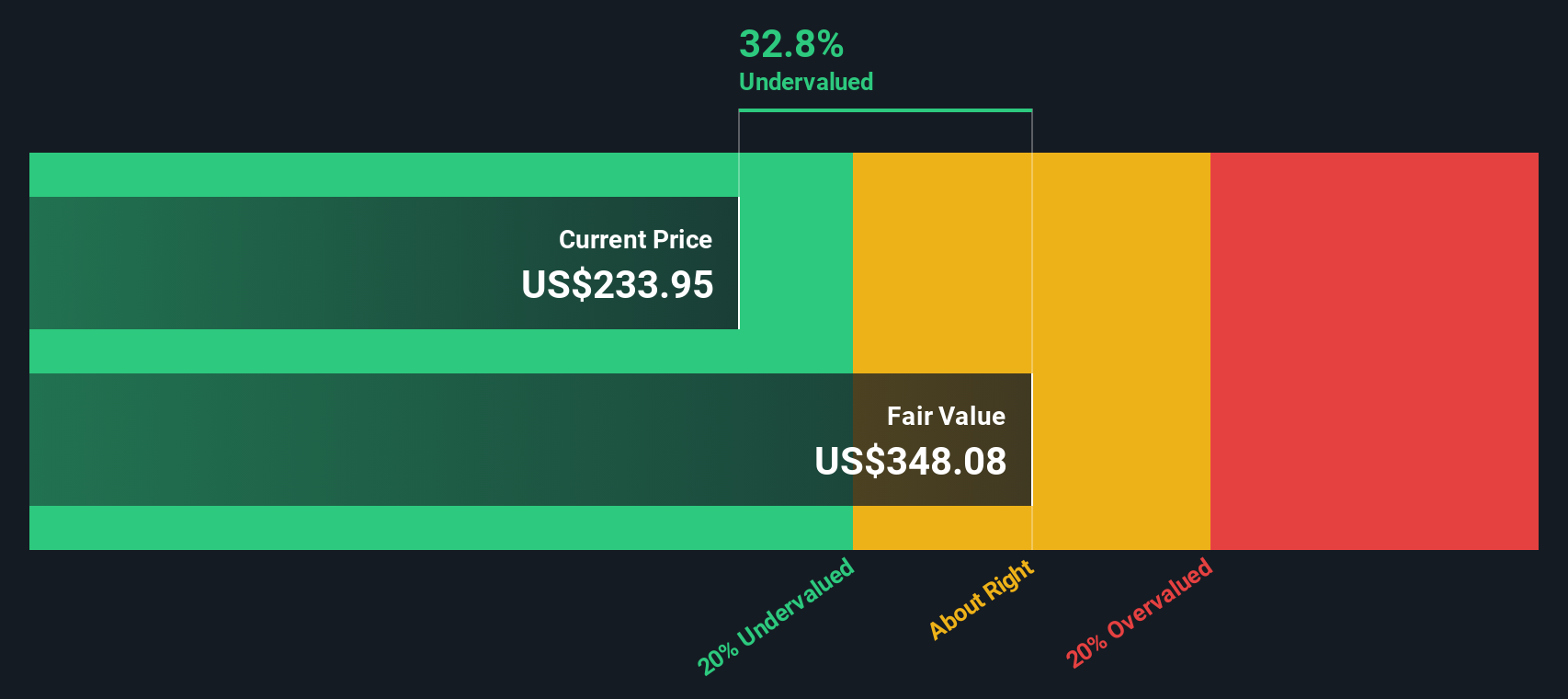

Another View: Cash Flows Tell a Different Story

While the popular narrative suggests Clean Harbors is about 10% overvalued on earnings assumptions, our DCF model points a different way. At $260.95, the shares sit roughly 25% below an estimated future cash flow value of $349.79. This frames today’s price as a potential gap in sentiment rather than fundamentals. Which signal do you put more weight on: an earnings multiple or the cash flows behind it?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Clean Harbors for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 868 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Clean Harbors Narrative

If you see the story differently or prefer to work through the assumptions yourself, you can build your own view in just a few minutes. To begin, use Do it your way.

A great starting point for your Clean Harbors research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Clean Harbors caught your attention, do not stop there. Broaden your watchlist with other angles and keep your next potential move within reach.

- Spot emerging names early by scanning these 3533 penny stocks with strong financials that already show stronger balance sheets and business quality than many expect at this size.

- Position yourself at the intersection of healthcare and automation by reviewing these 107 healthcare AI stocks that apply data and algorithms to real world medical problems.

- Target potential mispricings by filtering for these 868 undervalued stocks based on cash flows where current prices sit below estimated cash flow based assessments.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com