- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

AAON (AAON) Valuation Check As Cash Flow Strains Meet Earnings And Leadership Changes

AAON (AAON) is heading into its February 26, 2026 earnings report with several moving pieces, including margin pressure, higher capital needs, new leadership and fresh credit capacity for potential investment.

See our latest analysis for AAON.

At a share price of $95.24, AAON has seen a 16.89% 1 month share price return and a 20.27% year to date share price return. Its 1 year total shareholder return of 16.73% contrasts with much stronger 3 and 5 year total shareholder returns, suggesting long term holders have fared better than more recent investors while near term momentum has picked up ahead of earnings and management changes.

If AAON's recent move has caught your eye, this could be a useful moment to widen the lens and check out aerospace and defense stocks as another pocket of industrial exposure.

With AAON trading at $95.24, carrying mixed recent returns and flagged for weaker margins and free cash flow, the key question is whether these risks are already reflected in the price or if the market is still incorporating expectations for future growth.

Most Popular Narrative: 17.4% Undervalued

With AAON closing at $95.24 against a narrative fair value of $115.25, the most widely followed view is building in a meaningful valuation gap tied to future growth and margin recovery.

The company is overcoming short-term operational disruptions related to its ERP rollout, with visible progress in production efficiency and a strong, favorably priced backlog, supporting expectations for accelerating top-line growth and margin recovery in the second half of 2025 and into 2026. (Impacts revenue and gross margins)

Curious what earnings power and margin profile this narrative is baking in, and how long AI related demand needs to hold up for that math to work?

Result: Fair Value of $115.25 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside view still hinges on smoother ERP rollouts and data center demand holding up, while high capital spending and cash flow pressure remain key swing factors.

Find out about the key risks to this AAON narrative.

Another Way To Look At AAON's Valuation

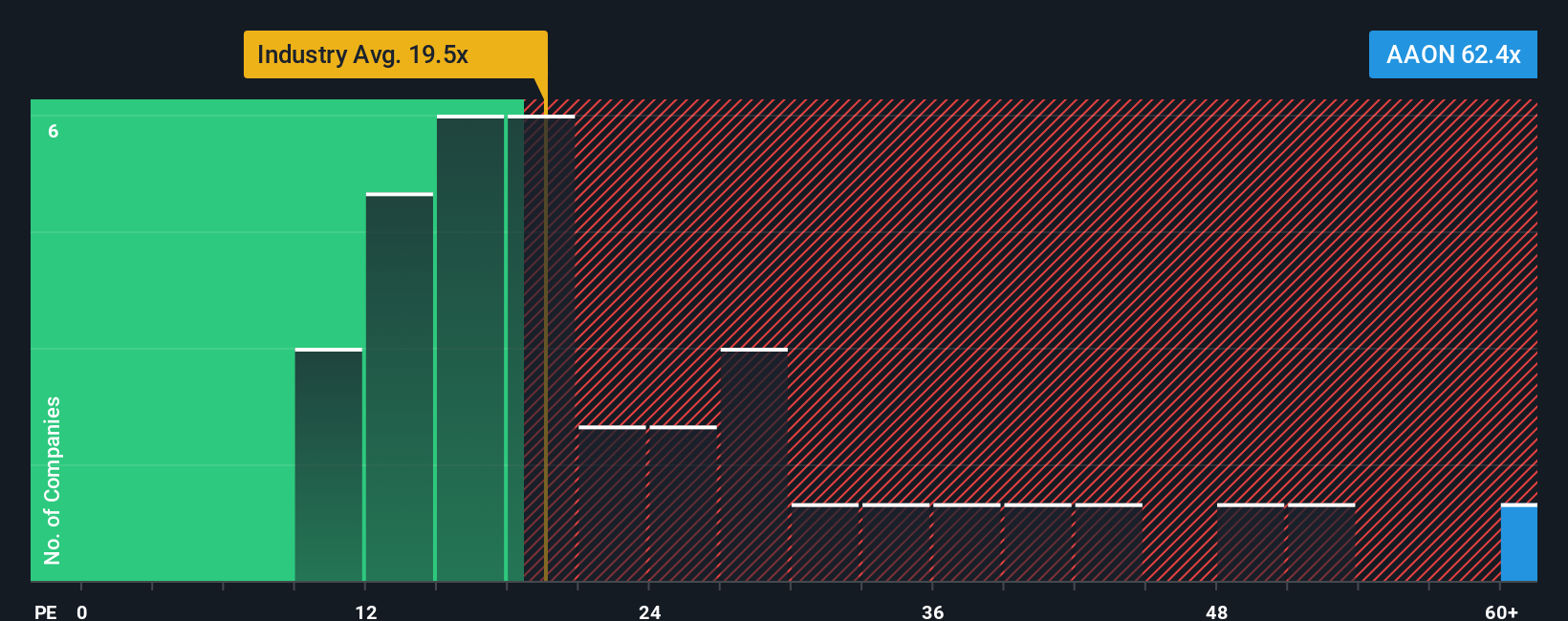

The narrative points to a fair value of $115.25 and frames AAON as undervalued, but the current P/E of 77.5x tells a very different story compared with the US Building industry at 21.5x, peers at 37.9x and a fair ratio of 47.4x, which all suggest meaningful valuation risk if expectations cool.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own AAON Narrative

If you see the data differently or prefer to piece things together yourself, you can build a custom AAON view in minutes with Do it your way.

A great starting point for your AAON research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If AAON has sparked your interest, do not stop here. Broaden your watchlist with a few focused idea sets that could surface your next move.

- Target potential bargains by scanning these 868 undervalued stocks based on cash flows that the market may have priced conservatively based on their cash flows.

- Explore trends in automation and machine learning by checking out these 27 AI penny stocks that are shaping developments in tech demand.

- Position your portfolio for income by reviewing these 11 dividend stocks with yields > 3% that offer yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com