- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Why Photronics (PLAB) Is Down 5.6% After Raising 2026 Capex Guidance And Beating EPS Estimates

- In its latest reported quarter, Photronics, Inc. delivered adjusted EPS of US$0.60 versus US$0.45 expected on revenue of US$216,000,000, and sharply raised its 2026 capital expenditure guidance to US$330,000,000 from around US$190,000,000 in 2025.

- Management also highlighted Photronics’ position as the only U.S.-headquartered producer of trusted photomasks with the country’s only commercial high-end trusted mask facility, underscoring the company’s geopolitical importance in semiconductor supply chains.

- We’ll now examine how Photronics’ significant 2026 capex increase reshapes its investment narrative, particularly around capacity expansion and long-term positioning.

We've found 11 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

What Is Photronics' Investment Narrative?

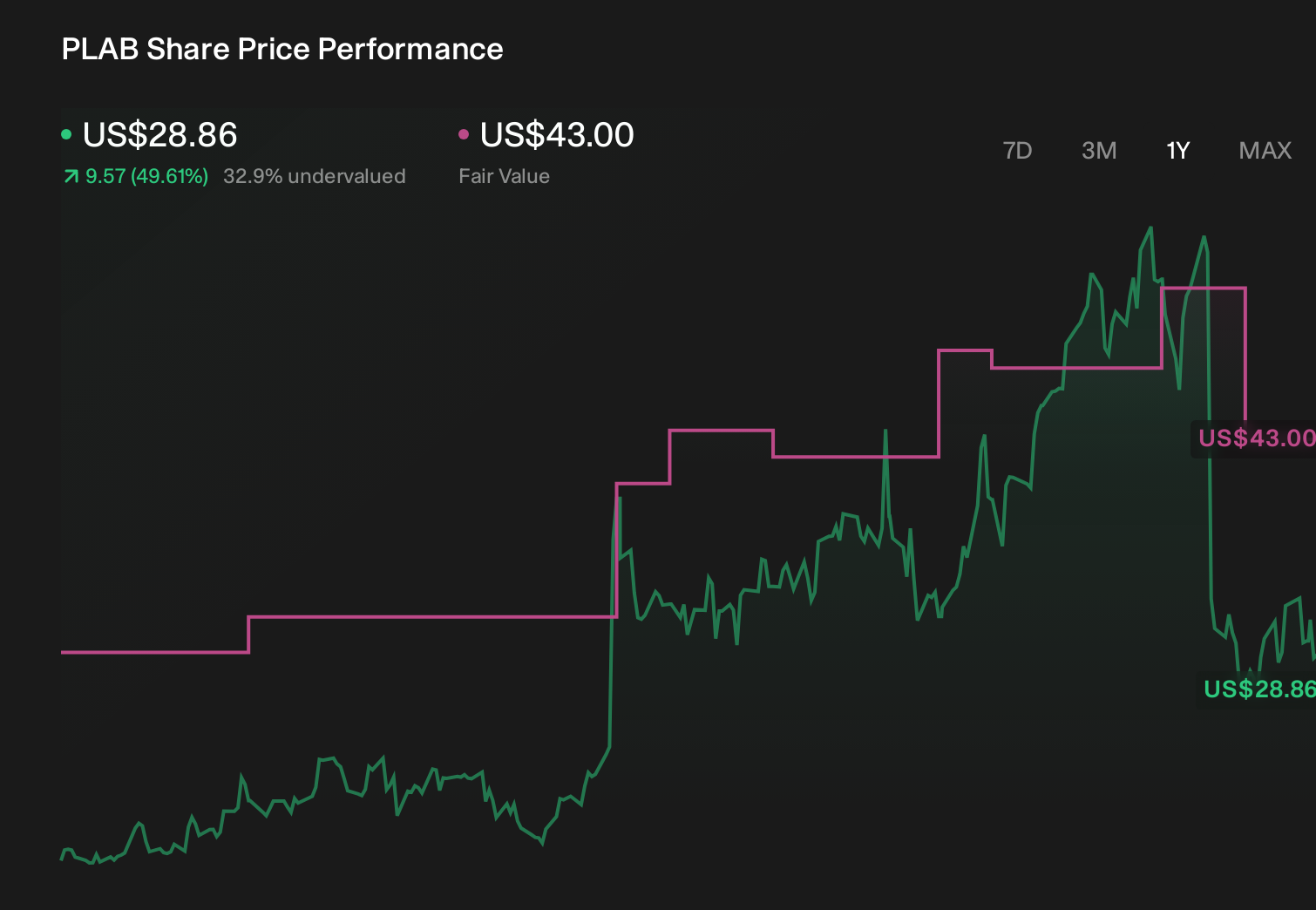

To own Photronics, you have to believe its niche in trusted U.S. photomasks and disciplined capital allocation can matter more than its relatively low forecast growth and volatile share price. The latest beat on earnings and revenue, paired with a big jump in 2026 capex guidance to US$330,000,000, reinforces a story centered on capacity build‑out and deeper engagement with high‑value customers rather than near‑term margin optimization. In the short term, the stronger guidance for next quarter’s revenue and the ongoing buyback program remain key sentiment drivers, while the capex step‑up tilts the catalyst mix toward execution on new tools and facilities. At the same time, higher spending and a relatively new management team add operational and capital allocation risk that now sit more squarely in focus.

However, a much heavier capex load is a risk investors should understand in detail. Photronics' share price has been on the slide but might be dropping deeper into value territory. Find out whether it's a bargain at this price.Exploring Other Perspectives

Explore 8 other fair value estimates on Photronics - why the stock might be worth as much as 24% more than the current price!

Build Your Own Photronics Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Photronics research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Photronics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Photronics' overall financial health at a glance.

Want Some Alternatives?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Outshine the giants: these 27 early-stage AI stocks could fund your retirement.

- AI is about to change healthcare. These 107 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- This technology could replace computers: discover 23 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com