- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Kanzhun (NasdaqGS:BZ) Valuation After Recent Share Capital And Governance Changes

Share capital changes put Kanzhun (NasdaqGS:BZ) governance structure in focus

Kanzhun (NasdaqGS:BZ) has drawn attention after recent changes to its share capital, including new Class A shares from employee option exercises and the conversion of 3,904,000 Class B shares into Class A stock.

For investors, this kind of shift in share classes can influence views on governance and voting power, as well as the liquidity profile of the stock in regular trading.

See our latest analysis for Kanzhun.

At a share price of $18.80, Kanzhun’s 1 day share price return of 1.51% contrasts with a 30 day share price return of a 10.09% decline. The 1 year total shareholder return of 28.51% and 3 year total shareholder return of a 14.13% decline suggest recent momentum has cooled compared to longer term performance, with the latest share capital changes likely feeding into how investors view governance and risk.

If you are weighing Kanzhun alongside other tech driven recruitment and AI names, it could be a good moment to broaden your search with high growth tech and AI stocks.

With Kanzhun trading at $18.80 and internal estimates pointing to a sizeable intrinsic discount, the key question is whether this gap reflects mispricing or whether the market is already factoring in future growth.

Most Popular Narrative: 27.6% Undervalued

The most followed narrative puts Kanzhun’s fair value at $25.98, well above the current $18.80 share price. This frames a clear valuation gap for investors to assess.

Operating leverage through cost control, efficiency gains from AI integration across R&D and customer service, and a robust two-sided network effect are together driving margin expansion, suggesting continued improvement in net margins and profitability.

Curious what this margin story really assumes? Revenue climbing, earnings compounding and a higher profit share on every extra dollar of sales. The full narrative joins those dots.

Result: Fair Value of $25.98 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this upside story still relies on assumptions that could be challenged if competitive intensity reduces margins or if China’s hiring cycle weakens more than expected.

Find out about the key risks to this Kanzhun narrative.

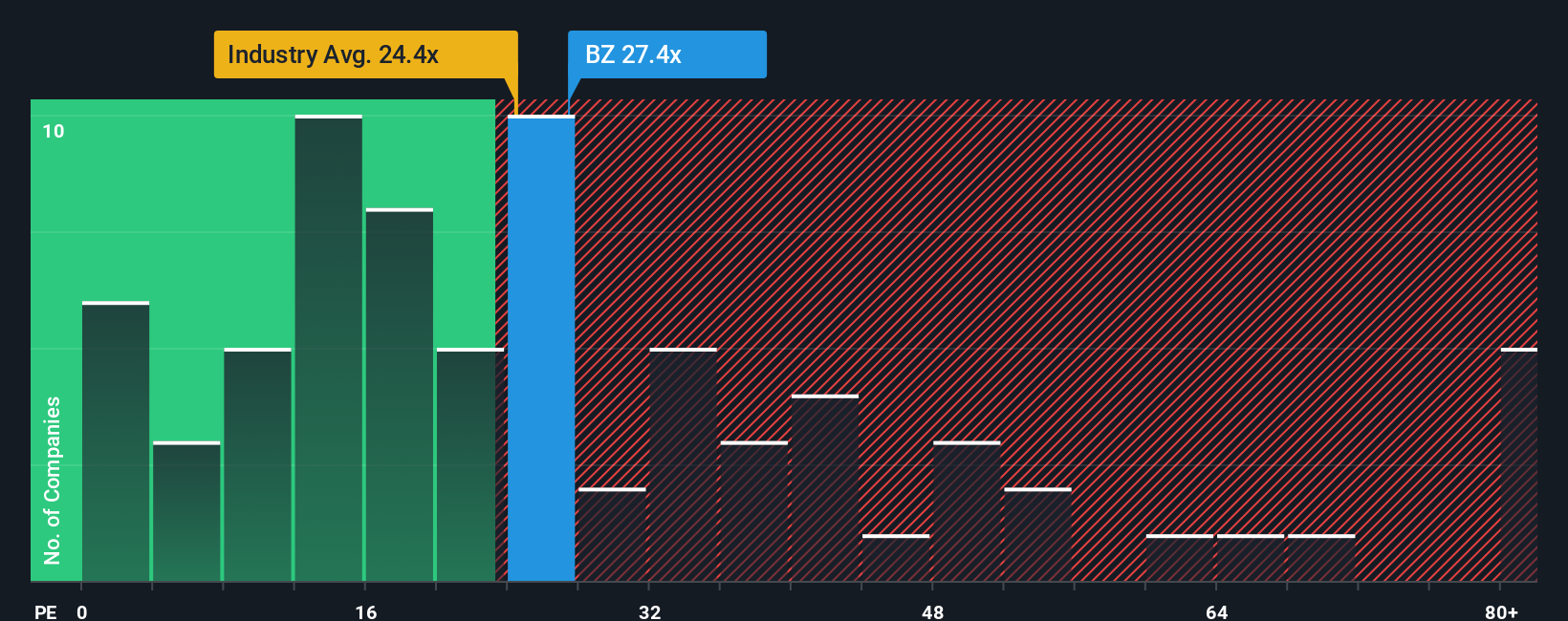

Another View: Earnings Multiple Sends A Different Signal

The narrative and our fair value estimate of $25.98 suggest Kanzhun looks 27.6% undervalued, yet the current P/E of 24.4x paints a more cautious picture. It is higher than both the US Professional Services industry at 23.3x and the peer average at 18.4x, even though the fair ratio sits at 26.7x.

In practice, that means you are paying a richer price than many peers today, while the market still sits below where our fair ratio suggests it could drift. Is that a margin of safety you are comfortable with, or a premium that needs stronger conviction?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Kanzhun Narrative

If this narrative does not quite fit how you see Kanzhun, take a few minutes to test the data yourself and shape your own view with Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Kanzhun.

Looking for more investment ideas?

If Kanzhun is on your radar, do not stop there. Use the same data driven tools to spot other opportunities that might better fit your goals.

- Target potential bargains by scanning these 875 undervalued stocks based on cash flows that may be trading below what their cash flows suggest.

- Zero in on income potential by reviewing these 13 dividend stocks with yields > 3% that could complement a long term portfolio.

- Tap into future facing themes by checking out these 18 cryptocurrency and blockchain stocks riding the growth of digital assets and blockchain adoption.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com