- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Valley National Bancorp (VLY) Valuation After Record Earnings And Positive Outlook

Valley National Bancorp (VLY) has drawn fresh attention after reporting record fourth quarter and full year 2025 results, with earnings and revenue ahead of analyst expectations and solid growth in loans and deposits.

See our latest analysis for Valley National Bancorp.

The latest results have come alongside a steady upswing in the share price, with a 90 day share price return of 17.5% and a 1 year total shareholder return of 31.33%. This suggests improving sentiment around Valley National Bancorp as earnings, buybacks and board changes land in quick succession.

If strong bank earnings have your attention, it could be a good moment to widen the lens and look at fast growing stocks with high insider ownership for other potential ideas on your radar.

With the share price up strongly over the past year and the latest results beating expectations, investors now face a key question: is Valley National Bancorp still trading at an attractive discount, or is the market already pricing in future growth?

Most Popular Narrative: 10.1% Undervalued

At a last close of $12.62 against a most-followed fair value estimate of about $14.04, the current price sits below that narrative anchor, putting a spotlight on what is baked into those cash flow assumptions and growth forecasts.

Valley's accelerating growth in commercial & specialty deposit accounts, driven by technology investments and targeted market penetration, is likely to yield structurally lower funding costs and enhanced net interest margin as legacy brokered deposits are replaced with lower-cost core deposits, directly supporting revenue and margin expansion.

Curious what kind of revenue climb, margin reset, and earnings power shift need to line up for that fair value to hold together? The narrative focuses on a multi year step up in profitability and a different earnings multiple than today. If you want to see exactly which levers do the heavy lifting in this model, the full story spells them out clearly.

Result: Fair Value of $14.04 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this depends on Valley managing its commercial real estate exposure and regional concentration risks in markets like New Jersey, New York, and Florida, which could unsettle that story.

Find out about the key risks to this Valley National Bancorp narrative.

Another View: Market Pricing Sends A Different Signal

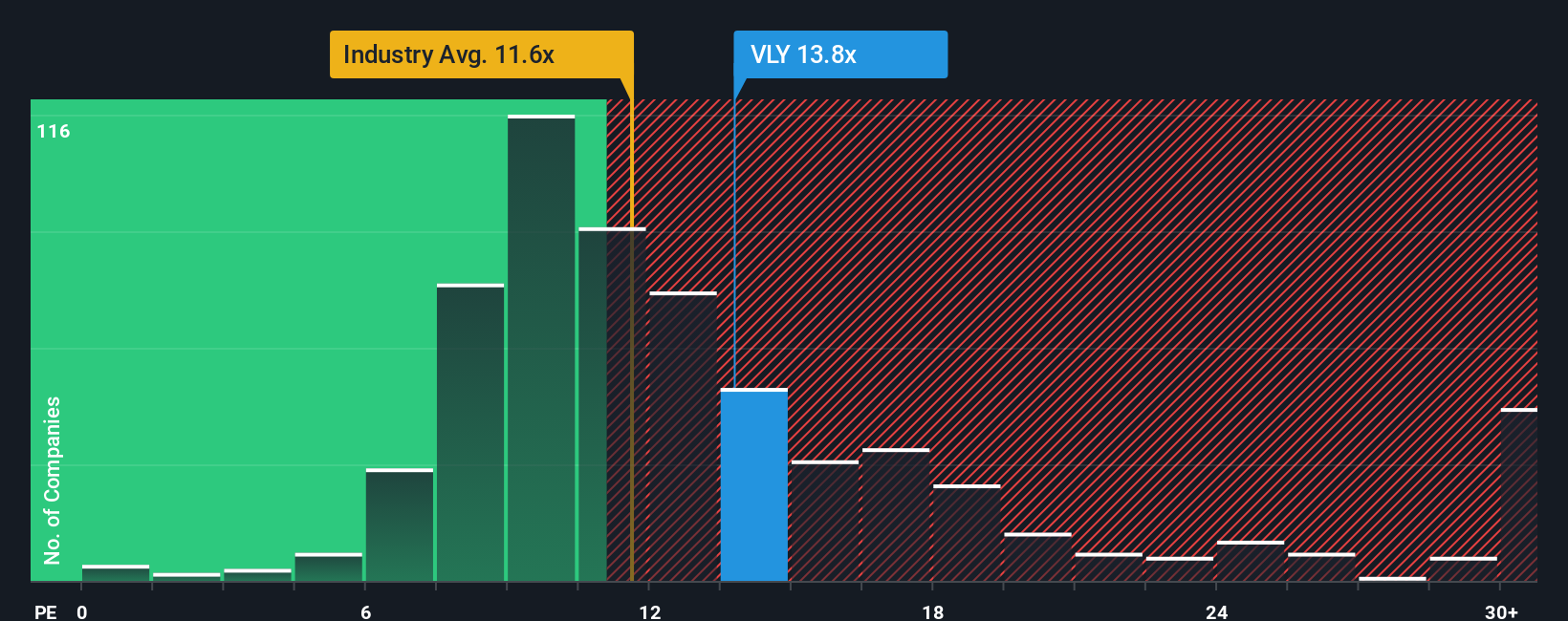

Those cash flow assumptions point to Valley National Bancorp trading well below an implied fair value, but the earnings multiple tells a cooler story. VLY sits on a P/E of 12.3x, a bit richer than the US Banks industry at 11.7x, yet below its fair ratio of 14.7x and peer average of 15.5x. That combination of a slight industry premium and a discount to peers and the fair ratio raises the question of whether the real risk is overpaying or underestimating what could change in the next few years.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Valley National Bancorp Narrative

If your perspective on Valley National Bancorp differs, or you prefer to rely on your own analysis, you can create a personalised narrative in just a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Valley National Bancorp.

Looking for more investment ideas?

If Valley National Bancorp is on your radar, do not stop there. Broaden your watchlist and let data driven ideas surface opportunities you might otherwise miss.

- Spot potential turnaround candidates early by scanning these 3542 penny stocks with strong financials that already show stronger financial foundations than many of their low priced peers.

- Ride long term secular themes by zeroing in on these 24 AI penny stocks positioned at the intersection of artificial intelligence and fast evolving business models.

- Focus on price versus fundamentals by filtering for these 876 undervalued stocks based on cash flows that may offer more attractive cash flow based entry points.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com