- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Adtalem Global Education (ATGE) Valuation After Recent Share Price Pullback

Assessing Adtalem Global Education’s Recent Share Performance

Adtalem Global Education (ATGE) has drawn investor attention after a mixed stretch, with the share price slipping about 4% over the past day and 12% over the past week, despite stronger longer term returns.

See our latest analysis for Adtalem Global Education.

The recent pullback sits against a mixed picture, with a 12.39% 7 day share price decline and a largely flat year to date share price return of 0.88%. The 3 year total shareholder return of 154.30% reflects much stronger longer run outcomes, suggesting near term momentum is fading even as longer term holders have seen considerable value creation.

If Adtalem’s move has you reassessing education and healthcare exposure, it could be a good moment to scan a wider set of healthcare stocks that fit your own criteria.

With Adtalem trading at $103.55 against a US$161.50 analyst target and an indicated intrinsic value gap, yet coming off a flat year and a strong three-year run, are you looking at a genuine opportunity or a market that is already pricing in future growth?

Preferred Multiple of 14.1x P/E: Is It Justified?

On a P/E of 14.1x, Adtalem Global Education screens as undervalued compared with both peers and what the SWS fair ratio suggests, even after the recent share pullback.

The P/E multiple compares the current share price with earnings per share, so a lower P/E than peers can indicate the market is paying less for each dollar of earnings. For a mature, profitable education and healthcare group with $1,888.83m of revenue and $253.98m of net income, this metric is a straightforward way to line up price against the earnings profile investors are currently paying for.

Here, Adtalem trades at a 14.1x P/E while the estimated fair P/E is 19.1x, and both peer and US Consumer Services industry averages sit higher at 20.2x and 16.2x respectively. That is a wide gap. If the market moved closer to the fair ratio level, it would imply a higher price being applied to the same earnings base.

Explore the SWS fair ratio for Adtalem Global Education

Result: Price-to-earnings of 14.1x (UNDERVALUED)

However, you also have to weigh the 1 year total return decline, as well as any potential shifts in healthcare education demand that could challenge the current valuation gap.

Find out about the key risks to this Adtalem Global Education narrative.

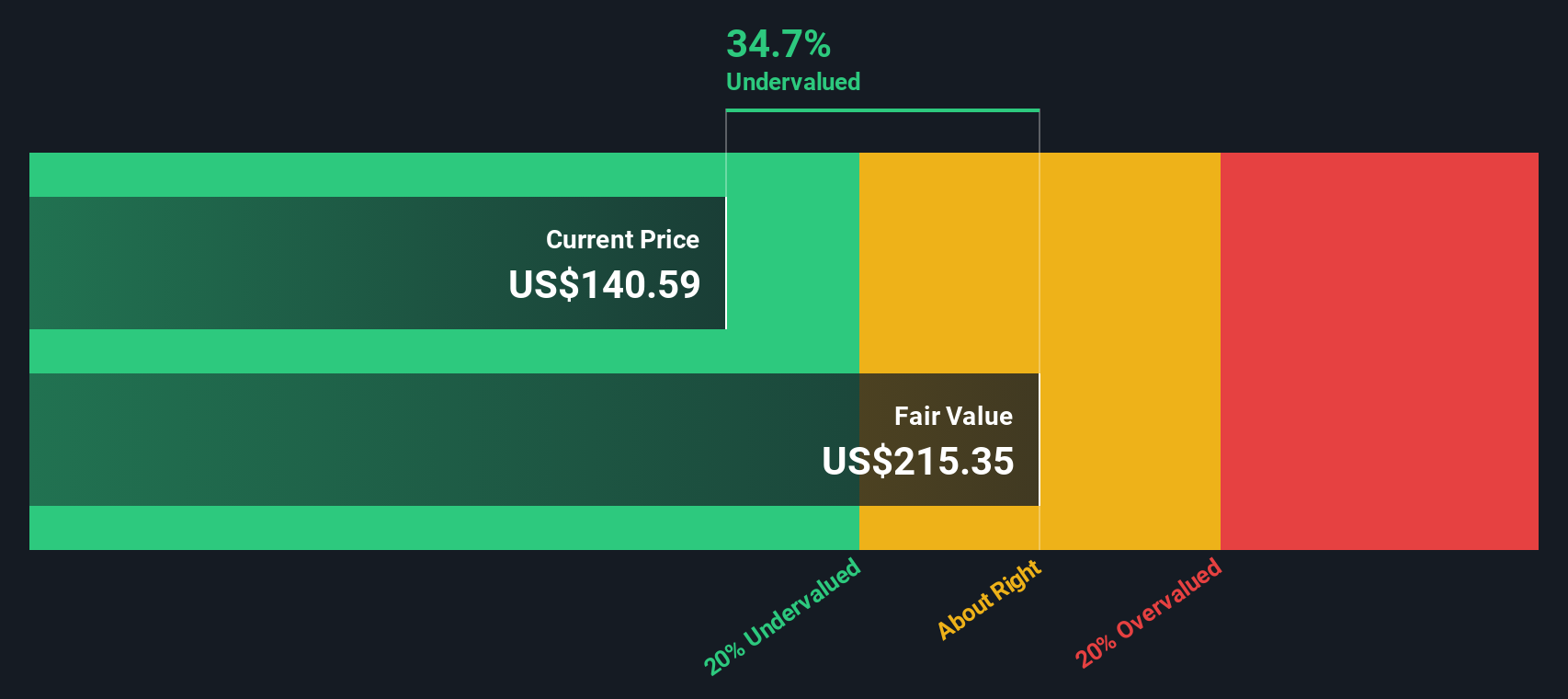

Another View: Cash Flows Point to a Deeper Discount

While the 14.1x P/E suggests Adtalem Global Education is priced below peers, our DCF model goes further. On this view, the shares at $103.55 sit about 54.2% below an estimated fair value of $225.87. This represents a much steeper gap for you to weigh.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Adtalem Global Education for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 887 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Adtalem Global Education Narrative

If this view does not fully sit with you, or you would rather rely on your own work, you can build a fresh narrative in minutes with Do it your way.

A good starting point is our analysis highlighting 5 key rewards investors are optimistic about regarding Adtalem Global Education.

Looking for more investment ideas?

If you are weighing your next move after reviewing Adtalem, consider using these focused stock sets to pressure test and refine your wider watchlist.

- Target potential future income by scanning these 12 dividend stocks with yields > 3% to help you explore a portfolio centered on cash returns rather than short term price moves.

- Spot growth themes by checking these 24 AI penny stocks that link artificial intelligence applications with listed companies already in the market.

- Search for value by reviewing these 887 undervalued stocks based on cash flows that compare current prices with underlying cash flow profiles across different sectors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com