- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Easterly Government Properties (DEA) Valuation After Strong Quarterly Results And Recent Share Price Gains

Quarterly results move Easterly Government Properties (DEA) into focus

On October 27, Easterly Government Properties (DEA) reported quarterly results that management described as supporting consistent, compounding growth. This message coincided with an 11% stock gain over the past month.

See our latest analysis for Easterly Government Properties.

That upbeat earnings message has arrived after a mixed run, with an 8.3% 30 day share price return and 6.9% 90 day share price return, but a 1 year total shareholder return of a 10.9% decline. This suggests recent momentum is improving from a weaker longer term record.

If these results have you looking beyond government focused real estate, it could be a good moment to widen your search with fast growing stocks with high insider ownership for fresh ideas.

With Easterly Government Properties trading close to its analyst price target yet carrying a sizeable modelled intrinsic discount, you have to ask whether this reflects mispricing or whether the market is already incorporating expectations about future growth.

Most Popular Narrative: 4% Undervalued

With Easterly Government Properties last closing at $23.13 against a narrative fair value of $24.08, the current story centers on a modest valuation gap rather than a deep discount or premium.

The federal government's ongoing modernization and renewal of real estate procurement, as evident from recent multi-year lease renewals with built-in rent escalators, positions Easterly to capture rent growth and maintain high tenant retention, positively influencing both revenue and net operating income.

Want to see what this calm, government backed cash flow story is really pricing in? The narrative leans on measured revenue growth, steady margins and a future earnings profile that requires a higher multiple than the sector usually commands. Curious how those moving parts combine into that fair value estimate and modest discount? Read on to see the full narrative behind the number.

Result: Fair Value of $24.08 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still pressure points, such as higher capital costs and government efforts to streamline real estate footprints, that could challenge this calm cash flow story.

Find out about the key risks to this Easterly Government Properties narrative.

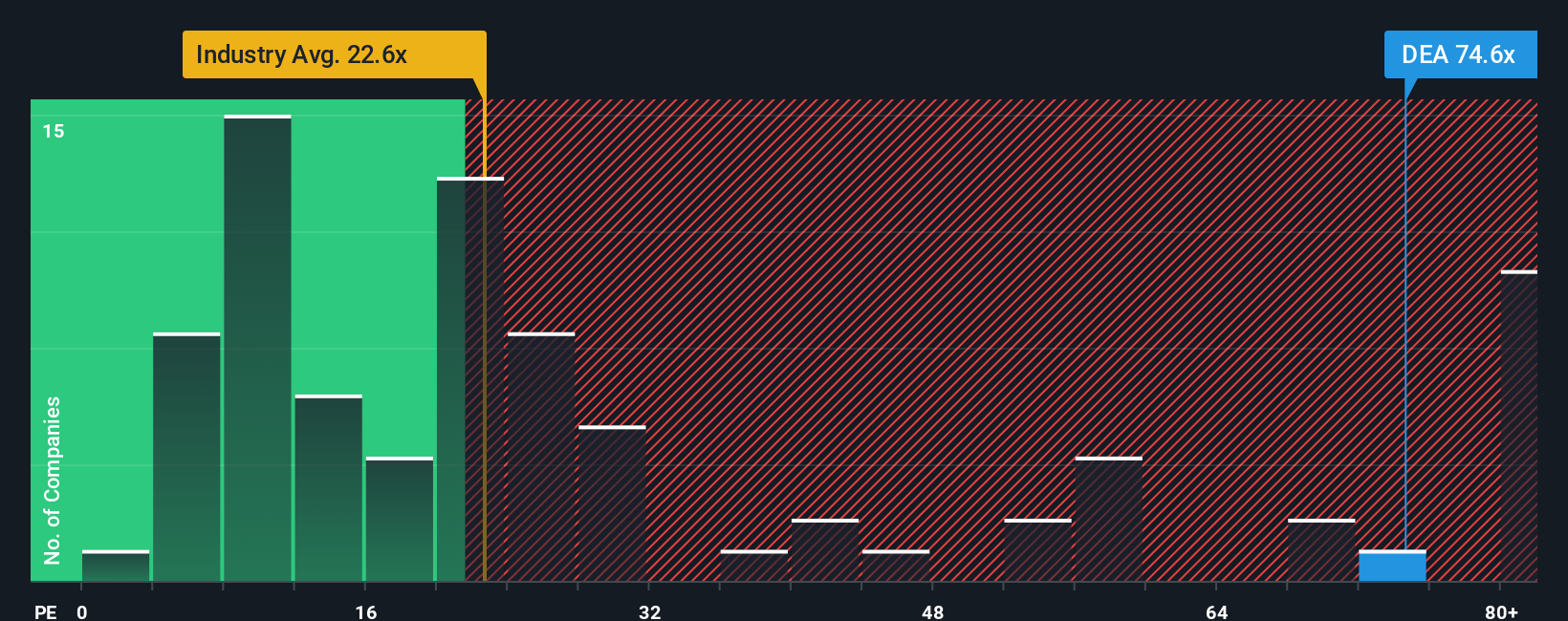

Another View: Rich P/E Keeps The Story In Check

There is a clear tension between the narrative fair value of $24.08 and how the market is already pricing Easterly today. The shares trade on a P/E of 80.4x, compared with 45.5x for peers, 22.1x for the wider Office REITs group and a fair ratio of 36.7x. That gap points to real valuation risk if expectations fade. How comfortable are you paying more than double that fair ratio for modest growth?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Easterly Government Properties Narrative

If this framework does not quite fit how you see Easterly, or you would rather work from the raw numbers yourself, you can build a narrative that reflects your own view in just a few minutes, starting with Do it your way.

A great starting point for your Easterly Government Properties research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If Easterly has you thinking differently about risk and reward, do not stop here, use the Simply Wall St Screener to spot other compelling opportunities right now.

- Spot potential turnaround stories by checking out these 3526 penny stocks with strong financials that already show stronger balance sheets and improving fundamentals.

- Position yourself early in structural tech shifts by scanning these 23 AI penny stocks shaping the way data, automation and decision making come together.

- Focus on price and cash flow discipline by reviewing these 865 undervalued stocks based on cash flows that may offer more attractive entry points than well known names.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com