- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

WesBanco (WSBC) Net Interest Margin Strength Challenges Bearish Credit Narratives

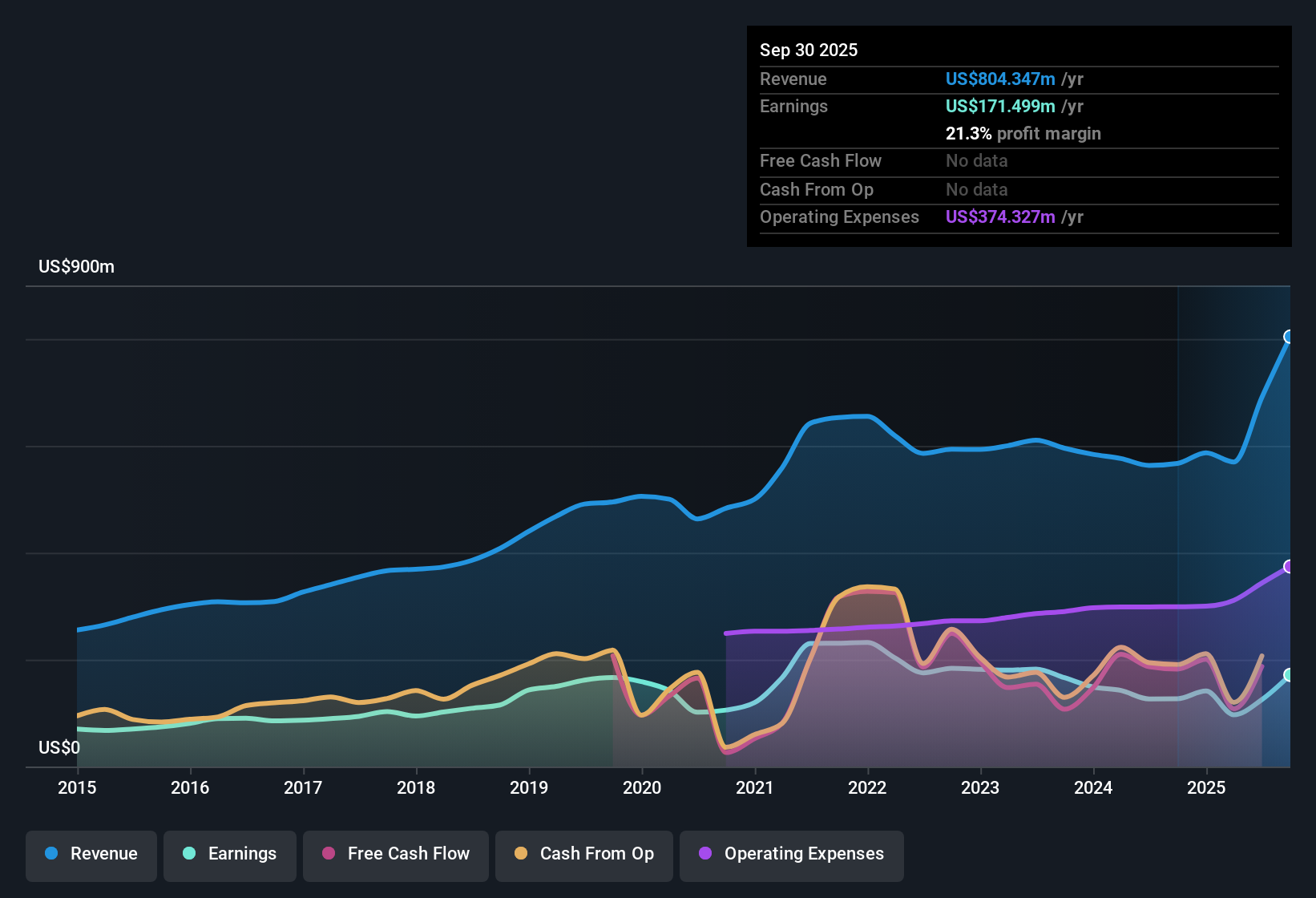

WesBanco (WSBC) has just wrapped up FY 2025 with fourth quarter revenue of US$262.5 million and basic EPS of US$0.81, capping a trailing twelve months where revenue reached US$903.8 million and EPS came in at US$2.23. Over the last few quarters, revenue has moved from US$163.0 million in Q4 2024 to US$262.5 million in Q4 2025, while quarterly EPS shifted from US$0.70 to US$0.81. This sets the scene for investors to weigh those earnings against shifting profit margins and credit quality.

See our full analysis for WesBanco.With the headline numbers on the table, the next step is to see how this earnings run rate lines up with the stories investors follow about WesBanco, and where the latest figures push back against those narratives.

Curious how numbers become stories that shape markets? Explore Community Narratives

Margins And One Offs Shape FY 2025 Story

- Across the last 12 months, WesBanco converted US$903.8 million of revenue into US$202.6 million of net income, which works out to a 22.4% net profit margin compared with 24.1% a year earlier, while that period also included a one off loss of US$75.9 million.

- What is interesting for a bullish view is that earnings grew 43.3% over the year even though the margin eased and there was that US$75.9 million one off loss, which means:

- Bulls pointing to a 43.3% earnings improvement can also point to the higher net interest margin on a trailing basis at 3.53% versus 2.96% a year earlier as support.

- At the same time, the five year earnings trend shows a 6.9% annual decline, so anyone leaning bullish needs to weigh the recent rebound against that longer history.

Loan Book Expansion And Credit Quality

- Total loans in the quarterly data stepped from US$12,451.4 million in Q3 2024 to US$18,932.1 million in Q3 2025, while non performing loans in those quarters were US$30.4 million and US$94.5 million respectively.

- Critics who lean bearish often focus on asset quality, and the move in non performing loans alongside higher earnings gives them data to point to:

- Bears can highlight that non performing loans in the trailing data rose from US$30.4 million in Q3 2024 to US$94.5 million in Q3 2025 while the net profit margin eased from 24.1% to 22.4%.

- On the other hand, the bank still reported US$202.6 million of net income over the last 12 months and a 3.53% net interest margin, which shows earnings remained positive even with higher reported problem loans.

Valuation Gap And Dividend Trade Off

- The shares trade at a P/E of 16.3x versus 11.8x for the US banks industry and 15.7x for peers, while the DCF fair value supplied here is US$70.30 against a current share price of US$34.30 and the dividend yield is 4.43%.

- Supporters with a bullish tilt can point to several numbers that differ from a typical regional bank profile, which creates an interesting mix for income and value focused investors:

- They can argue that a 4.43% dividend yield alongside a P/E only modestly above peers at 16.3x looks supported when earnings grew 43.3% over the last year and revenue growth is forecast at 12.9% per year.

- At the same time, the P/E premium and substantial shareholder dilution over the past year sit against the idea of a bargain, even with the DCF fair value of US$70.30 implying a large gap to the current US$34.30 price.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on WesBanco's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

WesBanco’s softer net margin, rising non performing loans, and higher P/E compared with the US banks industry raise questions about the quality of its earnings profile.

If those pressure points leave you wanting sturdier foundations, use our CTA_SCREENER_SOLID_BALANCE_SHEET to quickly zero in on companies with stronger balance sheets and cleaner credit trends.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com