- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At KE Holdings (NYSE:BEKE) Valuation After Earnings Beat And Efficiency Push

Why KE Holdings stock moved on the latest earnings update

KE Holdings (BEKE) recently reported in line revenues with stronger than expected earnings for 3Q25, a combination that appears to have lifted sentiment despite ongoing pressure in China’s property market.

Investors are also focusing on management’s push for operational efficiency and the use of AI across the platform, as these efforts are expected to support margin improvement even while sector headwinds remain.

See our latest analysis for KE Holdings.

KE Holdings’ share price has gained 16.1% over the past month and 16.4% year to date. The 1 year total shareholder return of 9.7% and 3 year total shareholder return of 1.9% suggest only gradual recovery after a much weaker 5 year total shareholder return decline of 68.9%, indicating early but still fragile momentum around the recent earnings and efficiency focus.

If earnings driven moves in real estate have caught your eye, it could be a good moment to widen your watchlist with fast growing stocks with high insider ownership.

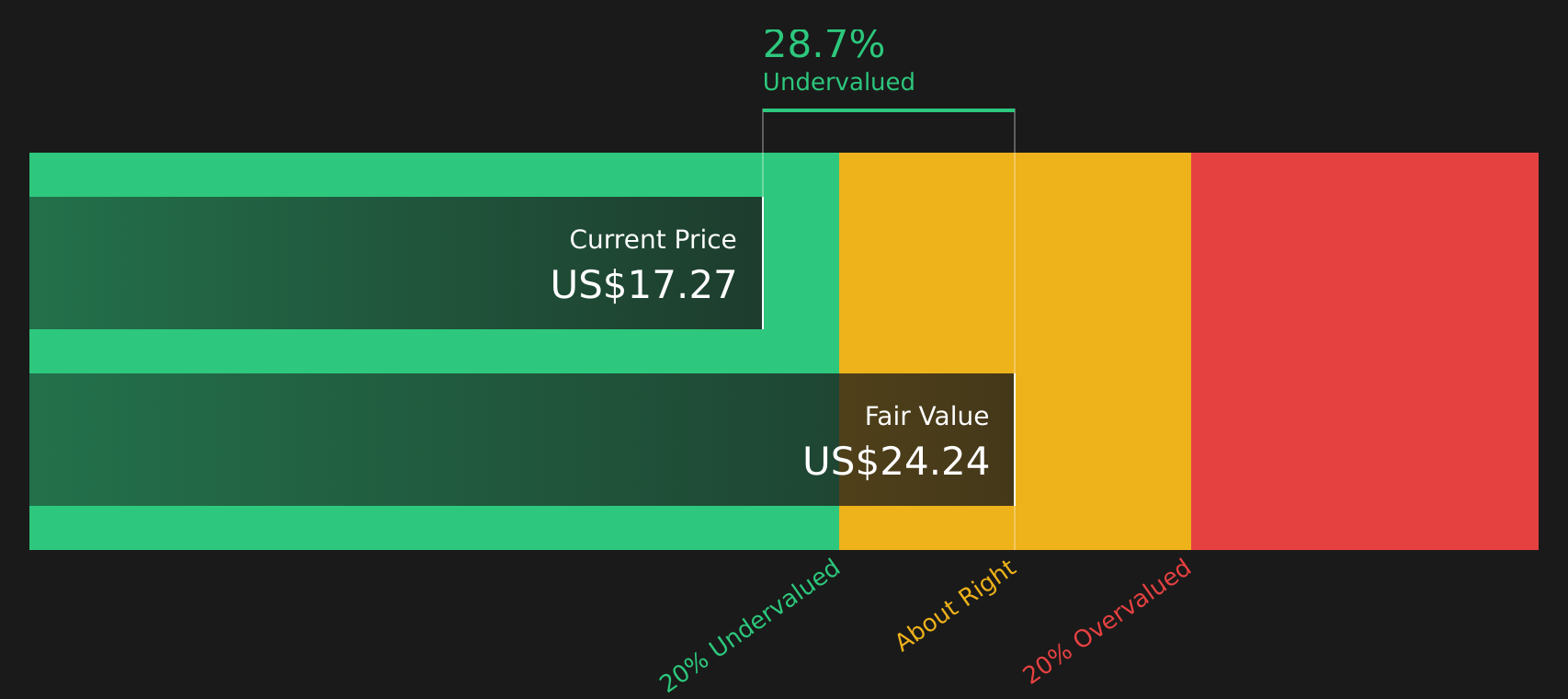

With KE Holdings trading at $18.70 and sitting at roughly a 32% discount to one intrinsic value estimate, as well as a smaller gap to analyst targets, you have to ask: is there still mispricing here, or is future growth already reflected in the price?

Most Popular Narrative: 8.2% Undervalued

KE Holdings’ most followed narrative pegs fair value at $20.37, a little above the recent $18.70 close, which implies the current price does not fully reflect the long term cash flow story behind the model.

KE Holdings is diversifying revenue through rapid expansion of its high margin, recurring service businesses such as home renovation, furniture, and rental services, with these non transactional revenues now comprising 41% of total sales, reducing cyclicality and supporting more stable revenue and higher blended margins as the platform matures.

Curious what kind of revenue mix, profit margins, and valuation multiple have to line up for that fair value to make sense? The narrative leans on a specific growth path, a tighter share count, and a required return of 9.88% to get there. The detail sits in how earnings are expected to scale against that discount rate over the next few years.

Result: Fair Value of $20.37 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the story could change quickly if China’s property slump drags on, or if expansion into renovation and rental services adds cost without delivering the expected earnings support.

Find out about the key risks to this KE Holdings narrative.

Another way to look at valuation

The Simply Wall St DCF model paints a stronger picture than the earnings based fair value. On this view, KE Holdings at $18.70 is trading below an estimated future cash flow value of $27.68, which points to an undervalued setup rather than just a mild discount. Which story do you trust more: the cash flows or the earnings multiple?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own KE Holdings Narrative

If you look at the numbers and come to a different conclusion, or just prefer to build from your own assumptions, you can shape a custom KE Holdings story in a few minutes and Do it your way.

A great starting point for your KE Holdings research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If KE Holdings is on your radar, do not stop there; widening your search now can help you spot opportunities that others might overlook.

- Scan for early stage growth stories that still sit at lower share prices by checking out these 3521 penny stocks with strong financials with solid fundamentals behind them.

- Target companies shaping the AI trend in real businesses by reviewing these 23 AI penny stocks that already show real revenue traction.

- Focus on price versus cash flow and hunt for potential mispricing by running through these 868 undervalued stocks based on cash flows that line up with your return expectations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com