- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Corporación América Airports (NYSE:CAAP) Valuation After Seymour Extension And Traffic Growth Update

Corporación América Airports (NYSE:CAAP) is back in focus after two fresh updates: a six year extension of its Seymour Airport concession in the Galápagos and detailed operating results for December and full year 2025.

See our latest analysis for Corporación América Airports.

The latest Seymour extension and traffic update comes after a strong run in the shares, with a 33.82% 90 day share price return and a 46.33% one year total shareholder return, suggesting momentum has been building rather than fading.

If the Seymour Airport news has you thinking more broadly about transport and infrastructure exposure, it could be worth widening your search across auto manufacturers as a different way to tap into global mobility trends.

With the stock up strongly and trading only about 1% below its average analyst price target, yet showing a wide intrinsic value gap on some models, should you view CAAP as still mispriced, or has the market already priced in future growth?

Most Popular Narrative: 1.1% Overvalued

With Corporación América Airports last closing at $29.12 against a most-followed fair value estimate of $28.80, the narrative views the shares as slightly ahead of that modeled value, and it builds this view around detailed assumptions for growth, margins, and future earnings power.

Ongoing major infrastructure investments, such as the Florence Airport Master Plan (recently environmentally approved), expansion projects in Armenia, and future growth opportunities in M&A and concessions, should increase capacity and competitiveness, underpinning future top-line and adjusted EBITDA expansion.

Curious what kind of revenue path, margin uplift, and future P/E level sit behind that fair value? The narrative ties them together with a specific discount rate and a tight earnings roadmap that may surprise you when you see the full picture.

As context, this most popular narrative now anchors on a fair value of $28.80, a modest uplift from prior work, and applies a discount rate of 6.88% to bring its long term cash flow expectations back to today. It couples relatively measured revenue growth assumptions with a meaningful improvement in profitability and a future earnings multiple that sits below where many infrastructure names have been priced, which together help frame why the current price sits only slightly above that fair value mark.

Result: Fair Value of $28.80 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on Argentina’s economic and regulatory backdrop, along with execution on large CapEx and M&A plans, which could strain cash flows if returns disappoint.

Find out about the key risks to this Corporación América Airports narrative.

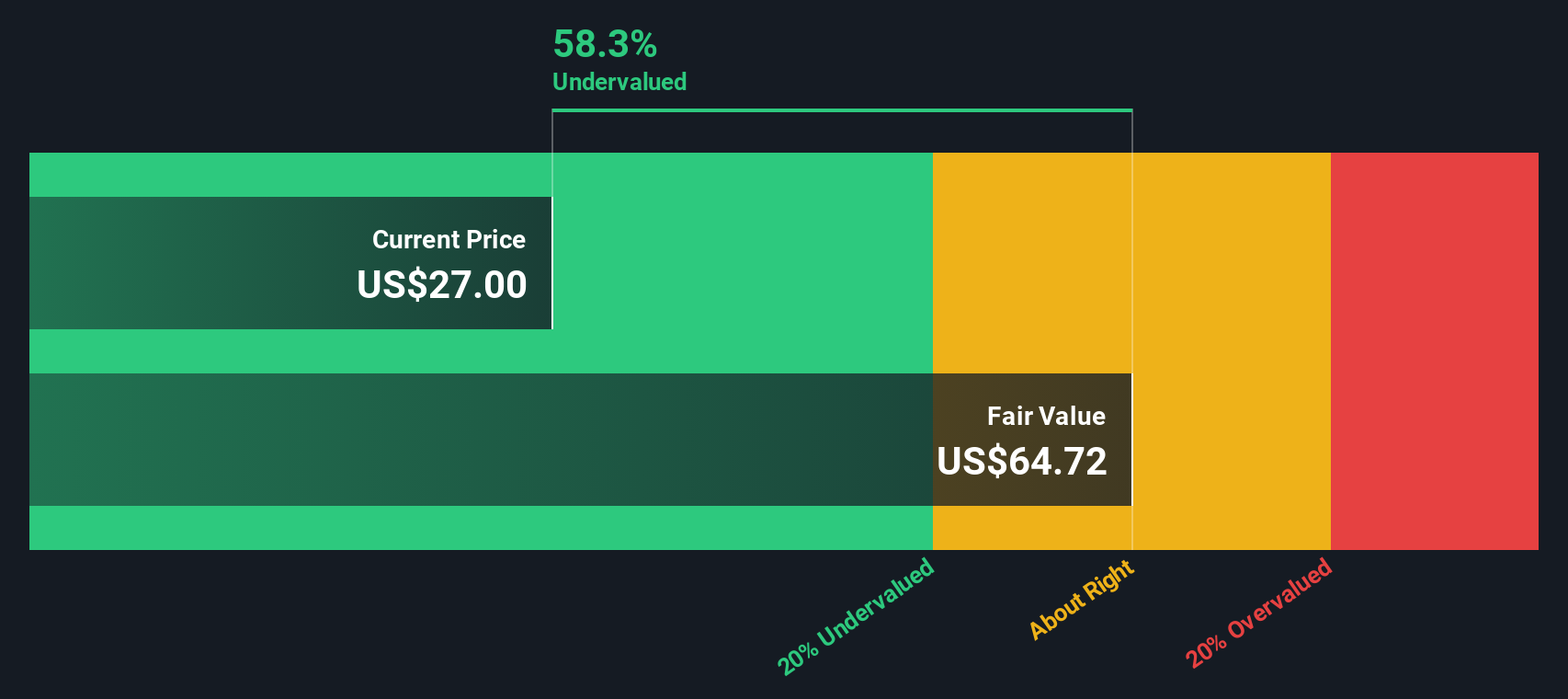

Another View: Big Discount On Cash Flows

While the most followed fair value of $28.80 suggests CAAP is slightly overvalued at $29.12, our DCF model points in a very different direction, with an estimated future cash flow value of $65.10 and a 55.3% discount. Which story do you think fits the risk and execution picture better?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Corporación América Airports for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 877 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Corporación América Airports Narrative

If you look at these numbers and come to a different conclusion, or simply prefer running your own view from the ground up, you can build a full narrative in just a few minutes and see how it stacks up against the consensus, Do it your way.

A great starting point for your Corporación América Airports research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If CAAP has sharpened your focus, do not stop here. Widen your watchlist now so you are not chasing opportunities after they are crowded.

- Zero in on potential high risk, high reward names by reviewing these 3519 penny stocks with strong financials that pair tiny market caps with solid underlying numbers.

- Tap into the growth of artificial intelligence by checking out these 24 AI penny stocks that tie AI themes to smaller, earlier stage companies.

- Hunt for possible mispricings by scanning these 877 undervalued stocks based on cash flows where current prices sit below modeled cash flow value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com