- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Lakeland Financial (LKFN) Credit Quality Improvement Reinforces Bullish Margin Narratives

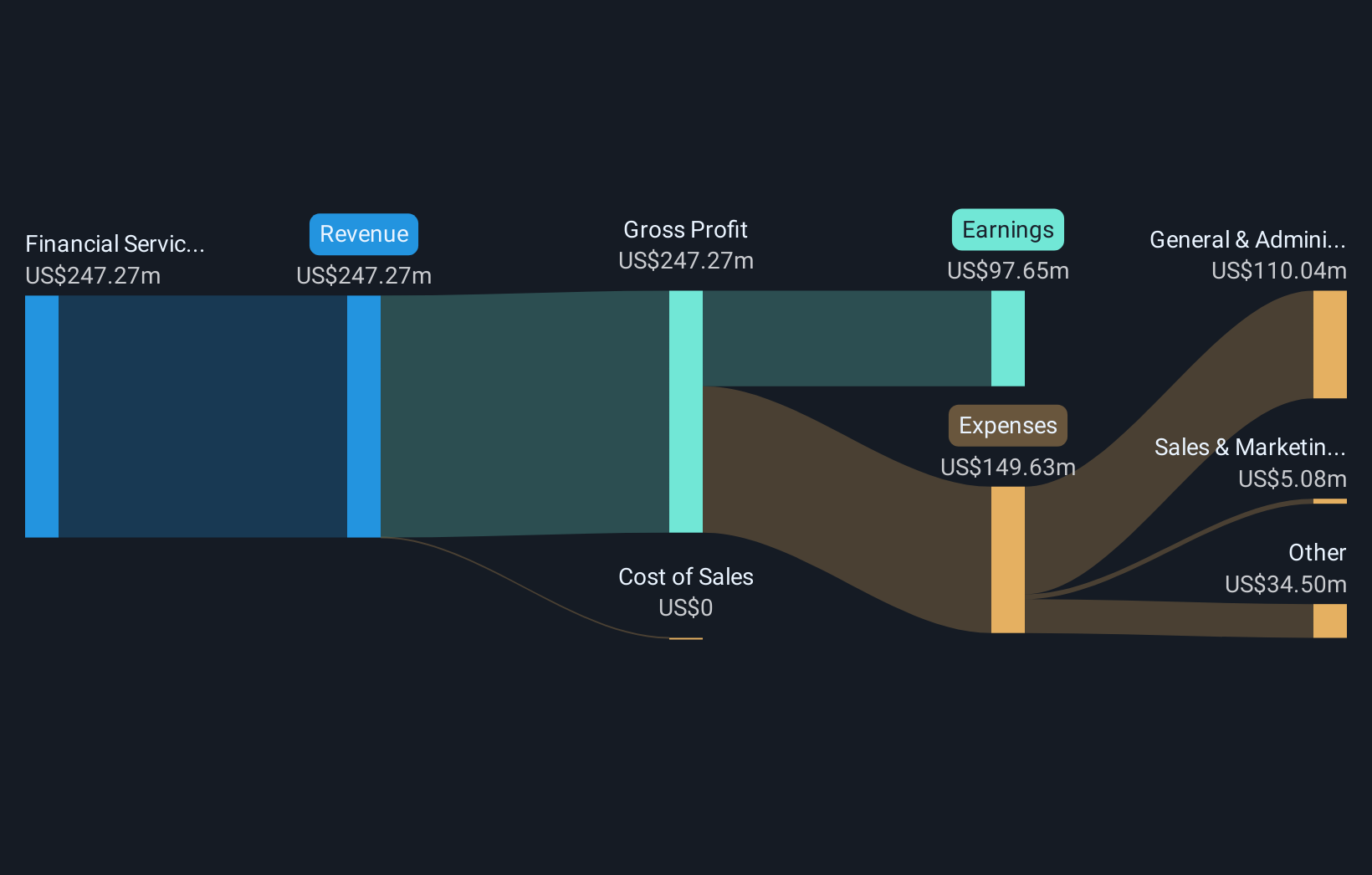

Lakeland Financial (LKFN) closed out FY 2025 with fourth quarter revenue of US$69.8 million and basic EPS of US$1.17, alongside trailing twelve month EPS of US$4.02. Over the past year, total revenue has moved from US$236.8 million on a trailing basis at the end of 2024 to US$257.2 million by the fourth quarter of 2025, while quarterly EPS shifted from US$0.94 in Q4 2024 to US$1.17 in Q4 2025. This gives investors a clear view of how the income line is tracking into the new year. With a trailing net profit margin of 40.2% and a cost to income ratio under 50%, the latest results put profitability squarely in focus for anyone tracking the bank’s earnings power.

See our full analysis for Lakeland Financial.With the headline numbers on the table, the next step is to see how this earnings profile lines up with the widely followed narratives around Lakeland Financial’s growth, risk, and income potential, and where those stories might need a rethink.

Curious how numbers become stories that shape markets? Explore Community Narratives

3.48% net interest margin keeps core banking income solid

- Net interest margin for FY 2025 on a trailing basis sits at 3.45%, with the latest quarter at 3.48%, while quarterly revenue moved from US$57.0 million in Q1 2025 to US$69.8 million in Q4 2025 alongside total loans of US$5.4 billion at year end.

- What stands out for a bullish view is how these income metrics line up with the idea of Lakeland Financial as a steady regional banking franchise, and

- Trailing net income of US$103.4 million on revenue of US$257.2 million points to a business that is turning a relatively stable margin into earnings that support the described high earnings quality.

- Forecast earnings growth of about 5.6% a year and revenue growth of 8.5% a year sit below broader US market forecasts, which can limit how strong that bullish angle looks even with a consistent net interest margin.

Cost to income ratio under 50% supports 40.2% net margin

- The trailing cost to income ratio is 48.93%, with Q4 2025 at 47.92%, sitting alongside a trailing net profit margin of 40.2% that is slightly above the prior year's 39.5% figure.

- Critics who lean bearish on slower growth forecasts may still have to account for these efficiency and margin numbers, because

- On a trailing basis, revenue of US$257.2 million and net income of US$103.4 million show that a relatively low cost base is turning into strong profitability even though forecast earnings growth of 5.6% a year is below the 16.1% US market forecast.

- The combination of a 3.47% dividend yield and a 40.2% net margin means a fair amount of cash is already flowing to shareholders, which sits awkwardly with a purely bearish stance that focuses only on the slower projected top line and earnings growth.

Non performing loans fall to US$20.9 million on a larger book

- Non performing loans have moved from US$57.4 million at the start of FY 2025 to US$20.9 million by Q4 2025, even as total loans rose from US$5.2 billion in Q1 2025 to US$5.4 billion at year end.

- For a bullish angle, this shift in credit quality sits alongside the earnings profile and can be read as supportive of the bank's ability to sustain its high margin and dividend story, because

- Lower non performing loans on a larger loan book reduce the drag from problem credits at the same time as the bank is running a 3.45% trailing net interest margin and a cost to income ratio under 50% on the same trailing view.

- When you put that together with trailing EPS of US$4.02 against a current share price of US$58.13, which implies a P/E of about 14.6x, it helps explain why some investors might focus on credit quality as a key support for the overall bullish thesis even if growth forecasts are more modest than the wider US market.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Lakeland Financial's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Lakeland Financial combines solid margins and credit quality with forecast earnings and revenue growth that sit below broader US market expectations.

If that slower outlook leaves you wanting faster compounding, check out CTA_SCREENER_LARGE_CAP_HIGH_GROWTH_POTENTIAL to focus on established names with stronger growth forecasts that may better align with your objectives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com