- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Zymeworks (ZYME) Valuation After Major Leadership And Board Reshuffle

Zymeworks (ZYME) has announced a broad refresh of its leadership team, including new board appointments and senior executive changes, as it works to align management roles with its updated corporate strategy.

See our latest analysis for Zymeworks.

At a share price of $23.24, Zymeworks has a 90 day share price return of 20.41% and a 1 year total shareholder return of 60.83%. However, the year to date share price return of 12.70% and 30 day share price return of 13.51% suggest some recent momentum has cooled as investors weigh the broad leadership reshuffle and earlier management changes.

If these leadership moves have you thinking about other opportunities in healthcare, it could be a good moment to scan healthcare stocks for ideas that fit your watchlist.

With Zymeworks trading at $23.24 and internal models suggesting a potential intrinsic value premium, the key question is whether recent leadership changes leave additional upside on the table or whether the market is already accounting for future growth.

Most Popular Narrative: 32.6% Undervalued

With Zymeworks closing at $23.24 and the most followed narrative pointing to a fair value of $34.50, the gap between price and narrative is hard to ignore.

The analysts have a consensus price target of $21.05 for Zymeworks based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $30.0, and the most bearish reporting a price target of just $12.0.

Curious what sits behind that higher fair value line? Revenue ramp assumptions, margin shifts, and a punchy future earnings multiple are doing the heavy lifting. Want the full story?

Result: Fair Value of $34.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on partner execution and clinical success, and any delays to milestone payments or pipeline readouts could quickly challenge the royalty driven upside story.

Find out about the key risks to this Zymeworks narrative.

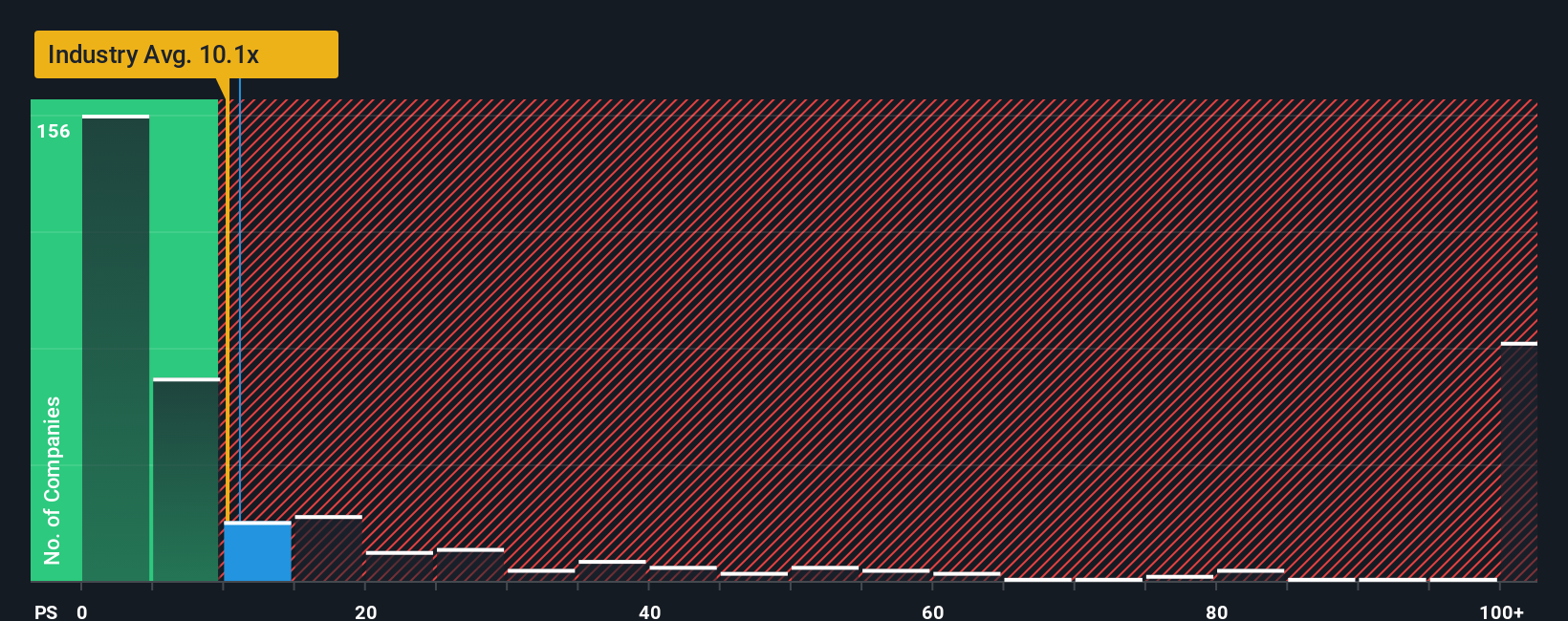

Another View: Multiples Flash A Very Different Signal

That 32.6% gap to a $34.50 fair value is one side of the story. On simple P/S, Zymeworks trades at 12.9x versus a fair ratio of 2.4x and a US Biotechs average of 11.9x, which points to a rich setup. Is this justified by the royalty pivot, or does it leave less room for error?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Zymeworks Narrative

If you are not sold on this view or prefer to lean on your own homework, you can build a custom thesis in minutes with Do it your way.

A great starting point for your Zymeworks research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Zymeworks has caught your attention, do not stop here. A quick pass through a few focused screeners could surface opportunities that fit your next move even better.

- Target potential mispricings by checking stocks that appear cheap on future cash flows through these 876 undervalued stocks based on cash flows before they get more attention.

- Approach the AI theme more deliberately by scanning these 23 AI penny stocks for companies tied to machine learning, automation, and data driven products.

- Build a more income focused watchlist by reviewing these 14 dividend stocks with yields > 3% that may align with your preferred yield and payout profile.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com