- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing UniFirst (UNF) Valuation After Energy Efficiency Upgrades Across 39 Facilities

UniFirst (UNF) is back in focus after completing the first phase of a multi site energy modernization program with Redaptive across 39 U.S. facilities, targeting lower energy costs and improved environmental metrics.

See our latest analysis for UniFirst.

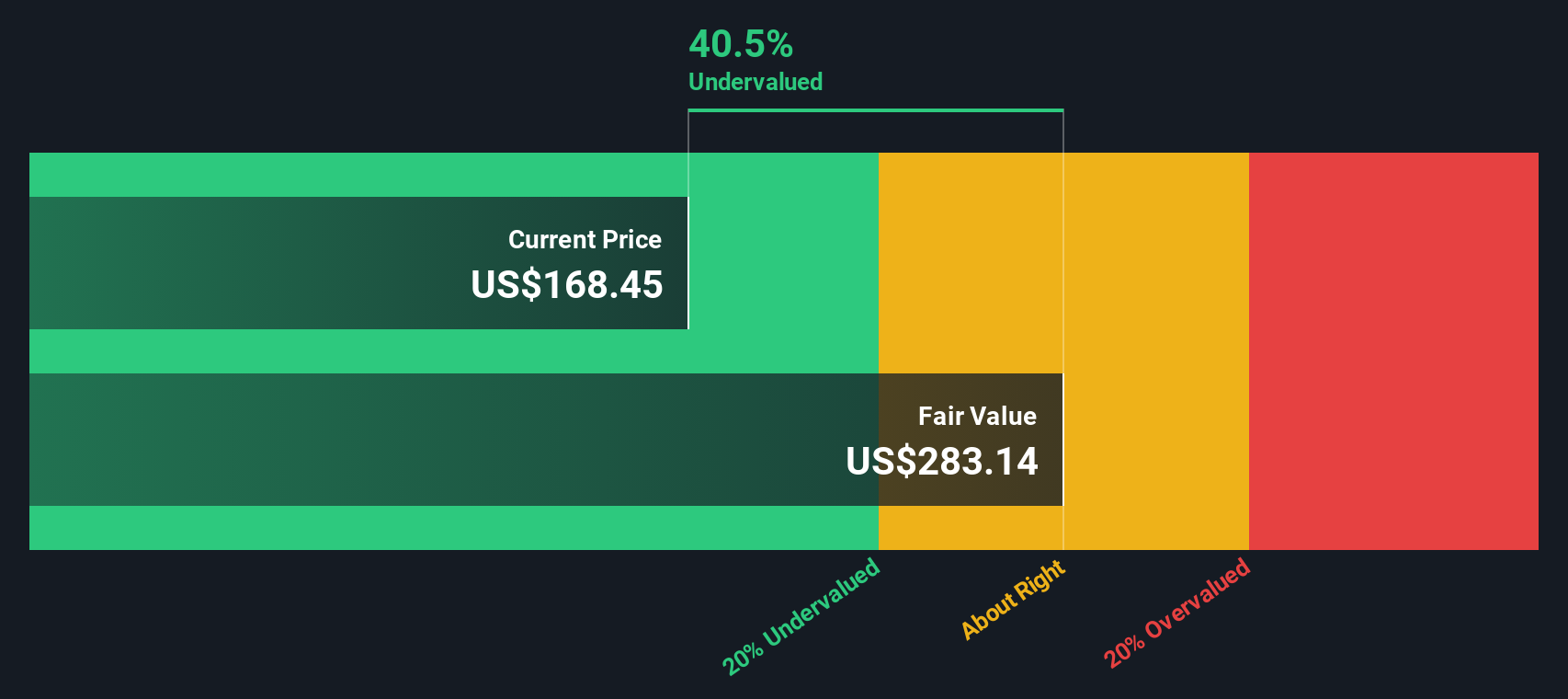

Against this backdrop, UniFirst’s share price is at US$207.99, with a 90 day share price return of 31.84% and a 30 day share price return of 5.27%. The 1 year total shareholder return is 4.86% lower, suggesting short term momentum has picked up even as longer term returns have been more muted.

If this kind of operational upgrade has caught your attention, it could be a useful moment to widen your watchlist and see fast growing stocks with high insider ownership.

With UniFirst trading at US$207.99, which is above the US$183.00 analyst price target and follows only a modest 5 year total return, the key question is whether the market is already pricing in future growth or if a buying window still exists.

Most Popular Narrative: 13.7% Overvalued

UniFirst’s widely followed narrative pegs fair value at $183.00, which sits below the last close of $207.99, putting the current price under the spotlight.

The analysts have a consensus price target of $178.25 for UniFirst based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $194.0, and the most bearish reporting a price target of just $152.0.

Want to see what kind of revenue path, margin profile, and future earnings multiple need to line up to support that valuation gap? The narrative lays out a clear set of growth assumptions, profitability targets, and required pricing of future earnings that go well beyond a simple P/E snapshot. The most interesting part is how those moving pieces interact under a single discount rate to land on that $183.00 figure.

Result: Fair Value of $183.00 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, weaker net wearer levels and rising health care costs could pressure both revenue and margins, challenging the assumptions that support the current overvaluation narrative.

Find out about the key risks to this UniFirst narrative.

Another View On Valuation

Our DCF model points to a fair value of $157.24 per share, compared with the current $207.99 price and the $183.00 narrative fair value, so it also flags UniFirst as overvalued. If both earnings multiples and cash flow math are cautious, what would need to change to close that gap?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own UniFirst Narrative

If you see the setup differently or prefer to lean on your own data work, you can pull the numbers, test your assumptions, and Do it your way in under three minutes.

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding UniFirst.

Looking for more investment ideas?

If UniFirst has you thinking differently about your portfolio, do not stop here. Run a few focused screens and see what else stands out right now.

- Spot potential growth stories early by checking out these 3523 penny stocks with strong financials that already back their operations with solid financials.

- Position yourself for long term tech shifts by scanning these 23 AI penny stocks that link artificial intelligence themes with listed companies.

- Target value focused opportunities by reviewing these 871 undervalued stocks based on cash flows that appear cheap relative to their cash flow profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com