- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Burford Capital (BUR) Valuation After The $450 Million Senior Notes Offering

Burford Capital (NYSE:BUR) has drawn fresh attention after launching a planned $450 million private offering of senior notes due 2034. The proceeds are earmarked to redeem 2026 bonds and for broader corporate uses.

See our latest analysis for Burford Capital.

The planned 2034 notes come after a period of mixed market signals, with a 30-day share price return of 8.33% and a year-to-date share price return of 11.43%. The 1-year total shareholder return is 29.46% lower, suggesting recent momentum is building from a weaker base as investors reassess Burford Capital's refinancing and its expansion moves, including the appointment of a new senior leader in Korea.

If this kind of refinancing story has your attention, it could be a good moment to broaden your search and check out fast growing stocks with high insider ownership.

With Burford trading at $9.75 alongside an indicated intrinsic discount of about 42% and a wide gap to analyst targets, you have to ask: is this a genuine value opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 48.4% Undervalued

Against Burford Capital's last close at $9.75, the most followed narrative points to a fair value of about $18.90, framing a sizeable implied gap that this new $450 million notes issue sits inside.

Platform diversification across geographies, legal verticals, and risk/duration characteristics is translating into a more robust, less volatile portfolio with greater ability to consistently realize gains and improve risk-adjusted earnings.

Curious what kind of growth story supports that valuation gap? Revenue expansion, margin assumptions and a future earnings multiple all have to line up. The full narrative spells out how those moving parts fit together.

Result: Fair Value of $18.90 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges heavily on the YPF case and on regulators not tightening rules around litigation finance. Either development could quickly challenge that underpriced thesis.

Find out about the key risks to this Burford Capital narrative.

Another View: Is The Market Already Paying Up?

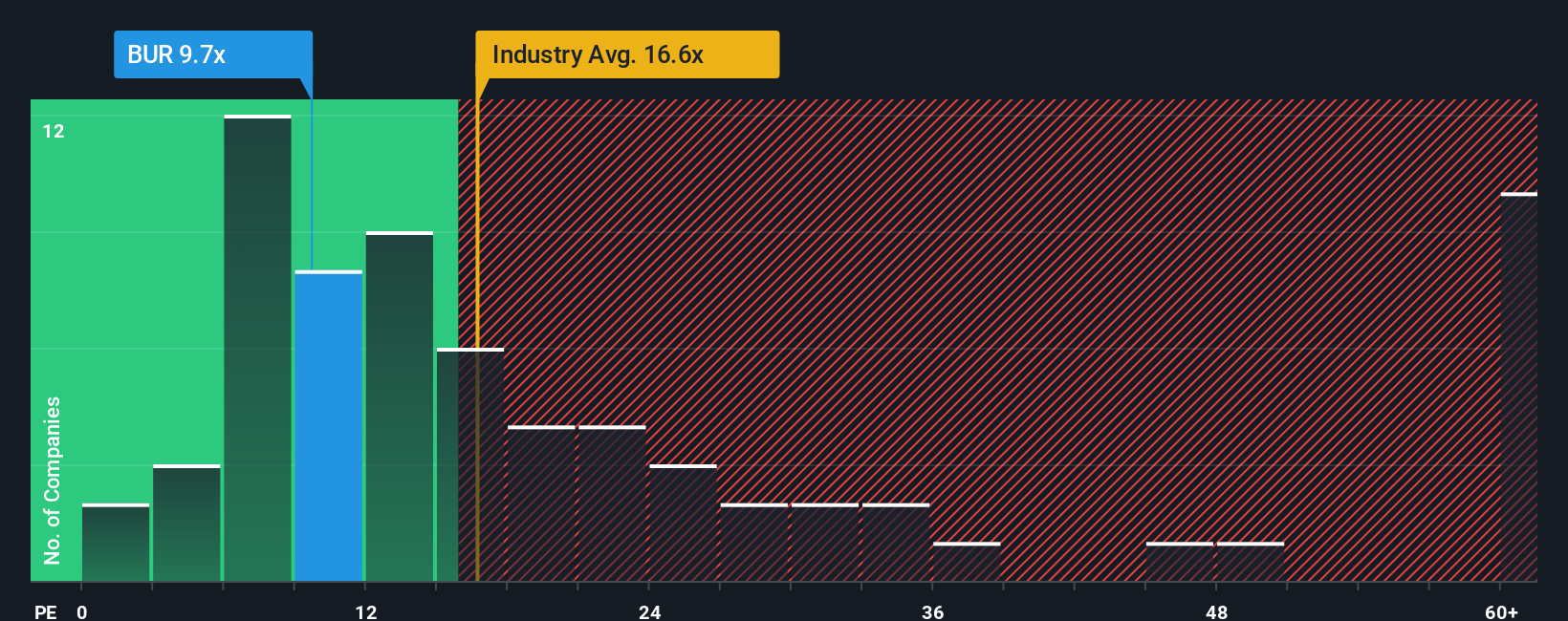

While our DCF model suggests Burford Capital is undervalued, the P/E tells a different story. At 24.5x earnings, the stock trades above the US Diversified Financial industry at 14.8x and above its own fair ratio of 22.2x, which points to some valuation risk if expectations cool.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Burford Capital Narrative

If you look at the numbers and reach a different conclusion, or simply want to test your own view against the data, you can build a complete Burford thesis in just a few minutes with Do it your way.

A great starting point for your Burford Capital research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Burford has sharpened your thinking, do not stop here. The screener gives you a fast way to surface fresh ideas before the crowd notices.

- Target income potential by checking out these 13 dividend stocks with yields > 3% if regular cash returns matter to you.

- Spot potential mispricings by scanning these 862 undervalued stocks based on cash flows that currently flag a discount on cash flow expectations.

- Get ahead of the next tech shift by reviewing these 24 AI penny stocks tied to artificial intelligence themes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com