- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Precigen (PGEN) Valuation After PAPZIMEOS Becomes Preferred First Line RRP Treatment

Precigen (PGEN) is back in focus after an expert consensus paper in The Laryngoscope recommended its PAPZIMEOS therapy as the preferred first line treatment for adults with recurrent respiratory papillomatosis.

See our latest analysis for Precigen.

Precigen shares trade at US$4.76, with a 30 day share price return of 13.60% and a 90 day share price return of 9.93%, while the 1 year total shareholder return of 242.45% points to strong recent momentum despite a mixed 5 year total shareholder return of a 44.00% loss. Recent product updates on PAPZIMEOS and the company’s presentation at the J.P. Morgan Healthcare Conference sit alongside this move, suggesting that investors may be reacting both to growing commercialization efforts and to changing perceptions of risk and opportunity around the RRP franchise.

If PAPZIMEOS has caught your eye, it could be a moment to look across the sector and check out healthcare stocks as you weigh up other healthcare names.

With Precigen returning 242.45% over the past year and still trading at a discount to the US$8.50 analyst price target, the question is whether there is still value here or if the market is already pricing in future growth.

Most Popular Narrative: 44% Undervalued

Precigen's most followed narrative sets a fair value of $8.50 per share against the last close of $4.76, framing a wide valuation gap for PAPZIMEOS-driven expectations.

Rapid uptake of PAPZIMEOS in a sizable and previously underserved adult RRP population, combined with strong physician enthusiasm and broad label coverage, supports a multi year ramp in product revenue as pent up demand converts into treated patients.

Curious what has to happen for that kind of gap to make sense? The narrative leans on aggressive revenue scaling, richer margins and a future earnings multiple more often seen in market favorites. Want to see which specific growth and profitability assumptions sit under that fair value call and how sensitive the outcome is to them?

Result: Fair Value of $8.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on PAPZIMEOS maintaining real world durability and safety, and on uptake being strong enough to cover heavy commercial and manufacturing spend.

Find out about the key risks to this Precigen narrative.

Another View: Rich On Traditional Metrics

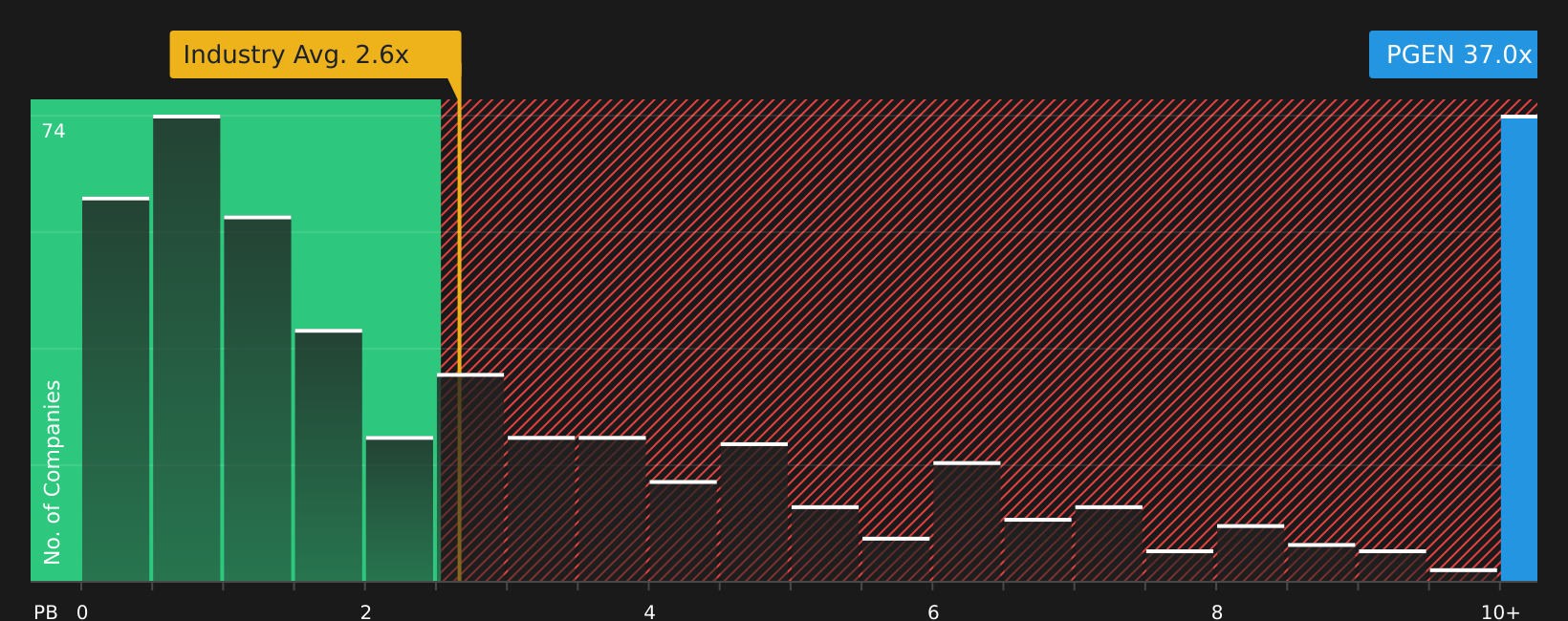

That 44% undervalued story sits awkwardly next to how the stock looks on a simple P/B check. Precigen trades on a P/B of 40.2x, compared with 6.4x for peers and 2.7x for the wider US Biotechs group, which signals a lot of optimism already in the price. If sentiment cools or expectations reset, how much room is there for disappointment?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Precigen Narrative

If you see the numbers differently or simply prefer to lean on your own work, you can pull the data, build your assumptions and Do it your way in just a few minutes.

A great starting point for your Precigen research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at one company. Use the Simply Wall St Screener to pressure test your next moves.

- Spot potential mispricings by scanning these 864 undervalued stocks based on cash flows that align with your return and risk expectations.

- Capture growth themes early by checking out these 24 AI penny stocks that are tied to real business models, not just headlines.

- Strengthen your income stream by reviewing these 13 dividend stocks with yields > 3% that may offer cash returns through changing market conditions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com