- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Sterling Infrastructure (STRL) Valuation After Strong 1 Year Return And Backlog Growth

Why Sterling Infrastructure is on investors’ radar today

Sterling Infrastructure (STRL) has been attracting attention after a strong 1 year total return of 87.6%, alongside reported revenue of US$2.23b and net income of US$315.77m. This has prompted closer scrutiny of its current share price.

See our latest analysis for Sterling Infrastructure.

At a share price of US$351.39, Sterling Infrastructure has seen an 11.9% 1 month share price return and a 10.1% year to date share price return. Its 1 year total shareholder return of 87.6% and very large 5 year total shareholder return suggest momentum has been strong over a longer period, despite some recent short term pullbacks.

If Sterling’s run has you thinking about what else is moving, it could be a good time to widen your search with fast growing stocks with high insider ownership.

With US$2.23b in revenue, US$315.77m in net income and a share price of US$351.39, the key question now is simple: is Sterling Infrastructure still undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 22.5% Undervalued

With Sterling Infrastructure last closing at $351.39 versus a narrative fair value of $453.33, the widely followed view sees a sizeable valuation gap, built on specific growth and earnings assumptions.

Record-high and growing backlog, particularly in E-Infrastructure Solutions (up 44% year-over-year to $1.2 billion), coupled with a robust pipeline of future phase work approaching $2 billion, provides strong multi-year revenue visibility and stability, mitigating downside risk to revenues and supporting sustained earnings growth.

Curious what kind of revenue path and margin profile could justify that gap to fair value, and why the implied future P/E needs to step up from today? The narrative leans heavily on E-Infrastructure strength, ongoing mega projects and buybacks to support per share outcomes, as well as a specific discount rate that pulls those expectations back into today’s price. The full story connects those moving parts into one cohesive valuation case.

Result: Fair Value of $453.33 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you also need to weigh execution risks related to mega-project dependence and labor expansion, as well as potential shifts in infrastructure funding that could challenge these assumptions.

Find out about the key risks to this Sterling Infrastructure narrative.

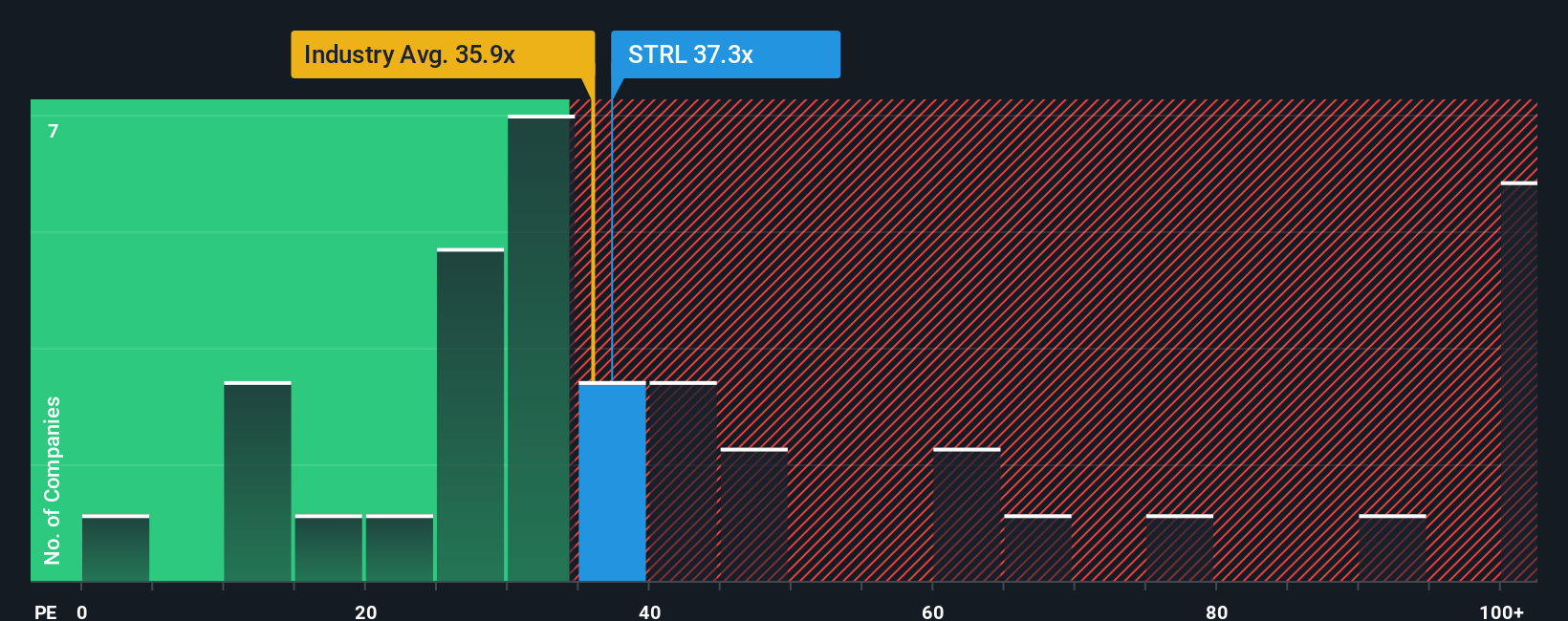

Another view on Sterling’s valuation

While the narrative fair value points to Sterling Infrastructure being 22.5% undervalued at $453.33, the P/E picture is more cautious. At 34.2x, the stock trades above the peer average of 29x and slightly above a 33.6x fair ratio, which raises the question of whether enthusiasm has run ahead of itself.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Sterling Infrastructure Narrative

If you look at these numbers and come to a different conclusion, or prefer to rely on your own analysis, you can build a tailored narrative yourself in a few minutes with Do it your way.

A great starting point for your Sterling Infrastructure research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Sterling has your attention, do not stop here. Broadening your watchlist with other focused ideas can help you spot opportunities you might otherwise miss.

- Target income potential by scanning these 13 dividend stocks with yields > 3% that may offer more consistent cash returns than you will find in many growth names.

- Capture growth themes by reviewing these 24 AI penny stocks at the intersection of artificial intelligence and real business use cases.

- Position early in new trends by checking these 18 cryptocurrency and blockchain stocks tied to blockchain, digital assets, and next generation payment infrastructure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com