- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

OceanFirst Financial (OCFC) Valuation Check After Earnings Beat And Merger And Investment Plans

OceanFirst Financial (OCFC) is back in focus after quarterly results came in ahead of expectations on both revenue and non GAAP profit, helped by strong loan growth, higher net interest income, and ongoing merger activity.

See our latest analysis for OceanFirst Financial.

Despite the earnings beat and ongoing merger and capital initiatives, the 1 day share price return of 3.7% and 1 month share price return of 6.3% suggest some investors are reassessing near term risks, while the 5 year total shareholder return of 25.7% points to a steadier longer run record.

If this regional bank story has your attention, it could be a good moment to broaden your search and check out fast growing stocks with high insider ownership.

With OceanFirst trading at $18.48, sitting at a discount to the average analyst price target of $21.00 and an intrinsic value estimate that implies a premium, it is reasonable to ask whether there is still a buying opportunity here or whether the market is already pricing in future growth.

Most Popular Narrative: 13.4% Undervalued

OceanFirst Financial's most followed narrative pegs fair value at about $21.33 per share, compared with the latest close at $18.48, putting the focus squarely on what is driving that gap.

Ongoing digital initiatives and technology investments, including fintech partnerships, are enhancing operating leverage by reducing the incremental cost to serve and driving engagement with younger, tech savvy demographics, potentially increasing fee based income and improving net margins over time.

Curious what has to happen for that valuation to make sense? The narrative highlights assumptions around faster revenue expansion, higher margins, and a meaningfully different future earnings multiple. The full breakdown explains how those inputs are combined to arrive at the $21.33 figure.

Result: Fair Value of $21.33 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, those assumptions could be challenged if uneven loan demand persists or if deposit competition keeps funding costs high, which would put pressure on margins and future earnings expectations.

Find out about the key risks to this OceanFirst Financial narrative.

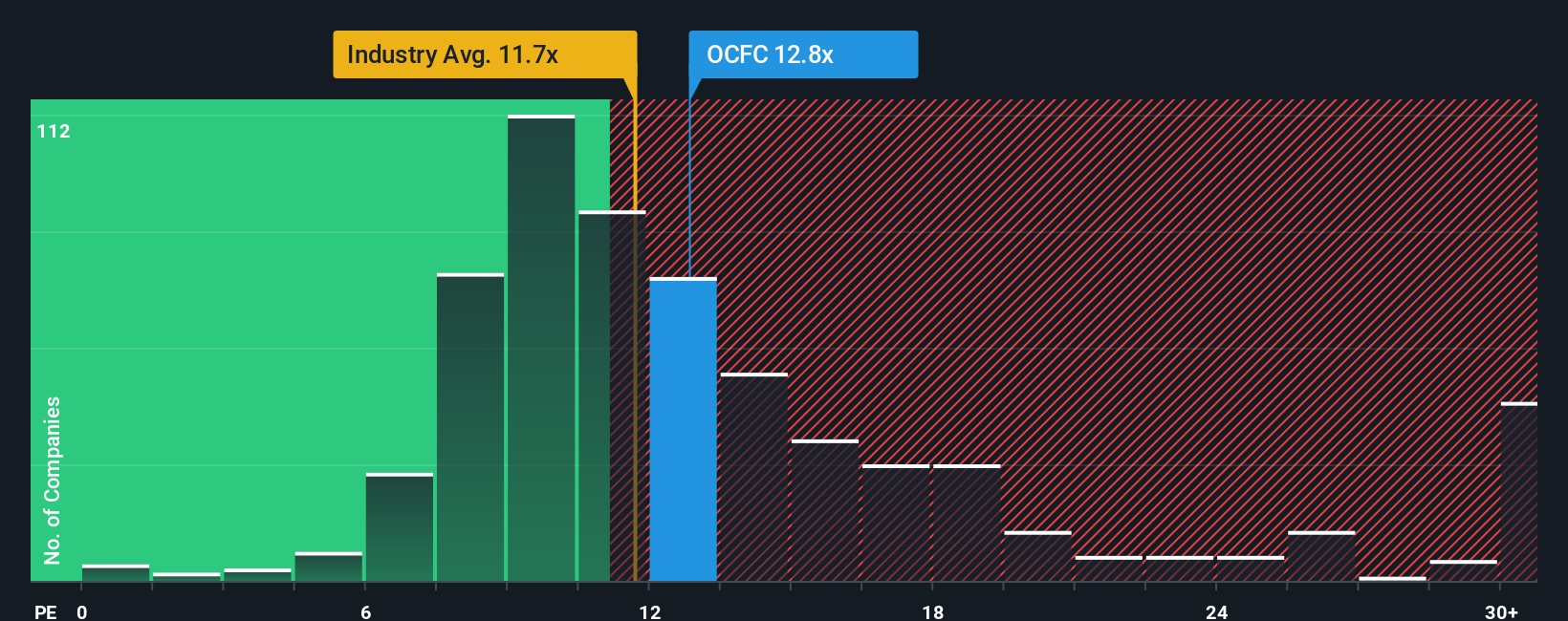

Another View: Earnings Multiple Sends a Different Signal

While the most followed narrative points to fair value of $21.33 and a 13.4% discount, the current P/E of 15.8x tells a more cautious story. It sits above the US Banks industry at 12.1x and above peers at 13.3x, even though the fair ratio is 27.2x. That gap leaves you weighing valuation risk against potential upside if sentiment shifts.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own OceanFirst Financial Narrative

If you see the numbers differently or prefer to stress test the assumptions yourself, you can create your own view in minutes with Do it your way.

A great starting point for your OceanFirst Financial research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If OceanFirst has sharpened your thinking, do not stop here. Use the screener to spot other opportunities that match your style before they move without you.

- Target potential value opportunities by reviewing these 864 undervalued stocks based on cash flows that align with your preferred price and quality filters.

- Capture growth themes at the frontier of technology by scanning these 24 AI penny stocks that fit your risk and return expectations.

- Strengthen your income watchlist by reviewing these 13 dividend stocks with yields > 3% that may complement a long term, cash flow focused portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com