- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Schrödinger (SDGR) Valuation Check As New AI Partnerships With Manas AI And Eli Lilly Take Shape

AI partnerships put Schrödinger (SDGR) in focus

Schrödinger (SDGR) has moved into the spotlight after a multi-year agreement with Manas AI for deep access to its physics-based computational platform, alongside a separate AI collaboration with Eli Lilly's TuneLab.

For you as an investor, these deals center on Schrödinger's software being embedded in AI-driven molecular discovery workflows and being used as a preferred interface for biotech users tapping into Lilly's TuneLab capabilities.

See our latest analysis for Schrödinger.

Despite these new AI-focused agreements, Schrödinger’s recent share price performance has been weak, with a 90-day share price return showing a 27.09% decline and a 1-year total shareholder return showing a 33.44% decline, pointing to fading momentum even as partnership news builds interest.

If these AI collaborations have caught your attention, it could be a good moment to scan other healthcare names by checking out healthcare stocks as potential additions to your watchlist.

With the shares down over the past year, trading at US$16.42 and screens flagging a possible intrinsic discount, you have to ask yourself: is Schrödinger being overlooked here, or is the market already pricing in future growth?

Most Popular Narrative: 39.9% Undervalued

Schrödinger's most followed narrative estimates fair value at $27.30, well above the last close at $16.42. This sets up a valuation story driven by growth expectations and improving margins over time.

Strong pipeline advancement and early clinical success, such as positive Phase I data for SGR-1505, positions the company to secure additional milestone payments, royalties, and out-licensing deals, creating potential for substantial long-term revenue growth and more predictable future cash flows.

Curious what kind of revenue ramp, margin shift, and future earnings multiple have to line up to back that $27.30 fair value? The narrative leans on steady software growth, richer profitability assumptions, and a premium future valuation that many investors would usually associate with higher visibility stories. If you want to see exactly how those moving parts fit together, the full write up lays the assumptions out in black and white.

Result: Fair Value of $27.30 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you also have to weigh softer software gross margins and reliance on volatile milestone and royalty revenue, which could easily knock this story off course.

Find out about the key risks to this Schrödinger narrative.

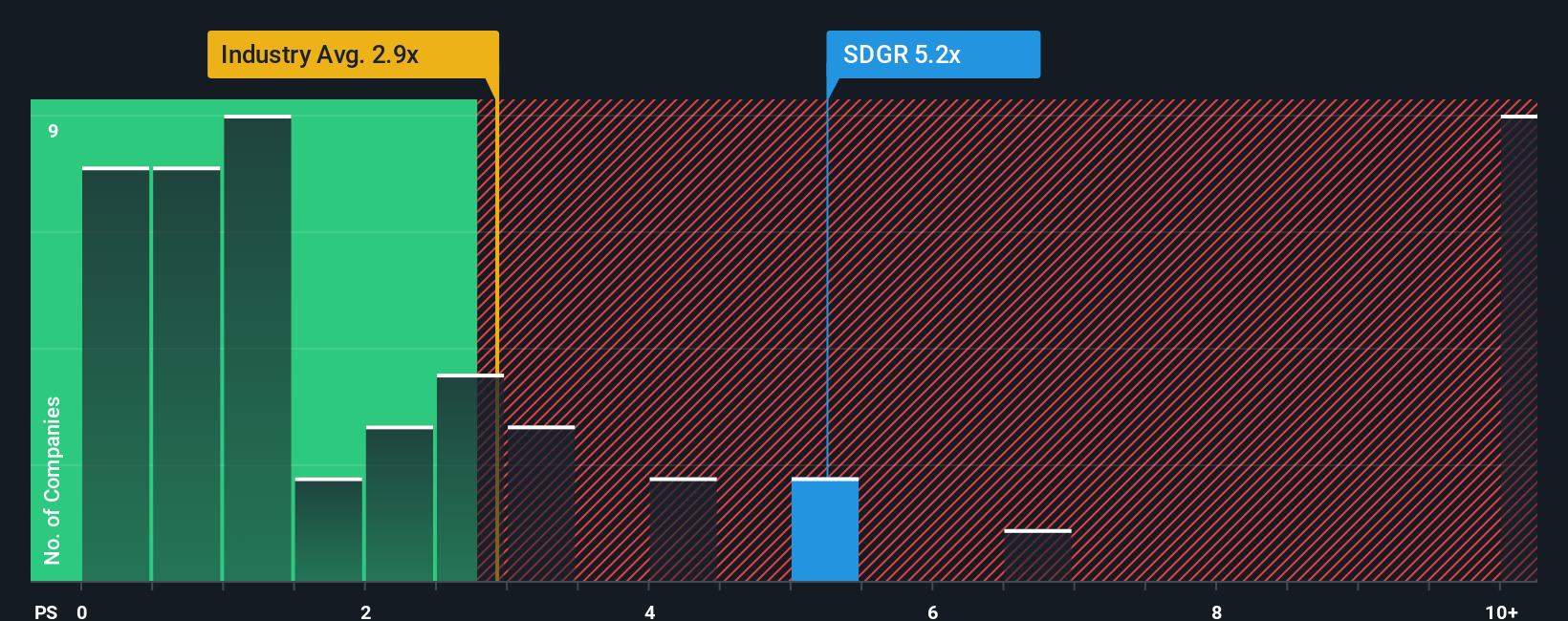

Another View: Multiples Paint a Tougher Picture

If you put the narratives and intrinsic value estimates to one side and just look at the current P/S of roughly 5x, the story flips. The fair ratio sits at 2.6x, and peers are closer to 1.9x to 2.2x. This points to meaningful valuation risk if sentiment cools.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Schrödinger Narrative

If you look at the numbers and reach a different conclusion, or simply prefer building your own thesis from the ground up, you can frame a tailored view in just a few minutes, starting with Do it your way

A great starting point for your Schrödinger research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Schrödinger has sparked your curiosity, do not stop there. Use the Simply Wall St Screener to spot fresh ideas that suit how you like to invest.

- Target dependable cash flows by scanning these 12 dividend stocks with yields > 3% that may offer more consistent income potential alongside capital appreciation.

- Hunt for mispriced opportunities by reviewing these 872 undervalued stocks based on cash flows that screens flag as trading below estimated intrinsic value.

- Get ahead of emerging themes by checking these 19 cryptocurrency and blockchain stocks tied to blockchain, digital assets, and related infrastructure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com