- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Bilibili (BILI) Valuation After First Profitable Year And AI Driven Advertising Shift

Profitability milestone puts Bilibili (BILI) at an inflection point

Bilibili (BILI) has just reported its first profitable year in 2025, supported by higher gross margins, advertising revenue and self developed games. At the same time, AI driven ad tools and cost controls are reshaping both its business model and community risks.

See our latest analysis for Bilibili.

The latest share price of US$33.40 comes after a 34.84% 1 month share price return and a 26.66% year to date share price return. The 1 year total shareholder return of 97.75% contrasts with a 5 year total shareholder return decline of 70.67%, suggesting momentum has recently picked up despite a difficult longer term record.

If Bilibili’s recent swing into profitability has your attention, this could be a useful moment to see how other tech names are shaping up through high growth tech and AI stocks.

With Bilibili now profitable, a 1-year total return near 98% and an intrinsic value estimate implying an 11% discount, the key question is whether there is still a buying opportunity here or if markets are already pricing in future growth.

Most Popular Narrative: 7.3% Overvalued

The most followed narrative pegs Bilibili’s fair value at about $31.14, a touch below the recent $33.40 close. This frames the current optimism in a tighter valuation band.

The expansion and monetization of Bilibili's creator ecosystem is creating new revenue streams through value-added services (memberships, fan charging, e-commerce), tapping into the rising demand for user-generated content and the growth of the creator economy; this supports higher ARPU and margin improvement.

Curious what kind of revenue mix, margin profile, and earnings power it takes to justify this richer price tag? The narrative leans on ambitious growth, rising profitability, and a future earnings multiple usually reserved for established leaders. The full set of assumptions spells out how those pieces are expected to fit together.

Result: Fair Value of $31.14 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear pressure points, including heavy reliance on youth demand in China and ongoing regulatory scrutiny that could affect growth expectations.

Find out about the key risks to this Bilibili narrative.

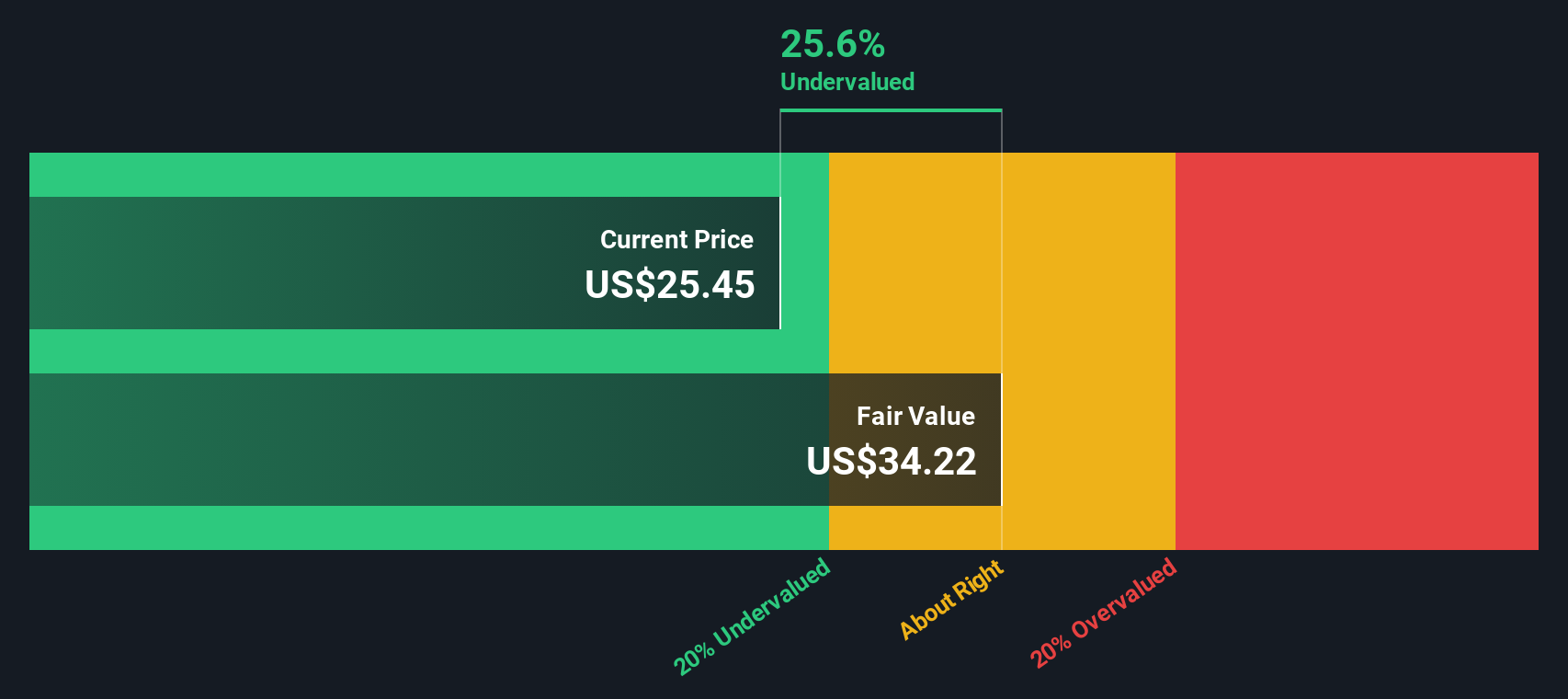

Another View: Cash Flows Paint A Different Picture

While the popular narrative suggests Bilibili is about 7.3% overvalued at $33.40, our DCF model indicates a fair value estimate of $37.41 instead. That 10.6% gap based on future cash flows raises a simple question: which story do you think is closer to reality?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Bilibili for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 872 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Bilibili Narrative

If you are not fully aligned with these views or simply want to test your own assumptions, you can build a personalized Bilibili thesis in just a few minutes with Do it your way.

A great starting point for your Bilibili research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Bilibili has sharpened your interest, do not stop here. Use the Screener to quickly spot other potential opportunities before they move without you.

- Target income focused opportunities by checking out these 12 dividend stocks with yields > 3% that might suit a portfolio built around regular cash returns.

- Expand your watchlist with growth themes by reviewing these 24 AI penny stocks that tie into long term trends in automation and machine learning.

- Hunt for potential mispricing by scanning these 872 undervalued stocks based on cash flows where market expectations and cash flow estimates may be out of sync.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com