- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At AbCellera Biologics (ABCL) Valuation After ABCL635 Advances Into Phase 2 Trial

AbCellera Biologics (ABCL) has begun dosing patients in the Phase 2 portion of its Phase 1/2 trial for ABCL635, a potential first in class non hormonal treatment for menopausal vasomotor symptoms.

See our latest analysis for AbCellera Biologics.

The ABCL635 Phase 2 start comes as AbCellera’s 30 day share price return of 15.05% and year to date share price return of 24.78% contrast with a 3 year total shareholder return of 58.89% decline, suggesting sentiment has improved recently after a difficult longer term run.

If this kind of clinical progress has your attention, it could be a good moment to survey other healthcare stocks that are trying to solve important medical problems too.

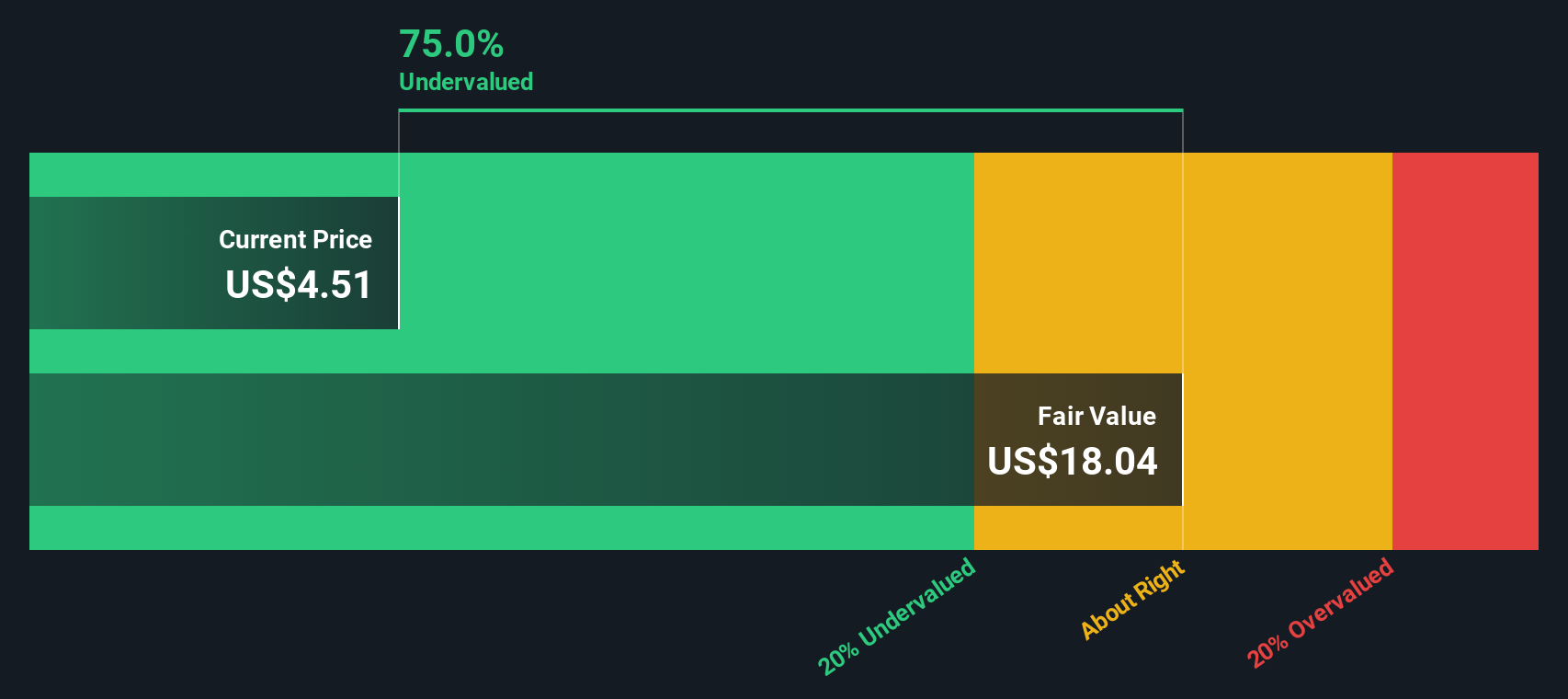

With AbCellera’s shares trading at US$4.28 and sitting at what appears to be a steep discount to analyst and intrinsic value estimates, is the market underestimating future progress or already factoring in the next stage of growth?

Price-to-Sales of 36.3x: Is it justified?

At the last close of US$4.28, AbCellera trades on a P/S of 36.3x, which sits well above both its Life Sciences peers and the levels implied by some fair value models.

The P/S ratio compares the company’s market value to its revenue, and it is often used for early stage or unprofitable businesses where earnings are not yet a reliable guide.

For AbCellera, a 36.3x P/S suggests investors are paying a high price for each dollar of current revenue. This is the case even though our DCF work indicates the shares are trading 74.9% below an internal estimate of future cash flow value of US$17.07 per share.

Against that comparison, the 36.3x P/S stands in sharp contrast to the US Life Sciences industry average of 3.8x and a peer average of 4.7x. It is also far above an estimated fair P/S of 0x, a level that implies the market could move a long way if expectations reset around those benchmarks.

Explore the SWS fair ratio for AbCellera Biologics

Result: Price-to-sales of 36.3x (OVERVALUED)

However, the story can shift quickly if trials disappoint or if AbCellera’s current revenue base of US$35.3m and net loss of US$171.7m begin to weigh more heavily on sentiment.

Find out about the key risks to this AbCellera Biologics narrative.

Another View: What Our DCF Model Suggests

While the 36.3x P/S points to a rich price tag against current revenue, our DCF model paints a very different picture. On that approach, AbCellera at US$4.28 screens as trading 74.9% below an estimated future cash flow value of US$17.07 per share. So is this a warning that sales based comparisons are too harsh, or is the cash flow model leaning too much on assumptions that may not play out?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out AbCellera Biologics for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 876 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own AbCellera Biologics Narrative

If you would rather weigh the numbers yourself and challenge these assumptions, you can pull the key metrics together in minutes and Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding AbCellera Biologics.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at one stock. Use the screener to quickly spot patterns, risks, and fresh opportunities.

- Chase potential mispricing by scanning these 876 undervalued stocks based on cash flows that may offer more attractive entry points based on their cash flow profiles.

- Spot emerging themes early by filtering for these 19 cryptocurrency and blockchain stocks that are tied to blockchain infrastructure and digital assets.

- Target future facing opportunities by honing in on these 23 AI penny stocks where artificial intelligence is central to the business model.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com