- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Chart Industries (GTLS) Valuation As Recent Returns Offer Mixed Signals

Why Chart Industries is on investors’ radar today

Chart Industries (GTLS) has recently attracted interest as investors weigh its current share price of US$207.41 against estimates of intrinsic value and recent total return figures across the past year and past 3 months.

See our latest analysis for Chart Industries.

While the recent 90 day share price return of 3.76% points to gradually improving momentum around the current US$207.41 level, the 1 year total shareholder return of 3.19% decline contrasts with a stronger 3 year total shareholder return of 63.02% and 5 year total shareholder return of 45.33%. This keeps longer term holders focused on how expectations for growth and risk are changing.

If Chart’s recent moves have you reassessing your watchlist, this could be a good moment to broaden your search with aerospace and defense stocks.

With Chart Industries trading near US$207 and showing a 27% discount to one intrinsic value estimate, yet sitting close to analyst targets, the key question is whether you are seeing mispricing here or a market that has already incorporated expectations of future growth.

Most Popular Narrative: 0.4% Overvalued

With Chart Industries last closing at US$207.41 against a narrative fair value of US$206.67, the current price sits slightly above that implied level. This puts the focus firmly on what is driving the future earnings story behind that estimate.

The company is strategically positioned in high-demand markets such as LNG, data centers, and space exploration, providing a strong pipeline of future projects and potential for significant revenue growth. Chart Industries is focusing heavily on growing its aftermarket service and repair business, which comprises a third of its revenue and offers higher margins, potentially improving overall earnings.

Want to see what kind of revenue path and margin uplift would support that fair value so close to today’s price, including how earnings and valuation multiples are expected to evolve over the next few years, and what assumptions sit behind that future profit profile, sector by sector?

Result: Fair Value of $206.67 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story can change quickly if tariff pressures bite harder than expected, or if large LNG and space projects are delayed or canceled.

Find out about the key risks to this Chart Industries narrative.

Another View: What the multiples are saying

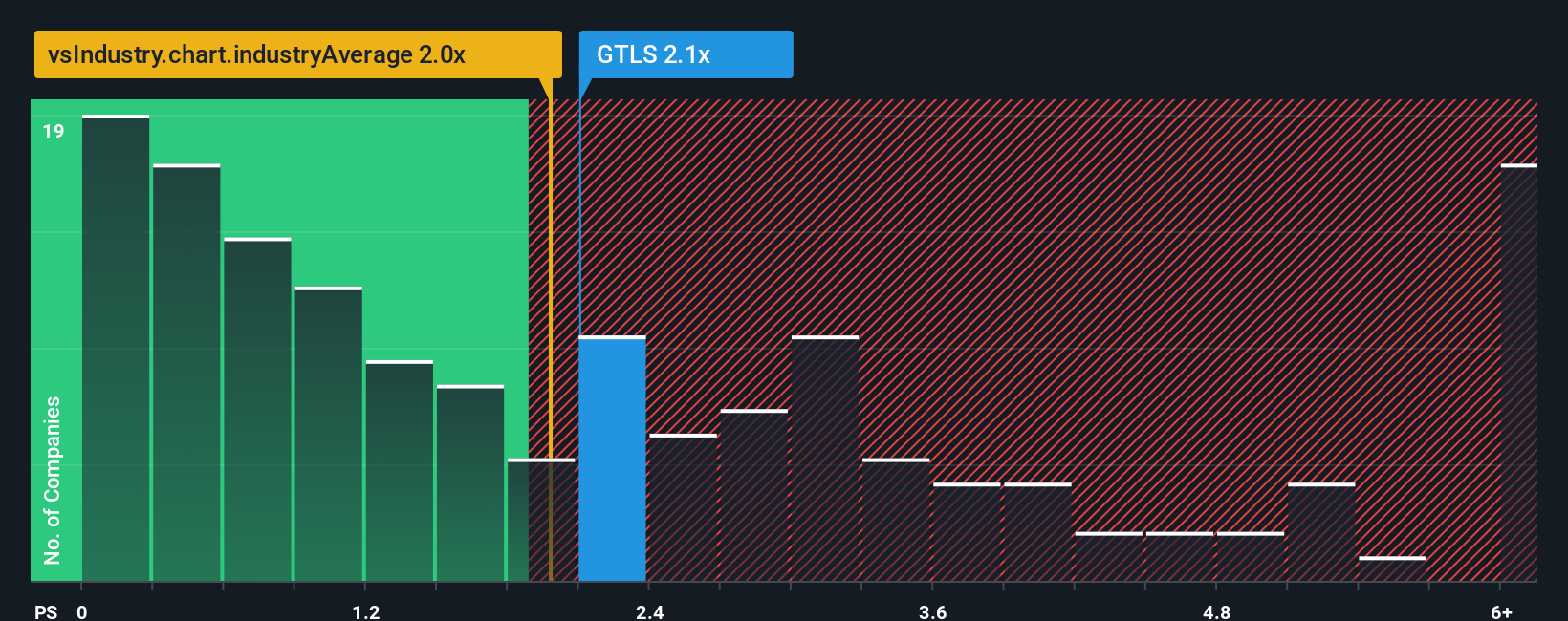

Our DCF view suggests Chart Industries is trading at a 27.2% discount to an estimated fair value of US$285.07, while its current price is only 0.4% above one narrative fair value estimate. On a price-to-sales multiple of 2.2x, it looks slightly richer than the US Machinery industry at 2.1x, but cheaper than peers at 3.5x and below an estimated fair ratio of 2.5x. That mixed picture leaves you deciding which signal you trust more: the cash flow model or the current market multiples.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Chart Industries Narrative

If this narrative does not quite line up with your own view, or you would rather test the numbers yourself, you can build a custom take in just a few minutes using Do it your way.

A great starting point for your Chart Industries research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If Chart Industries is already on your radar, do not stop there. Use this momentum to size up a few more focused ideas in minutes.

- Spot potential bargains early by checking out these 863 undervalued stocks based on cash flows that line up with your view on pricing and fundamentals.

- Tap into fast moving themes across digital assets with these 80 cryptocurrency and blockchain stocks that puts listed cryptocurrency and blockchain names in one place.

- Strengthen your income watchlist by filtering for these 12 dividend stocks with yields > 3% that meet your preferred yield and quality thresholds.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com