- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Zymeworks (ZYME) Valuation After Positive HERIZON GEA 01 Trial Results And Royalty Milestone Potential

Zymeworks (ZYME) shares are back in focus after the company reported Phase 3 HERIZON-GEA-01 results for Ziihera in HER2-positive gastroesophageal cancer, paired with sizeable potential milestone and royalty economics tied to future regulatory decisions.

See our latest analysis for Zymeworks.

The Zymeworks share price, now at US$23.63, has been volatile, with a 28.42% 90 day share price return and a 68.91% 1 year total shareholder return suggesting momentum has been building despite a weaker year to date share price return, recent leadership changes, and the Ziihera trial update.

If Zymeworks has caught your attention after the Ziihera data, this could be a good moment to see how it compares with other healthcare stocks that are moving on clinical and pipeline news.

With Zymeworks trading at US$23.63, a value score of 4, an indicated discount to analyst targets, and sizeable potential milestones on the table, is the market underestimating future cash flows or already pricing in the Ziihera story?

Most Popular Narrative: 31.5% Undervalued

With Zymeworks last closing at US$23.63 against a most followed fair value estimate of US$34.50, the narrative points to a sizeable valuation gap tied to its royalty heavy model and HER2 franchise.

Analysts are broadly constructive on Zymeworks, highlighting both the de risked nature of its lead assets and the upside from its emerging royalty platform, while still flagging execution risks around the new strategy.

Bullish analysts are lifting price targets into the mid to high 30s and low 40s, pointing to upside versus current trading levels as HERIZON GEA 01 and early ZW191 data are incorporated into models.

Want to see what is behind that royalty centric fair value? Revenue compounding, shifting profit margins and a steep future earnings multiple all sit at the core of this narrative.

Result: Fair Value of $34.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the story could change quickly if partner-led milestones disappoint or early-stage assets stumble in trials, putting those future royalty-heavy cash flows in question.

Find out about the key risks to this Zymeworks narrative.

Another Take: Multiples Tell a Different Story

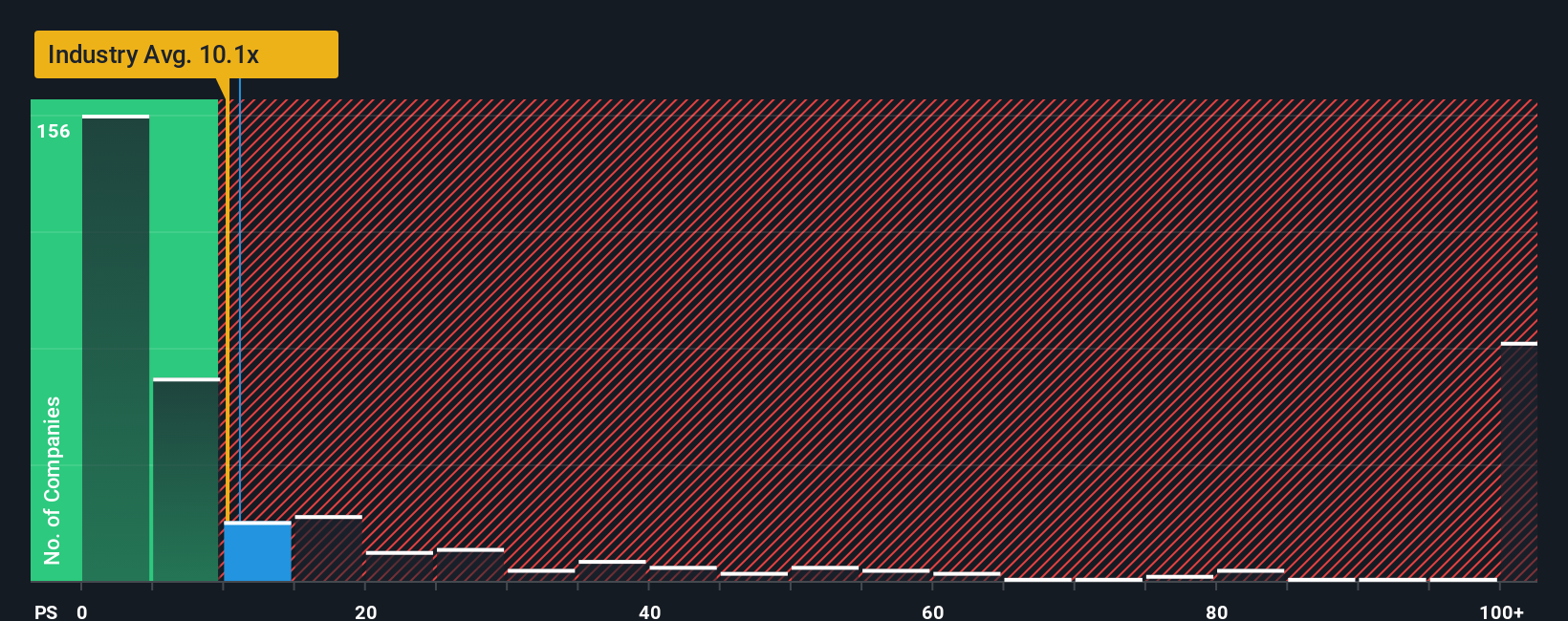

Our narrative fair value points to Zymeworks as undervalued, but the current P/S of 13.1x is higher than both the US Biotechs industry at 12.8x and the company’s own fair ratio of 2.4x. That gap suggests investors are already paying a premium, which may limit the remaining valuation cushion.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Zymeworks Narrative

If you look at the numbers and come to a different conclusion, or just want to test your own view against the data, you can build a tailored Zymeworks thesis in a few minutes using Do it your way.

A great starting point for your Zymeworks research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Zymeworks has sharpened your interest, do not stop here. Use this moment to scan other opportunities that could fit your portfolio before the crowd catches on.

- Spot potential value by checking out these 867 undervalued stocks based on cash flows that might offer pricing that still lines up with their underlying cash flows.

- Tap into cutting edge themes by reviewing these 24 AI penny stocks that are tied to artificial intelligence trends influencing many sectors.

- Strengthen your income focus by assessing these 12 dividend stocks with yields > 3% that may help you build a more consistent cash return profile.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com